Answered step by step

Verified Expert Solution

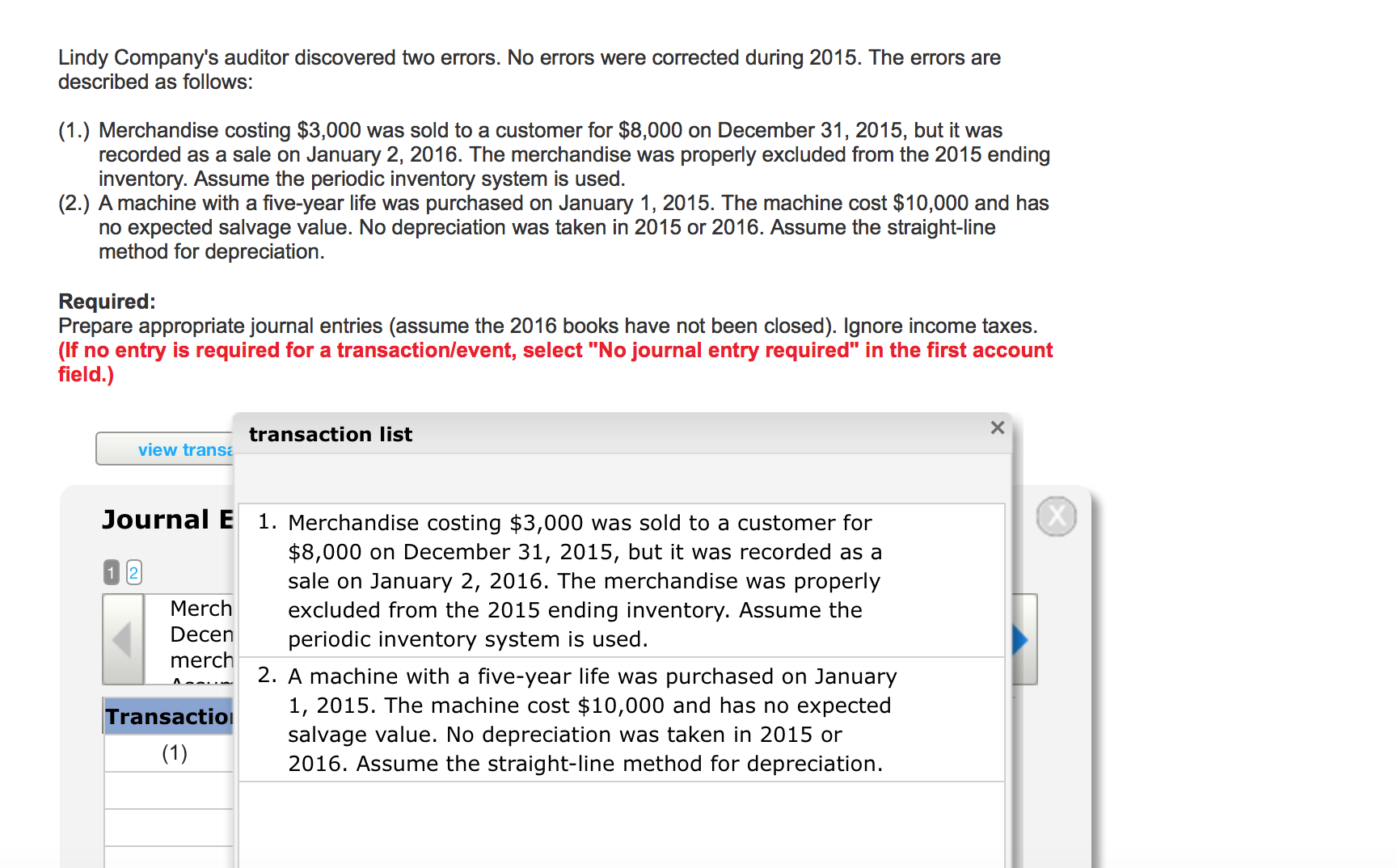

Question

1 Approved Answer

Lindy Company's auditor discovered two errors. No errors were corrected during 2015. The errors are described as follows: Merchandise costing $3,000 was sold to a

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments Unlimited A Novel About DevOps Security Audit Compliance And Thriving In The Digital Age

Authors: Helen Beal, Bill Bensing, Jason Cox, Michael Edenzon, John Willis

1st Edition

1950508536, 978-1950508532