Answered step by step

Verified Expert Solution

Question

1 Approved Answer

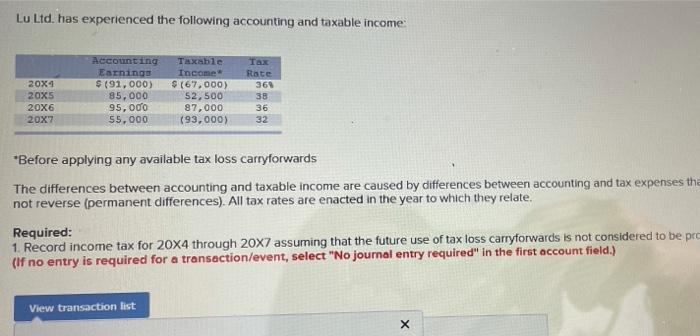

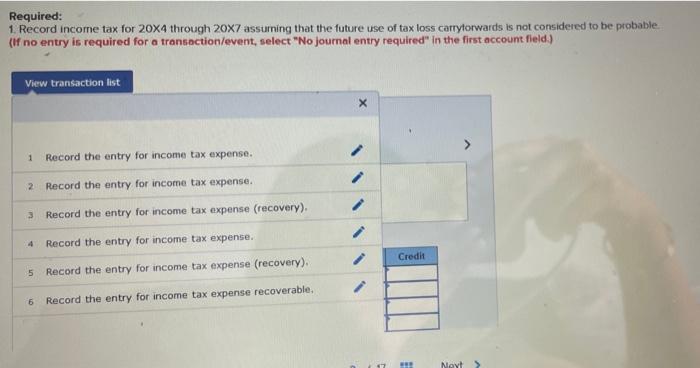

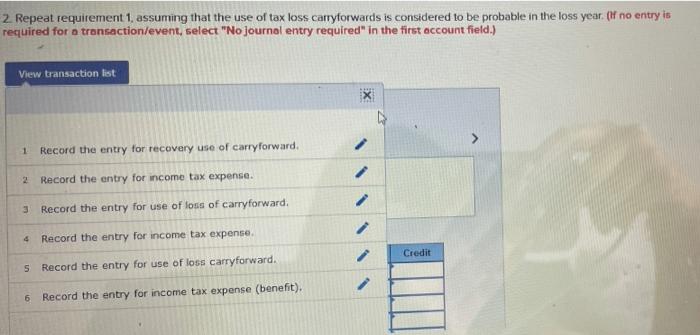

Lu Ltd. has experienced the following accounting and taxable income: 20x4 20X5 20X6 20X7 Accounting Earnings $ (91, 000) 85,000 95,000 55,000 Taxable Income $(67,000)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Loose Leaf Fundamental Financial Accounting Concepts

Authors: Thomas Edmonds, Frances McNair, Philip Olds

8th Edition

0077433807, 978-0077433802