Answered step by step

Verified Expert Solution

Question

1 Approved Answer

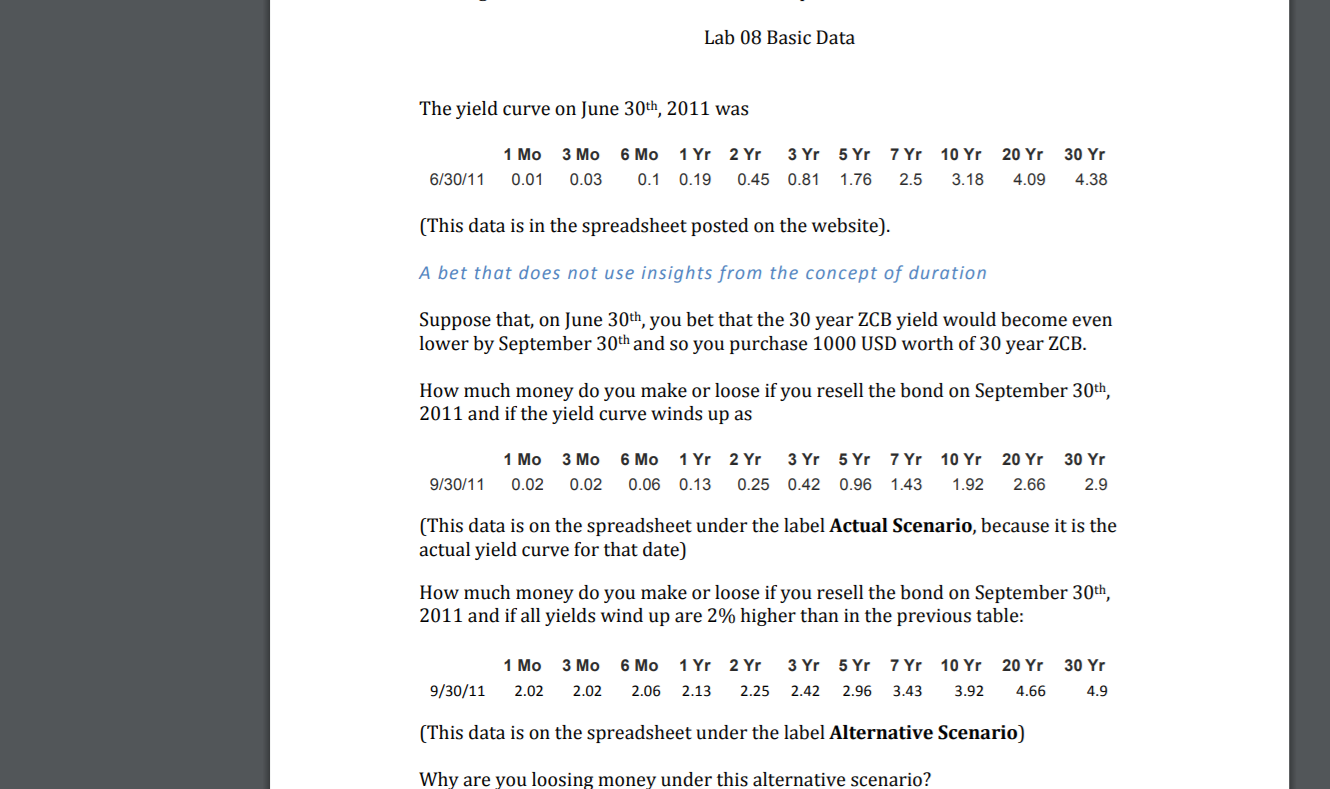

Lab 08 Basic Data The yield curve on June 30th, 2011 was 1M0 3M0 Ella 1Yr 2Yr 3Yr 5Yr TYr 10Yr 20Yr 30Yr 680111 0.01

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Multinational Finance

Authors: Michael Moffett, Arthur Stonehill, David Eiteman

6th Edition

0134472136, 978-0134472133