Question: Lecture 2: Causality, experiments and regression @ Which of the following quantities are a causal effect and which are not? In each case, briefly explain

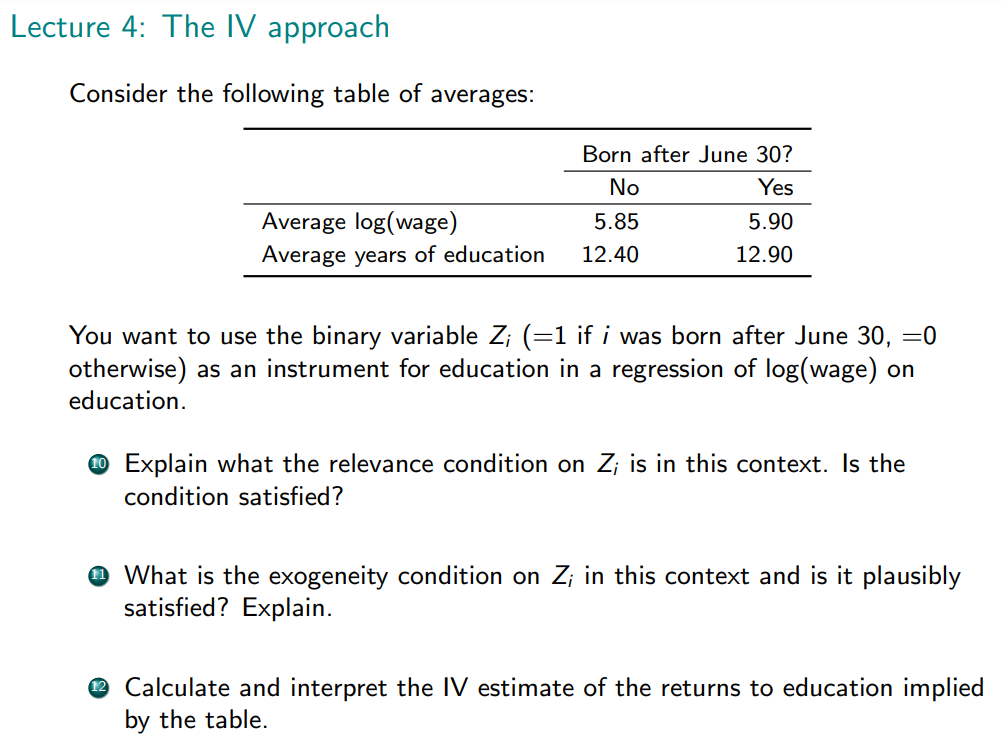

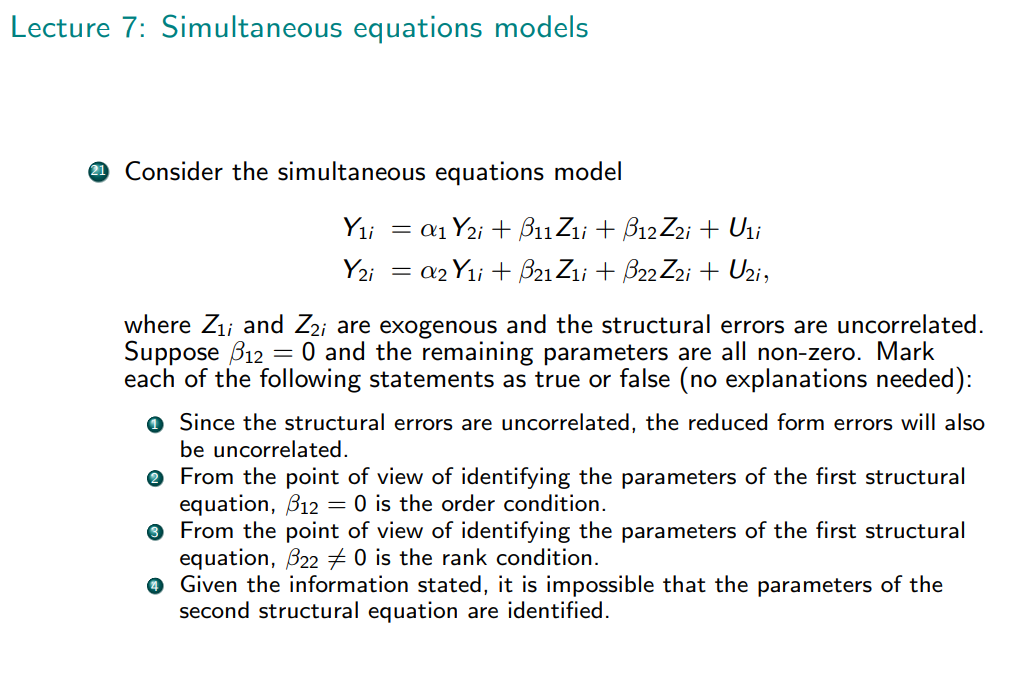

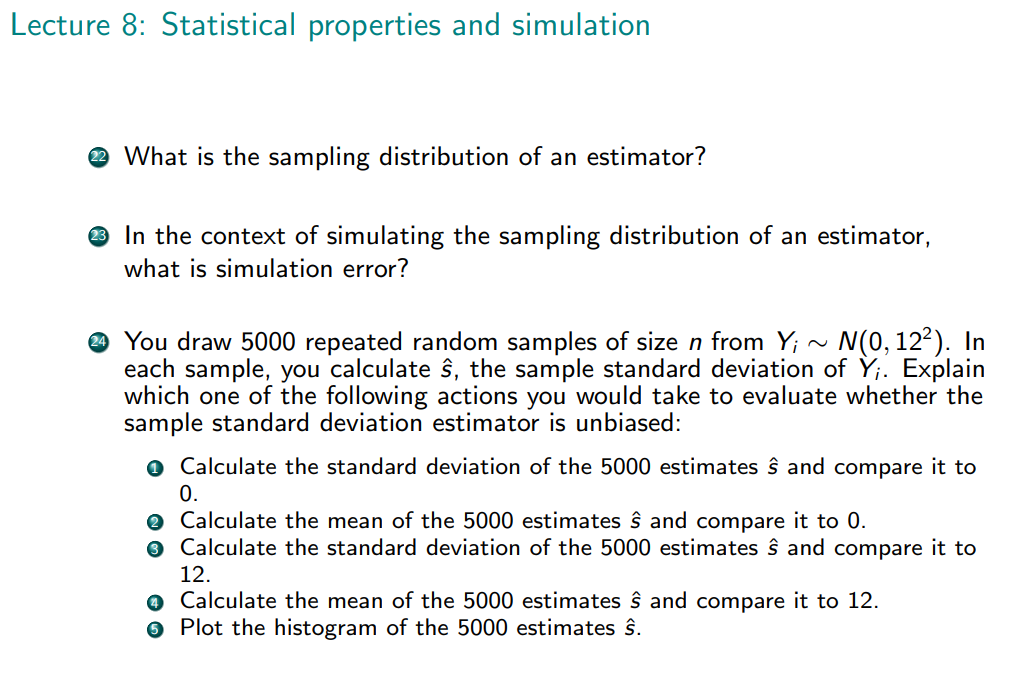

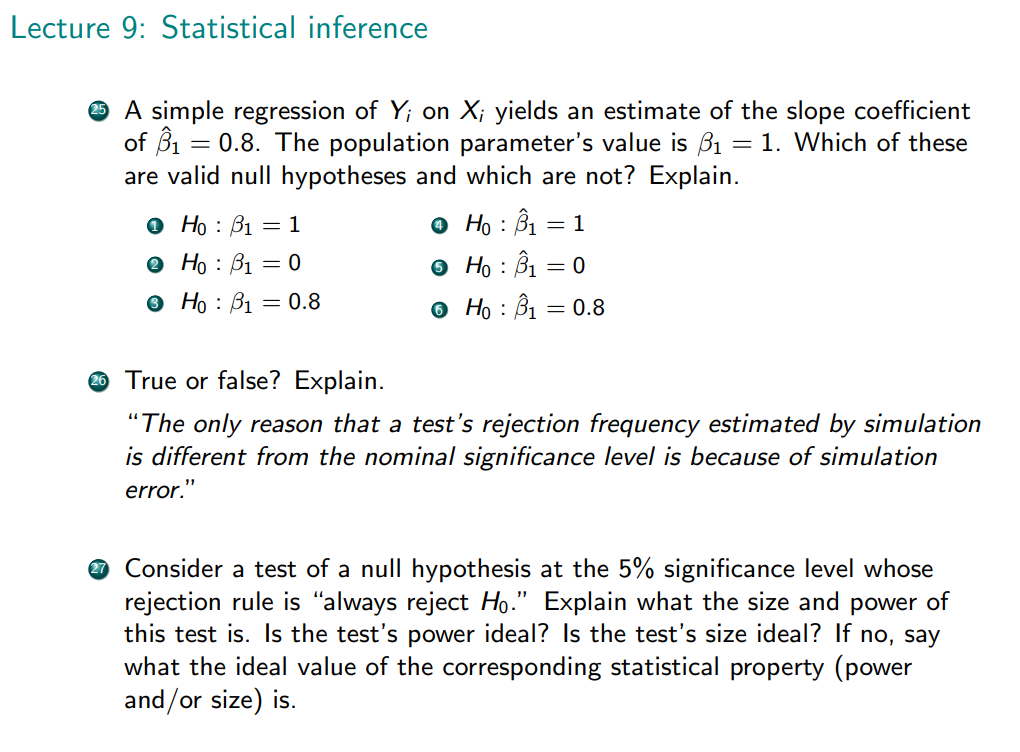

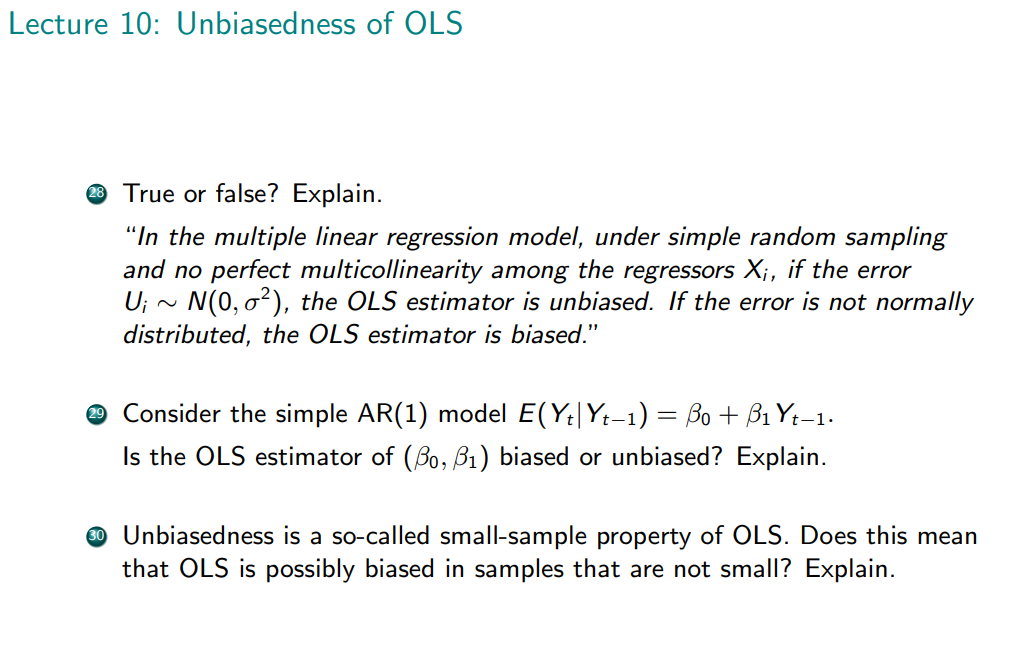

Lecture 2: Causality, experiments and regression @ Which of the following quantities are a causal effect and which are not? In each case, briefly explain why or why not. (a) E(Y1i|Xi =0) E(Yo;i|X; = 0) (b) E(Y1;|Xi =1) E(Yoi|X; =0) () E(Yi|Xi =0) E(Y;j|X; =0) @ Say if this statement is true or false, and explain why: \"When the treated (X;i = 1) would on average have a higher outcome than the non-treated (X; = 0) had nobody received the treatment, the simple difference in means, E(Y;|X; = 1) E(Y;|X; = 0), underestimates the average treatment effect on the treated.\" Let Y; = Yo + (Y1 Yoi)Xi and consider the case where Y1, Yy is the same for all /. Express the parameters and error term of the regression model Y; = Bo + 51.Xi + U; in terms of potential outcomes. Lecture 2: Regression and the CEF Q@ How does OLS choose the vector 3 in the linear regression model Y= X,'IB 'I' U_u? @ What is the relationship of the population regression function (PRF, X/j3) to the (CEF, E[Y;|Xi]) when (a) the CEF is linear? (b) the CEF is nonlinear? @ Identify which of the following statements is false and which one is true. For the false one, say which part or parts of the statement are false and why. (a) (b) \"If the error in the causal model is correlated with X;, the corresponding CEF is not causal. Consequently, the PRF, which always approximates the CEF, is not causal either." \"Regardless of whether the error in the causal model is correlated with X; or not, the CEF-error is always uncorrelated to the CEF and the PRF-error is always uncorrelated to the PRF. Therefore, the CEF and the corresponding PRF are always causal.\" Lecture 3: Long and short regression @ Suppose a short regression of Y; on Xj; is associated with a coefficient of 35 = 0. Is this situation compatible with 3f > 0? Briefly explain why or why not. Q Is this statement true or false? Explain briefly. \"Even in a randomised controlled trial it is necessary to include further control variables in a regression of Y; on the treatment, because there are many variables that affect Y; and they can cause omitted variable bias if they are not included in the regression.\" Q A regression of log(wage;) on education; gives a coefficient of 0.11. Do you think that including the variable rural; (an indicator variable that is equal to 1 if / lives in a rural area and 0 otherwise) in the regression would result in a coefficient on education; that is smaller, bigger or equal to 0.117 Explain stating your assumptions. Lecture 4: The IV approach Consider the following table of averages: Born after June 307 No Yes Average log(wage) 5.85 5.90 Average years of education 12.40 12.90 You want to use the binary variable Z; (=1 if i was born after June 30, =0 otherwise) as an instrument for education in a regression of log(wage) on education. @ Explain what the relevance condition on Z; is in this context. Is the condition satisfied? @ What is the exogeneity condition on Z; in this context and is it plausibly satisfied? Explain. @ Calculate and interpret the |V estimate of the returns to education implied by the table. Lecture 5: Two-stage least squares @ Consider the following equations: Y, = Po+ b/ Xi+ Palhi 4+ U; Xi = mo+mdbi+ Vi, where the first equation represents a causal model where X; is endogenous and Z;; is exogenous and all parameters are different from zero. In the second equation, m1 # 0 and E(V;|Z:;) = 0. Show why Z;; can or can't be used as an instrument to estimate the parameters of the causal model by 2518, @ Consider the following equations: Yi = bBo+/Xi+ B2+ U; Xi = mo+mdbi+ Vi, where the first equation represents a causal model where X; is endogenous and Z;; is exogenous and 32 = 0. In the second equation, m # 0 and E(V;|Zii) = 0. Show why Z;; can or can't be used as an instrument to estimate the parameters of the causal model by 2SLS. Lecture 5: Two-stage least squares Consider the following equation: Yi = Bo + BIXi + B2Z1i + U; where the first equation represents a causal model where X; is endogenous and Z1; is exogenous and all parameters are different from zero. In addition to Z1, you have access to two further exogenous variables, (Z2i, Z3;). Give the first stage equation of the 2SLS procedure that uses (Z2i, Z3i) as instruments for X;, and state the relevance condition in terms of first-stage parameters.Lecture 6: Matrices; measurement error @ Is this statement true or false? Explain briefly. \"When we represent the IV estimator as 3"V = (Z'X)7'Z'Y, Y is the vector containing the outcome variable, Z is a matrix whose columns contain all exogenous regressors and X is a matrix whose columns contain all the endogenous regressors." @ Is this statement true or false? Explain briefly. \"It is possible to compute the 25LS estimator directly without first computing the first stage.\" @ Consider the causal model Yi=PB+ 68X+ U, EU|X")=0, but we only observe a noisy measure of X", Xi = X;" + ;, where ; follows the classical errors-in-variables (CEV) assumptions. Thus, the corresponding observational model is Y; = 8o + 51 Xi + U:, with 0; = U; Biei. A second noisy measure of X" is available, Z; = X" + v;, with v; also following the CEV assumptions. Explain why Z; satisfies the IV exogeneity assumption in the observational model. That is, explain why Covl Z:.-U;) =0. Lecture 7: Simultaneous equations models Consider the simultaneous equations model Yli = a1 Y2i + Uli Yzi = 02 Ylit Uzi, where C(Uli, Uzi) = 0 and 0 0 or

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Mathematics Questions!