Answered step by step

Verified Expert Solution

Question

1 Approved Answer

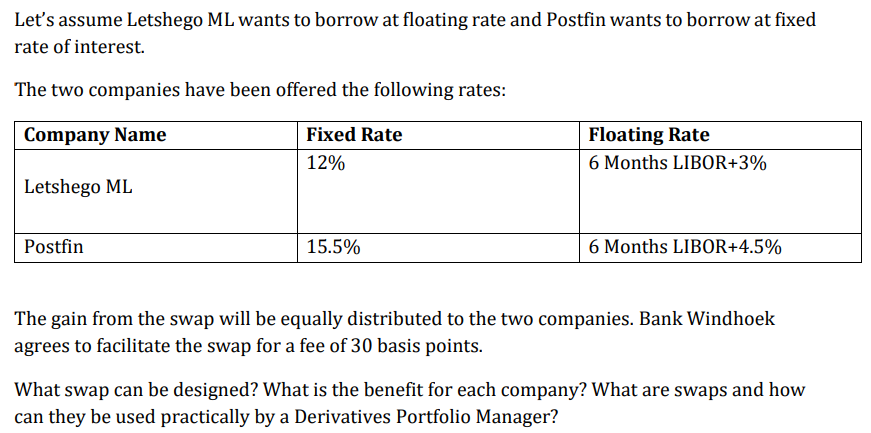

Let's assume Letshego ML wants to borrow at floating rate and Postfin wants to borrow at fixed rate of interest. The two companies have

Let's assume Letshego ML wants to borrow at floating rate and Postfin wants to borrow at fixed rate of interest. The two companies have been offered the following rates: Company Name Letshego ML Postfin Fixed Rate 12% 15.5% Floating Rate 6 Months LIBOR+3% 6 Months LIBOR+4.5% The gain from the swap will be equally distributed to the two companies. Bank Windhoek agrees to facilitate the swap for a fee of 30 basis points. What swap can be designed? What is the benefit for each company? What are swaps and how can they be used practically by a Derivatives Portfolio Manager?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

A plain vanilla interest rate swap can be designed where Letshego ML pays a fixed rate of 12 to Post...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Finance Principles And Practice

Authors: Denzil Watson, Antony Head

9th Edition

1292450940, 978-1292450940