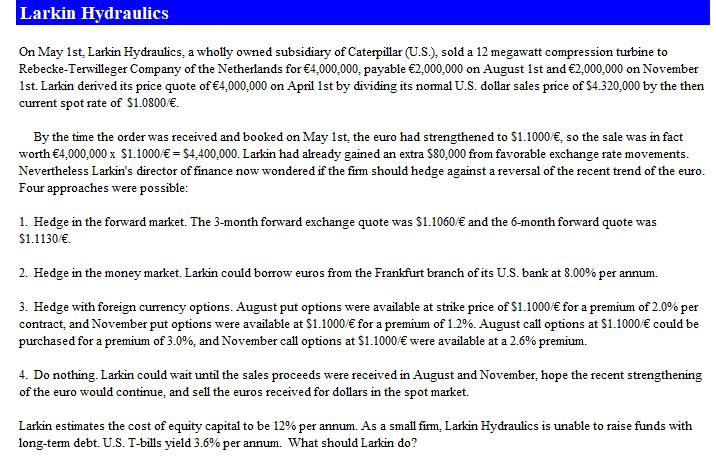

Larkin Hydraulics On May 1st, Larkin Hydraulics, a wholly owned subsidiary of Caterpillar (U.S.), sold a 12 megawatt compression turbine to Rebecke-Terwilleger Company of the Netherlands for 4.000.000. payable 2,000,000 on August 1st and 2,000,000 on November 1st. Larkin derived its price quote of 4,000,000 on April 1st by dividing its normal U.S. dollar sales price of $4.320,000 by the then current spot rate of $1.0800/. By the time the order was received and booked on May 1st, the euro had strengthened to $1.1000/, so the sale was in fact worth 4,000,000 x $1.1000/ = $4,400,000. Larkin had already gained an extra $80,000 from favorable exchange rate movements. Nevertheless Larkin's director of finance now wondered if the fimm should hedge against a reversal of the recent trend of the euro. Four approaches were possible: 1. Hedge in the forward market. The 3-month forward exchange quote was $1.1060 and the 6-month forward quote was $1.1130 . 2. Hedge in the money market. Larkin could borrow euros from the Frankfurt branch of its U.S. bank at 8.00% per annum. 3. Hedge with foreign currency options. August put options were available at strike price of $1.1000/ for a premium of 2.0% per contract, and November put options were available at $1.1000/ for a premium of 1.2% August call options at $1.1000/ could be purchased for a premium of 3.0%, and November call options at $1.1000/ were available at a 2.6% premium. 4. Do nothing. Larkin could wait until the sales proceeds were received in August and November, hope the recent strengthening of the euro would continue, and sell the euros received for dollars in the spot market. Larkin estimates the cost of equity capital to be 12% per annum. As a small firm, Larkin Hydraulics is unable to raise funds with long-term debt. U.S. T-bills yield 3.6% per annum. What should Larkin do? Larkin estimates the cost of equity capital to be 12% per annum. As a small firm, Larkin Hydraulics is unable to raise funds with long-term debt. U.S. T-bills yield 3.6% per annum. What should Larkin do? Values Today is May 1 Exchange Rate (S/) Assumptions 90-day Forward rate, S 180-day Forward rate. S US Treasury bill rate Larkin's borrowing rate, euros, per annum Larkin's cost of equity Date April 1 May 1 Strike ($/euro) Call Option Put Option Options on euros August maturity options November maturity options August Receivable November Receivable Valuation of Alternative Hedges Amount of receivable, in euros a. Hedge in the forward market Amount of receivable, in euros Respective forward rates (5 ) US dollar proceeds as hedged (5) Carry forward to Nov 1st at WACC Total USS proceeds on Nov 1st Total of both payments b. Hedge in the money market Amount of receivable, in euros Discount factor for euro funds, period Current proceeds from discounting, euros Current spot rate (5 ) Current US dollar proceeds Carry forward rate for the period US dollar proceeds on future date Total of both payments c. Hedge with options Amount of receivable, in euros Buy put options for maturities % x spot value) Carry forward for the period Premium cost carried forward to Nov 1 Gross put option value if exercised Carried forward 3 months to Nov 1 Gross proceeds, Nov 1 Total net proceeds, after premium deduction, Nov 1 d. Do nothing (remain uncovered) Amount of receivable, in euros Ending spot exchange rate (5 ) Larkin Hydraulics On May 1st, Larkin Hydraulics, a wholly owned subsidiary of Caterpillar (U.S.), sold a 12 megawatt compression turbine to Rebecke-Terwilleger Company of the Netherlands for 4.000.000. payable 2,000,000 on August 1st and 2,000,000 on November 1st. Larkin derived its price quote of 4,000,000 on April 1st by dividing its normal U.S. dollar sales price of $4.320,000 by the then current spot rate of $1.0800/. By the time the order was received and booked on May 1st, the euro had strengthened to $1.1000/, so the sale was in fact worth 4,000,000 x $1.1000/ = $4,400,000. Larkin had already gained an extra $80,000 from favorable exchange rate movements. Nevertheless Larkin's director of finance now wondered if the fimm should hedge against a reversal of the recent trend of the euro. Four approaches were possible: 1. Hedge in the forward market. The 3-month forward exchange quote was $1.1060 and the 6-month forward quote was $1.1130 . 2. Hedge in the money market. Larkin could borrow euros from the Frankfurt branch of its U.S. bank at 8.00% per annum. 3. Hedge with foreign currency options. August put options were available at strike price of $1.1000/ for a premium of 2.0% per contract, and November put options were available at $1.1000/ for a premium of 1.2% August call options at $1.1000/ could be purchased for a premium of 3.0%, and November call options at $1.1000/ were available at a 2.6% premium. 4. Do nothing. Larkin could wait until the sales proceeds were received in August and November, hope the recent strengthening of the euro would continue, and sell the euros received for dollars in the spot market. Larkin estimates the cost of equity capital to be 12% per annum. As a small firm, Larkin Hydraulics is unable to raise funds with long-term debt. U.S. T-bills yield 3.6% per annum. What should Larkin do? Larkin estimates the cost of equity capital to be 12% per annum. As a small firm, Larkin Hydraulics is unable to raise funds with long-term debt. U.S. T-bills yield 3.6% per annum. What should Larkin do? Values Today is May 1 Exchange Rate (S/) Assumptions 90-day Forward rate, S 180-day Forward rate. S US Treasury bill rate Larkin's borrowing rate, euros, per annum Larkin's cost of equity Date April 1 May 1 Strike ($/euro) Call Option Put Option Options on euros August maturity options November maturity options August Receivable November Receivable Valuation of Alternative Hedges Amount of receivable, in euros a. Hedge in the forward market Amount of receivable, in euros Respective forward rates (5 ) US dollar proceeds as hedged (5) Carry forward to Nov 1st at WACC Total USS proceeds on Nov 1st Total of both payments b. Hedge in the money market Amount of receivable, in euros Discount factor for euro funds, period Current proceeds from discounting, euros Current spot rate (5 ) Current US dollar proceeds Carry forward rate for the period US dollar proceeds on future date Total of both payments c. Hedge with options Amount of receivable, in euros Buy put options for maturities % x spot value) Carry forward for the period Premium cost carried forward to Nov 1 Gross put option value if exercised Carried forward 3 months to Nov 1 Gross proceeds, Nov 1 Total net proceeds, after premium deduction, Nov 1 d. Do nothing (remain uncovered) Amount of receivable, in euros Ending spot exchange rate (5 )