Answered step by step

Verified Expert Solution

Question

1 Approved Answer

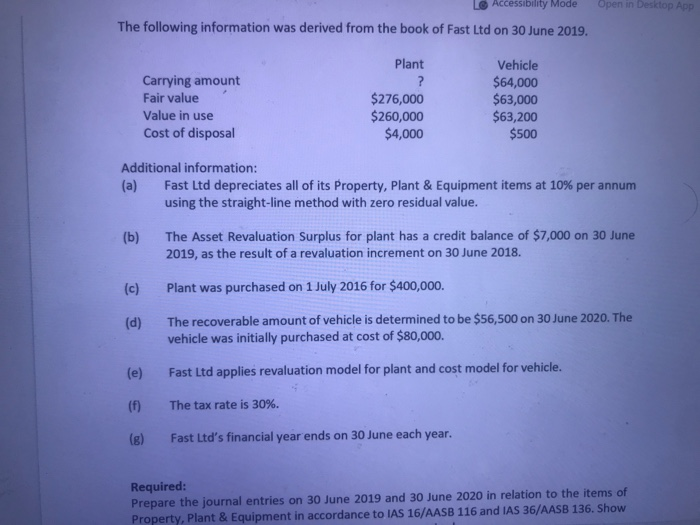

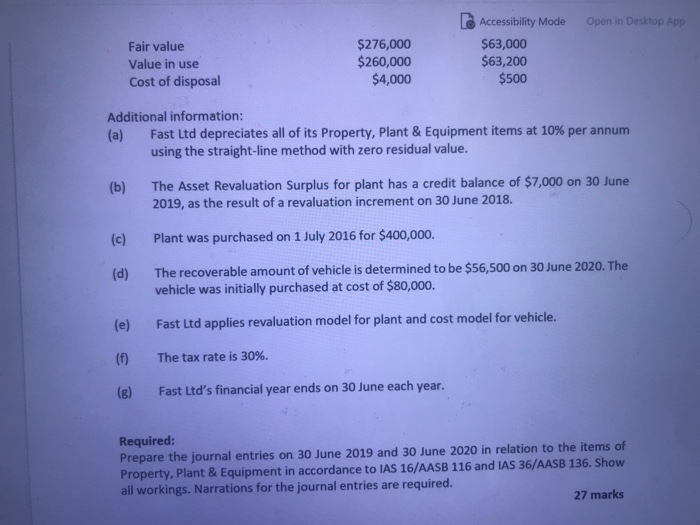

Lo Accessibility Mode Open in Desktop App The following information was derived from the book of Fast Ltd on 30 June 2019. Plant Carrying amount

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting For Managers Interpreting Accounting Information For Decision Making

Authors: Paul M. Collier

5th Edition

111900294X, 978-1119002949