Answered step by step

Verified Expert Solution

Question

1 Approved Answer

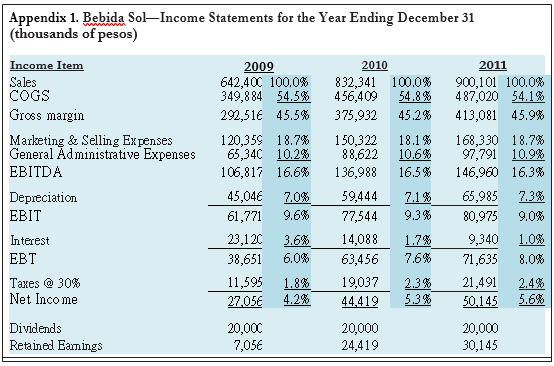

Kol a T he C apit al B udgeting Decision Analyze the possible investment in a new product line, a soda named Kola. A market

KolaThe Capital Budgeting Decision

- Analyze the possible investment in a new product line, a soda named Kola. A market study should be done to gauge the potential demand before the firm undertook the investment.

- Consumer groups in Mexico had demanded that the government impose a 20% tax on soft drinks, claiming that it would not only reduce consumption, but the tax revenue could also be used to fight health problems that soft drinks generated

- The market leaders accounted for a combined market share of more than 90%. The Mexican soft drink market had total revenues of $39.2bn in 2011, representing a compound annual growth rate (CAGR) of 6.3% between 2007 and 2011. Market consumption volumes increased with a CAGR of 4.5% between 2007 and 2011, reaching a total of 49.3 billion liters in 2011.4

- The poorer segment of the population. To capture this market, he started the company to offer about half the price. Bebida products were sold only in small, independent grocery stores and convenience stores in Mexico.5 The firm avoided the supermarkets and hypermarkets because it could not sustain the desired margin.

- The owners of these independent stores were given incentives to personally promote the products. Sales increased dramatically. from 80 million pesos in 1998 to about 900 million pesos in 2011.

- Antonio started working on the sales side of the business two years before his fathers death.

- The global financial crisis hit. The economic downturn in Mexico actually benefitted the low-price soda business. Demand increased dramatically as many consumers became price conscious and switched from international brands to private labels. Bebida Sols sales increased by 60% from 2008 to 2009, and continued to increase without the firm changing any of its business strategy or practices. The companys return on sales (net profit margin) also had been increasing in the last few years.

The Proposal

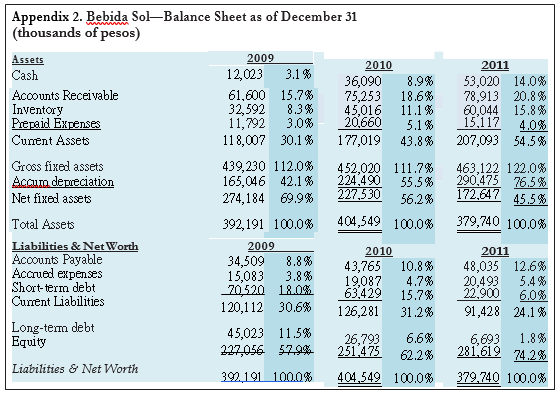

- Sol had accumulated a sizable amount of cash. With solid financial performance and steady cash flows, his banker had agreed to extend him a five-year, 16% annual interest term loan to launch Hola-Kola. In the proposal, Pedro Cortez estimated that with 20% of the needed capital borrowed, the 20/80 debt-equity structure would result in an 18.2% weighted average cost of capital for this project.

- Bigger question lingering in Antonios mind was whether there would be sufficient demand for this new, zero-calorie product line.

- If it were the former, the outlook for low- price, low-calorie carbonated soft drinks might not be too promising at this time. If it were the latter, it might be the perfect timing for Bebida Sol to introduce Hola-Kola.

- Pedro hired a consultant to do a market study right after Antonio discussed the idea of Hola-Kola with him. The consultant estimated that the company could sell a total of 600,000 liters of these zero-calorie carbonates a month, at a projected price of five pesos a liter. This volume of sales was expected for a period of five years at the same price. The market study took about two months to complete and cost the company five million pesos, which Pedro had paid shortly after its completion.

- Since the existing bottling plant was running at 100% capacity producing regular sodas, the proposal called for a fleet of new, semi-automated bottling and kegging machines designed for long, high-quality runs. The total cost of these machines, including installation, was estimated to be 50 million pesos. This amount could be fully depreciated on a straight-line basis over a period of five years. Pedro believed that the purchase of these machines would enable Bebida Sol to reduce its cost of labor and therefore the price to the customers, putting the firm in a more competitive position. With proper maintenance, these machines could produce at least 600,000 liters of carbonated drinks per month. Pedro also estimated that these machines would have a resale value of four million pesos in five years time, if the company were to either shut down the production of Hola-Kola, or replace these machines with fully automated ones at that time.

- The new machines would be housed in an unoccupied annex by the main production facility of Bebida Sol. The annex was also large enough to store the finished products before they were shipped out to grocery stores. Antonios father built the annex years ago when he planned to venture into the mineral water business. He died before he could execute his plan. The annex had been vacant ever since, even though Antonio recently received an offer to lease out the space for 60,000 pesos a year.

- Pedro determined that additional working capital was needed to ensure smooth production and sales of this new product line. He proposed keeping raw materials inventory at a level equal to one month of produc- tion. To encourage the independent grocery stores to carry the new product line, he proposed offering a longer collection period, letting the grocers pay in 45 days, instead of the normal 30 days. As far as accounts payable, he would follow the companys normal policy, and settle the accounts in 36 days.

- The proposal also outlined the various estimates of production and overhead costs, and selling expenses. Raw materials needed to produce the sodas were estimated to be 1.8 pesos per liter, while labor costs and energy costs per month were estimated to be 180,000 pesos and 50,000 pesos, respectively. The incremental general administrative and selling expenses were quite modest, estimated to be 300,000 a year, as the new product could be sold by Bebida Sols current sales force and via existing distribution channels. The accounting department typically charged 1% of sales as overhead costs for any new projects.

- Glancing back at his notes, Antonio started pondering. The market study seemed to indicate sufficient demand for the new product line. What he really feared was that the new zero-calorie carbonates might erode the sales of his existing productsthe regular sodas. The market study suggested that potential erosion could cost the firm as much as 800,000 pesos of after-tax cash flows per year. At the new tax rate of 30% for both income and capital gains, could he add value to the firm by taking on this project?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Forecasting Principles And Practice

Authors: Rob J Hyndman, George Athanasopoulos

1st Edition

0987507109, 978-0987507105