Answered step by step

Verified Expert Solution

Question

1 Approved Answer

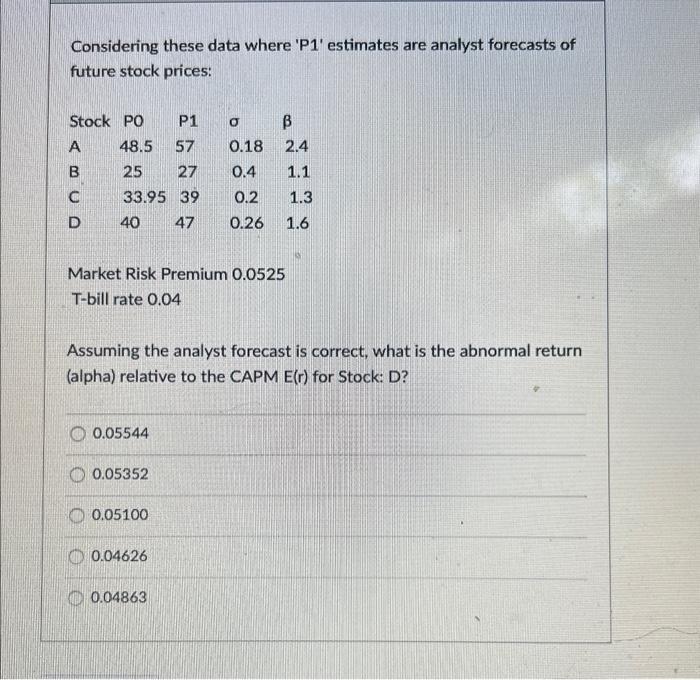

L7 Considering these data where 'P1' estimates are analyst forecasts of future stock prices: Market Risk Premium 0.0525 T-bill rate 0.04 Assuming the analyst forecast

L7

Considering these data where 'P1' estimates are analyst forecasts of future stock prices: Market Risk Premium 0.0525 T-bill rate 0.04 Assuming the analyst forecast is correct, what is the abnormal return (alpha) relative to the CAPM E(r) for Stock: D? 0.05544 0.05352 0.05100 0.04626 0.04863 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Applied Equity Analysis and Portfolio Management Tools to Analyze and Manage Your Stock Portfolio

Authors: Robert A.Weigand

1st edition

978-111863091, 1118630912, 978-1118630914