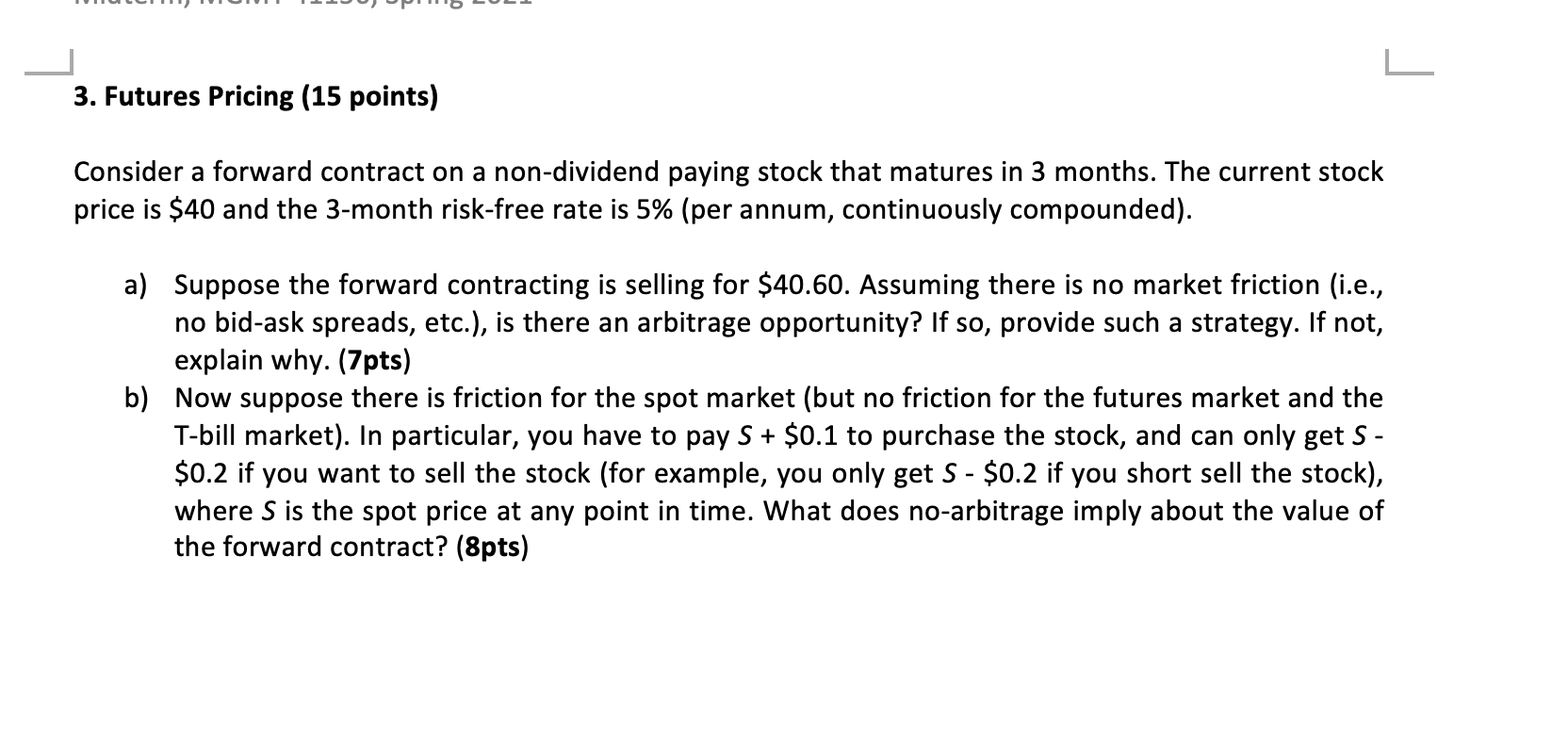

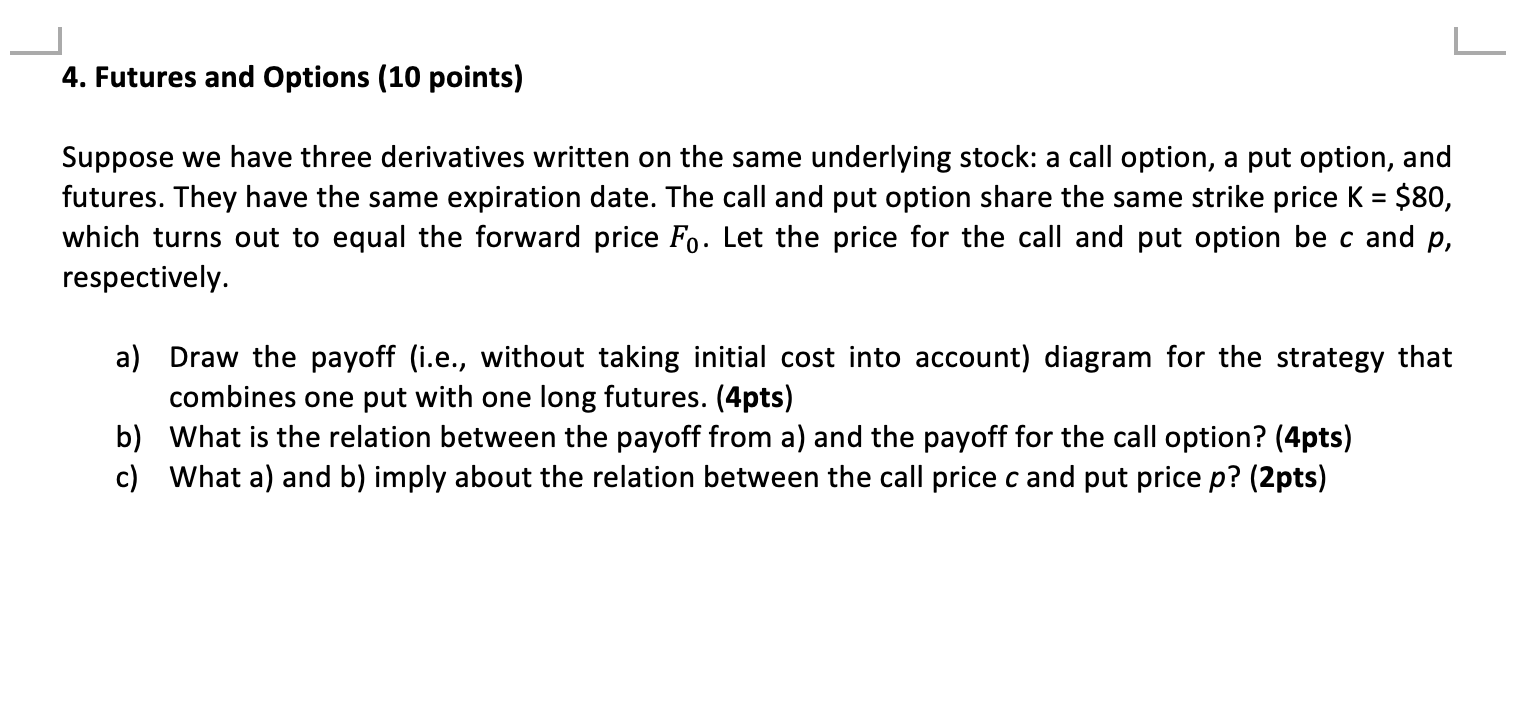

L 3. Futures Pricing (15 points) Consider a forward contract on a non-dividend paying stock that matures in 3 months. The current stock price is $40 and the 3-month risk-free rate is 5% (per annum, continuously compounded). a) Suppose the forward contracting is selling for $40.60. Assuming there is no market friction (i.e., no bid-ask spreads, etc.), is there an arbitrage opportunity? If so, provide such a strategy. If not, explain why. (7pts) b) Now suppose there is friction for the spot market (but no friction for the futures market and the T-bill market). In particular, you have to pay S + $0.1 purchase the stock, and can only get S - $0.2 if you want to sell the stock (for example, you only get S - $0.2 if you short sell the stock), where S is the spot price at any point in time. What does no-arbitrage imply about the value of the forward contract? (8pts) 4. Futures and Options (10 points) Suppose we have three derivatives written on the same underlying stock: a call option, a put option, and futures. They have the same expiration date. The call and put option share the same strike price K = $80, which turns out to equal the forward price Fo. Let the price for the call and put option be c and p, respectively. a) Draw the payoff (i.e., without taking initial cost into account) diagram for the strategy that combines one put with one long futures. (4pts) b) What is the relation between the payoff from a) and the payoff for the call option? (4pts) c) What a) and b) imply about the relation between the call price cand put price p? (2pts) L 3. Futures Pricing (15 points) Consider a forward contract on a non-dividend paying stock that matures in 3 months. The current stock price is $40 and the 3-month risk-free rate is 5% (per annum, continuously compounded). a) Suppose the forward contracting is selling for $40.60. Assuming there is no market friction (i.e., no bid-ask spreads, etc.), is there an arbitrage opportunity? If so, provide such a strategy. If not, explain why. (7pts) b) Now suppose there is friction for the spot market (but no friction for the futures market and the T-bill market). In particular, you have to pay S + $0.1 purchase the stock, and can only get S - $0.2 if you want to sell the stock (for example, you only get S - $0.2 if you short sell the stock), where S is the spot price at any point in time. What does no-arbitrage imply about the value of the forward contract? (8pts) 4. Futures and Options (10 points) Suppose we have three derivatives written on the same underlying stock: a call option, a put option, and futures. They have the same expiration date. The call and put option share the same strike price K = $80, which turns out to equal the forward price Fo. Let the price for the call and put option be c and p, respectively. a) Draw the payoff (i.e., without taking initial cost into account) diagram for the strategy that combines one put with one long futures. (4pts) b) What is the relation between the payoff from a) and the payoff for the call option? (4pts) c) What a) and b) imply about the relation between the call price cand put price p? (2pts)