Answered step by step

Verified Expert Solution

Question

1 Approved Answer

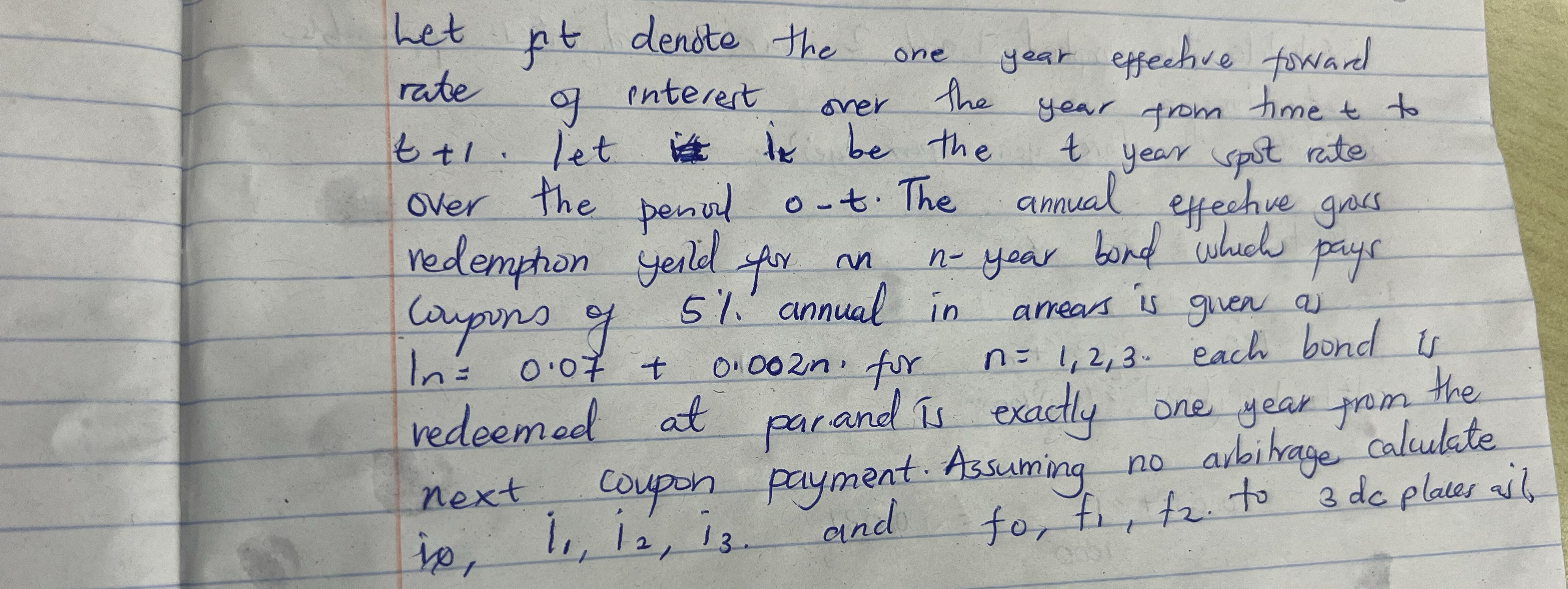

Let ft denote the one year effective foward rate of interest over the year from time to t + 1 . let it be the

Let ft denote the one year effective foward

rate of interest over the year from time to

let it be the year spot rate

over the pEriod The annual effective grass

redemption yeild for in year bond which pays

coupons of annual in arreas is given as

in n for each bond is

redeemed at par.and is exactly one year jrom the

next coupon payment. Assuming no arbitrage calculate

and to Decimal places

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The History Of Lloyd S And Of Marine Insurance In Great Britain

Authors: Frederick Martin

1st Edition

1421206269, 978-1421206264