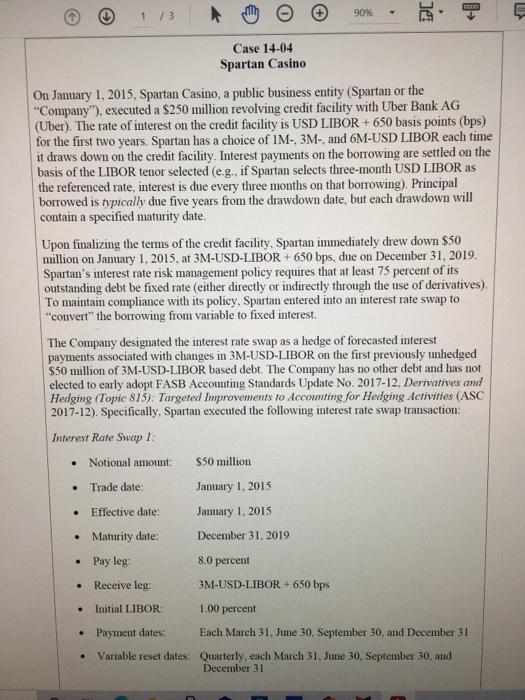

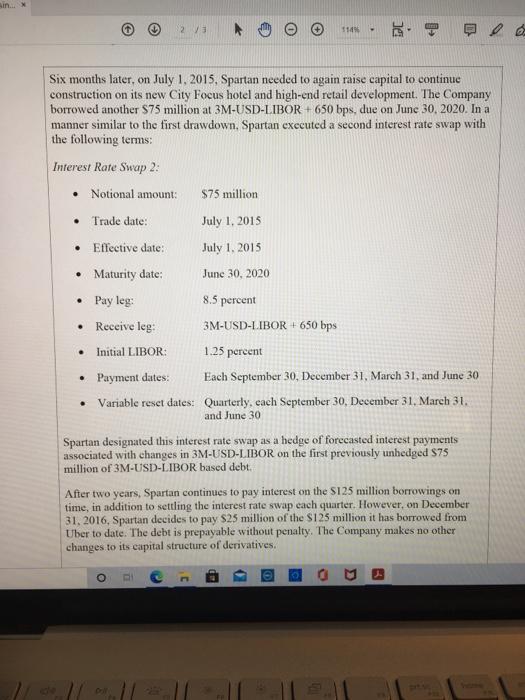

m 90% 1 / 3 . US Case 14-04 Spartan Casino On January 1, 2015, Spartan Casino, a public business entity (Spartan or the "Company"), executed a $250 million revolving credit facility with Uber Bank AG (Uber). The rate of interest on the credit facility is USD LIBOR +650 basis points (bps) for the first two years. Spartan has a choice of IM-, 3M-, and 6M-USD LIBOR each time it draws down on the credit facility. Interest payments on the borrowing are settled on the basis of the LIBOR tenor selected (e.g., if Spartan selects three-month USD LIBOR as the referenced rate, interest is due every three months on that borrowing). Principal borrowed is typically due five years from the drawdown date, but each drawdown will contain a specified maturity date. Upon finalizing the terms of the credit facility, Spartan immediately drew down $50 million on January 1, 2015 at 3M-USD-LIBOR +650 bps, due on December 31, 2019. Spartan's interest rate risk management policy requires that at least 75 percent of its outstanding debt be fixed rate (either directly or indirectly through the use of derivatives), To maintain compliance with its policy, Spartan entered into an interest rate swap to "convert" the borrowing from variable to fixed interest. The Company designated the interest rate swap as a hedge of forecasted interest payments associated with changes in 3M-USD-LIBOR on the first previously unhedged $50 million of 3M-USD-LIBOR based debt. The Company has no other debt and has not elected to eatly adopt FASB Accounting Standards Update No. 2017-12. Derivatives and Hedging (Topic 815). Targeted Improvements to Accounting for Hedging Activities (ASC 2017-12). Specifically, Spartan executed the following interest rate swap transaction: Interest Rate Swap 1: . Notional amount: $50 million . . Trade date: January 1, 2015 Effective date: January 1, 2015 Maturity date: December 31, 2019 Pay leg 8.0 percent Receive leg: 3M-USD-LIBOR + 650 bps Initial LIBOR: 1.00 percent Payment dates: Each March 31. Jme 30, September 30, and December 31 Variable reset dates: Quarterly, each March 31. June 30. September 30, and December 31 . . . Sin... 23 1145 D Six months later, on July 1, 2015, Spartan needed to again raise capital to continue construction on its new City Focus hotel and high-end retail development. The Company borrowed another $75 million at 3M-USD-LIBOR +650 bps. due on June 30, 2020. In a manner similar to the first drawdown. Spartan executed a second interest rate swap with the following terms: Interest Rate Swap 2: Notional amount: $75 million Trade date: July 1, 2015 Effective date: July 1, 2015 Maturity date: June 30, 2020 Pay leg: 8.5 percent Receive leg: 3M-USD-LIBOR +650 bps Initial LIBOR: 1.25 pereent Payment dates: Each September 30, December 31, March 31, and June 30 Variable reset dates: Quarterly, each September 30, December 31, March 31, and June 30 Spartan designated this interest rate swap as a hedge of forecasted interest payments associated with changes in 3M-USD-LIBOR on the first previously unhedged $75 million of 3M-USD-LIBOR based debt. After two years, Spartan continues to pay interest on the S125 million borrowings on time, in addition to settling the interest rate swap each quarter. However, on December 31, 2016, Spartan decides to pay $25 million of the S125 million it has borrowed from Uber to date. The debt is prepayable without penalty. The Company makes no other changes to its capital structure of derivatives. a O 71 A. Explain the issue as you see it and what challenges there are in addressing the matter in this specific instance and more broadly. B. Ultimately you must decide on how you want to treat the issue and support your decision with relevant research and citations which you feel support your argument. C. link directly to any accounting standards or sources of information you use in your analysis. 3 1 C m 90% 1 / 3 . US Case 14-04 Spartan Casino On January 1, 2015, Spartan Casino, a public business entity (Spartan or the "Company"), executed a $250 million revolving credit facility with Uber Bank AG (Uber). The rate of interest on the credit facility is USD LIBOR +650 basis points (bps) for the first two years. Spartan has a choice of IM-, 3M-, and 6M-USD LIBOR each time it draws down on the credit facility. Interest payments on the borrowing are settled on the basis of the LIBOR tenor selected (e.g., if Spartan selects three-month USD LIBOR as the referenced rate, interest is due every three months on that borrowing). Principal borrowed is typically due five years from the drawdown date, but each drawdown will contain a specified maturity date. Upon finalizing the terms of the credit facility, Spartan immediately drew down $50 million on January 1, 2015 at 3M-USD-LIBOR +650 bps, due on December 31, 2019. Spartan's interest rate risk management policy requires that at least 75 percent of its outstanding debt be fixed rate (either directly or indirectly through the use of derivatives), To maintain compliance with its policy, Spartan entered into an interest rate swap to "convert" the borrowing from variable to fixed interest. The Company designated the interest rate swap as a hedge of forecasted interest payments associated with changes in 3M-USD-LIBOR on the first previously unhedged $50 million of 3M-USD-LIBOR based debt. The Company has no other debt and has not elected to eatly adopt FASB Accounting Standards Update No. 2017-12. Derivatives and Hedging (Topic 815). Targeted Improvements to Accounting for Hedging Activities (ASC 2017-12). Specifically, Spartan executed the following interest rate swap transaction: Interest Rate Swap 1: . Notional amount: $50 million . . Trade date: January 1, 2015 Effective date: January 1, 2015 Maturity date: December 31, 2019 Pay leg 8.0 percent Receive leg: 3M-USD-LIBOR + 650 bps Initial LIBOR: 1.00 percent Payment dates: Each March 31. Jme 30, September 30, and December 31 Variable reset dates: Quarterly, each March 31. June 30. September 30, and December 31 . . . Sin... 23 1145 D Six months later, on July 1, 2015, Spartan needed to again raise capital to continue construction on its new City Focus hotel and high-end retail development. The Company borrowed another $75 million at 3M-USD-LIBOR +650 bps. due on June 30, 2020. In a manner similar to the first drawdown. Spartan executed a second interest rate swap with the following terms: Interest Rate Swap 2: Notional amount: $75 million Trade date: July 1, 2015 Effective date: July 1, 2015 Maturity date: June 30, 2020 Pay leg: 8.5 percent Receive leg: 3M-USD-LIBOR +650 bps Initial LIBOR: 1.25 pereent Payment dates: Each September 30, December 31, March 31, and June 30 Variable reset dates: Quarterly, each September 30, December 31, March 31, and June 30 Spartan designated this interest rate swap as a hedge of forecasted interest payments associated with changes in 3M-USD-LIBOR on the first previously unhedged $75 million of 3M-USD-LIBOR based debt. After two years, Spartan continues to pay interest on the S125 million borrowings on time, in addition to settling the interest rate swap each quarter. However, on December 31, 2016, Spartan decides to pay $25 million of the S125 million it has borrowed from Uber to date. The debt is prepayable without penalty. The Company makes no other changes to its capital structure of derivatives. a O 71 A. Explain the issue as you see it and what challenges there are in addressing the matter in this specific instance and more broadly. B. Ultimately you must decide on how you want to treat the issue and support your decision with relevant research and citations which you feel support your argument. C. link directly to any accounting standards or sources of information you use in your analysis. 3 1 C