Answered step by step

Verified Expert Solution

Question

1 Approved Answer

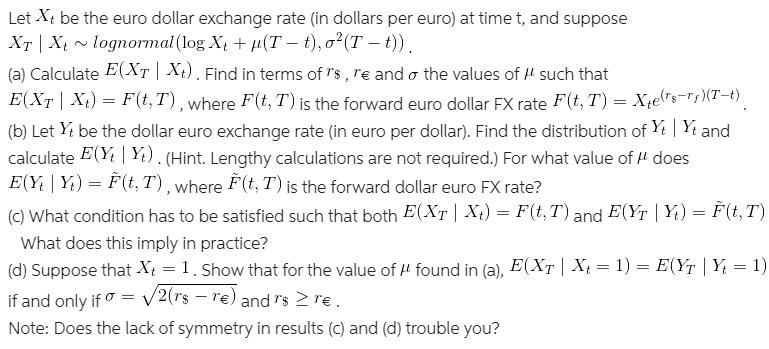

Let Xt be the euro dollar exchange rate (in dollars per euro) at time t, and suppose XT | Xt lognormal (log X +

Let Xt be the euro dollar exchange rate (in dollars per euro) at time t, and suppose XT | Xt lognormal (log X + (Tt), o (T-t)). (a) Calculate E(XT | Xt). Find in terms of rs, re and of the values of such that E(XT | Xt) = F(t,T), where F(t, T) is the forward euro dollar FX rate F(t,T) = Xe(s-)(T-t) (b) Let Yt be the dollar euro exchange rate (in euro per dollar). Find the distribution of Yt | Y and calculate E(YY). (Hint. Lengthy calculations are not required.) For what value of does E(YY)= F(t, T), where F(t, T) is the forward dollar euro FX rate? (c) What condition has to be satisfied such that both E(XT | Xt) = F(t, T) and E(YT | Yt) = F(t, T) What does this imply in practice? (d) Suppose that X = 1. Show that for the value of found in (a), E(XT | Xt = 1) = E(YT | Yt = 1) if and only if = 2(rs-re) and rs >re. Note: Does the lack of symmetry in results (c) and (d) trouble you?

Step by Step Solution

★★★★★

3.53 Rating (153 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introductory Econometrics A Modern Approach

Authors: Jeffrey Wooldridge

7th Edition

1337558869, 978-1337558860