Answered step by step

Verified Expert Solution

Question

1 Approved Answer

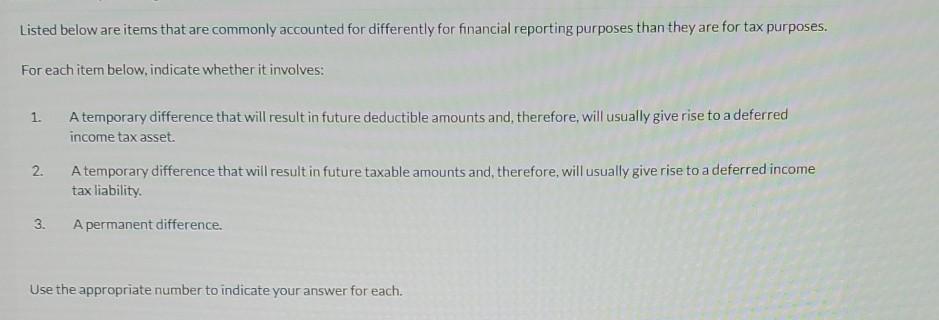

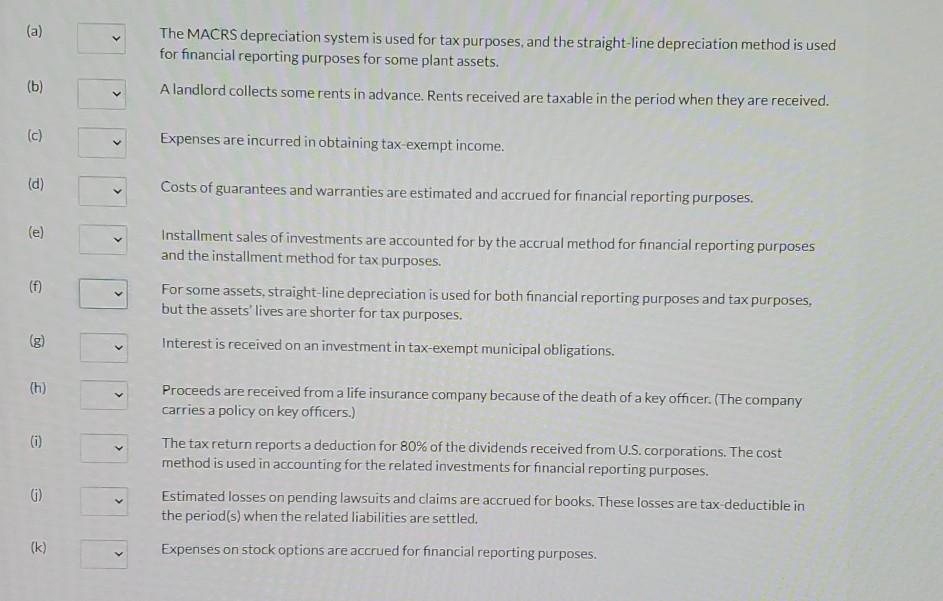

Listed below are items that are commonly accounted for differently for financial reporting purposes than they are for tax purposes. For each item below. indicate

Listed below are items that are commonly accounted for differently for financial reporting purposes than they are for tax purposes. For each item below. indicate whether it involves: 1. A temporary difference that will result in future deductible amounts and therefore, will usually give rise to a deferred income tax asset A temporary difference that will result in future taxable amounts and therefore, will usually give rise to a deferred income tax liability. 2. 3. A permanent difference. Use the appropriate number to indicate your answer for each. (a) (e) > Installment sales of investments are accounted for by the accrual method for financial reporting purposes and the installment method for tax purposes. For some assets, straight-line depreciation is used for both financial reporting purposes and tax purposes, but the assets' lives are shorter for tax purposes. (f) (8) (h) Proceeds are received from a life insurance company because of the death of a key officer. (The company carries a policy on key officers.) 0 The tax return reports a deduction for 80% of the dividends received from U.S. corporations. The cost method is used in accounting for the related investments for financial reporting purposes. Estimated losses on pending lawsuits and claims are accrued for books. These losses are tax deductible in the period(s) when the related liabilities are settled. 0) (k) Expenses on stock options are accrued for financial reporting purposes

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Guide To The National Initiative For Cybersecurity Education NICE Cybersecurity Workforce Framework 2.0 Internal Audit And IT Audit

Authors: Dan Shoemaker, Anne Kohnke, Ken Sigler

1st Edition

0367658623, 978-0367658625