Answered step by step

Verified Expert Solution

Question

1 Approved Answer

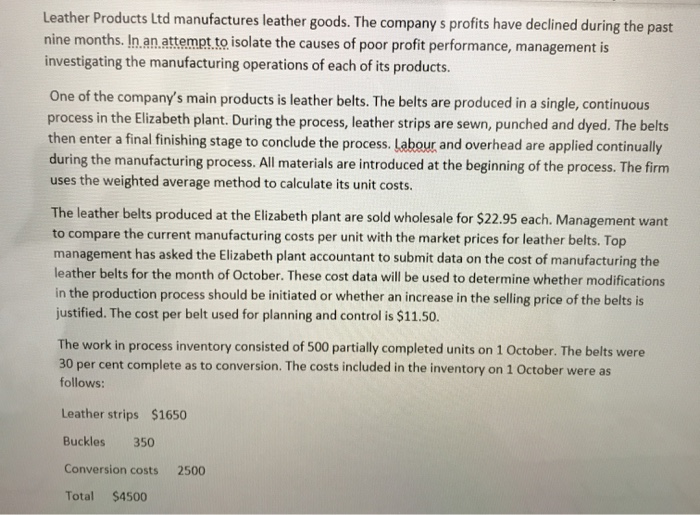

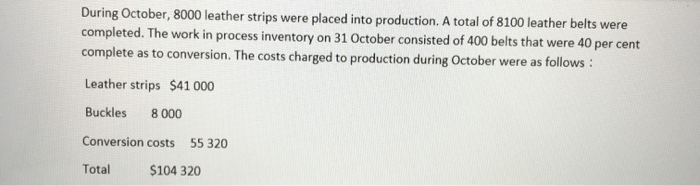

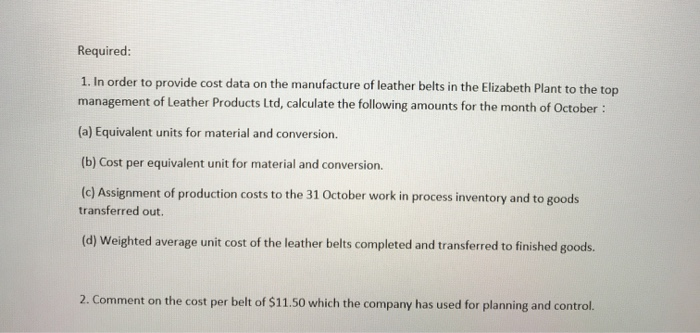

Leather Products Ltd manufactures leather goods. The company s profits have declined during the past nine months. In an attempt to isolate the causes of

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Visual Auditory And Kinesthetic Self Audit Communication And Learning Profiles

Authors: Brian Everard Walsh, Ronald Willard, Astrid Whiting

1st Edition

098666555X, 978-0986665554