Answered step by step

Verified Expert Solution

Question

1 Approved Answer

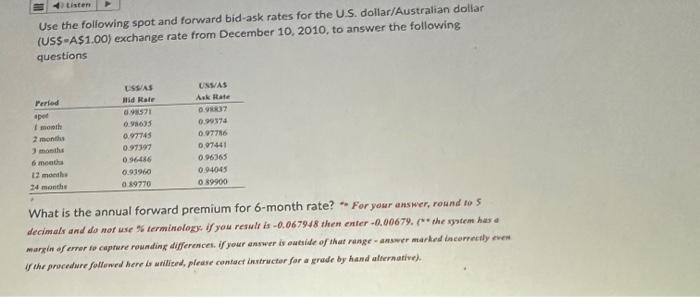

Listen Use the following spot and forward bid-ask rates for the U.S. dollar/Australian dollar (US$-A$1.00) exchange rate from December 10, 2010, to answer the following

Listen Use the following spot and forward bid-ask rates for the U.S. dollar/Australian dollar (US$-A$1.00) exchange rate from December 10, 2010, to answer the following questions Period spot 1 month 2 months 3 months 6 months 12 months 24 months USS/AS Bid Rate 0.98571 0.98635 0.97745 0.97397 0.96486 0.93960 0.89770 USS/AS Ask Rate 0.98837 0.99374 0.97786 0.97441 0.96365 0.94045 0.89900 What is the annual forward premium for 6-month rate? **For your answer, round to 5 decimals and do not use % terminology. if you result is -0.067948 then enter -0.00679. (** the system has a margin of error to capture rounding differences. if your answer is outside of that range answer marked incorrectly even if the procedure followed here is utilized, please contact instructor for a grade by hand alternative).

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Nasdaq And Us30 Ultimate Day Trading Strategy

Authors: James Jecool King

1st Edition

979-8367719499