Question

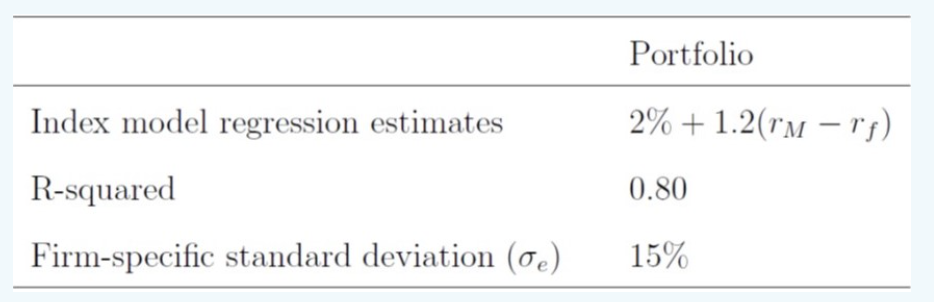

Let's evaluate the performance of this team after two months. Assume the following (excess return) index-model regression results for this team's portfolio. The risk-free rate

Let's evaluate the performance of this team after two months. Assume the following (excess return) index-model regression results for this team's portfolio. The risk-free rate over the period was 5%. The market's average return was 15%.

Please calculate the M2 for the team's portfolio and evaluate the performance relative to the market index. (Note: this is a challenging question and you have sufficient information to solve this question.)

Index model regression estimates R-squared Firm-specific standard deviation (de) Portfolio 2% +1.2(TM-T) 0.80 15% Index model regression estimates R-squared Firm-specific standard deviation (de) Portfolio 2% +1.2(TM-T) 0.80 15%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Banker To The World

Authors: William Rhodes

1st Edition

0071704256, 978-0071704250