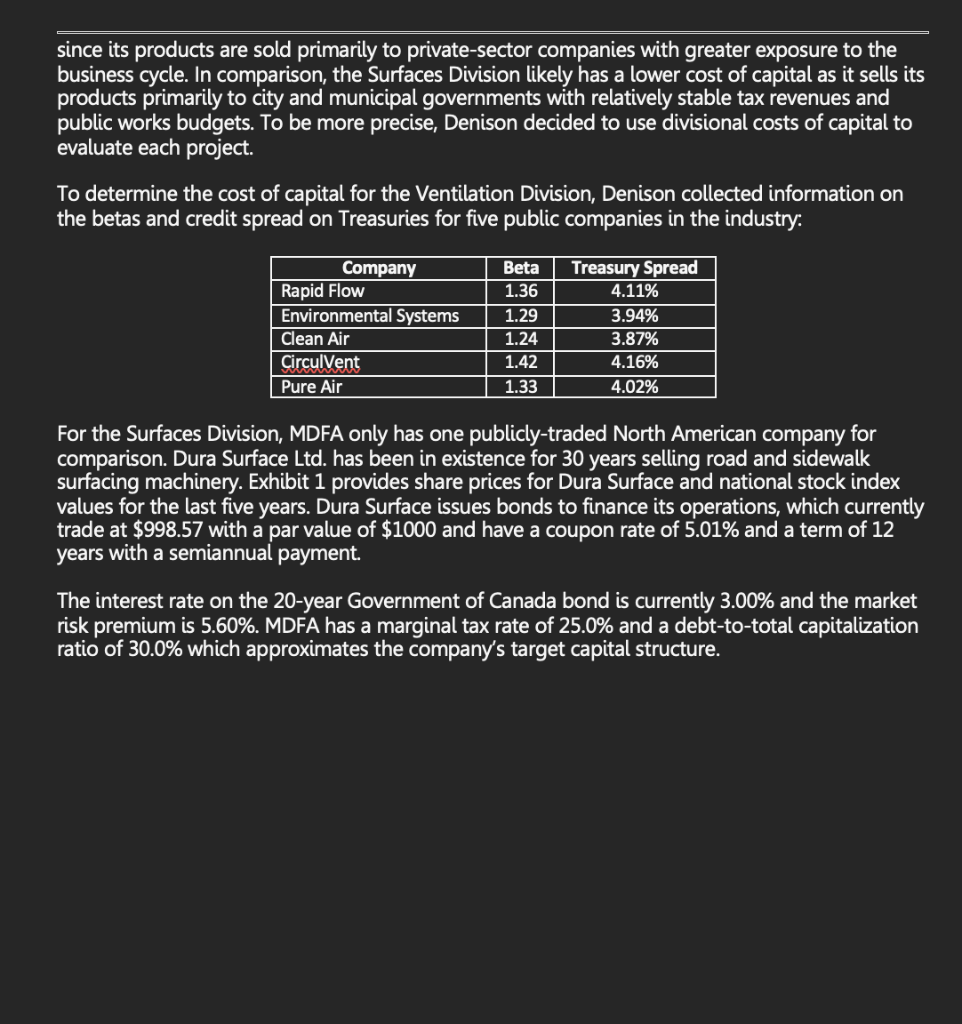

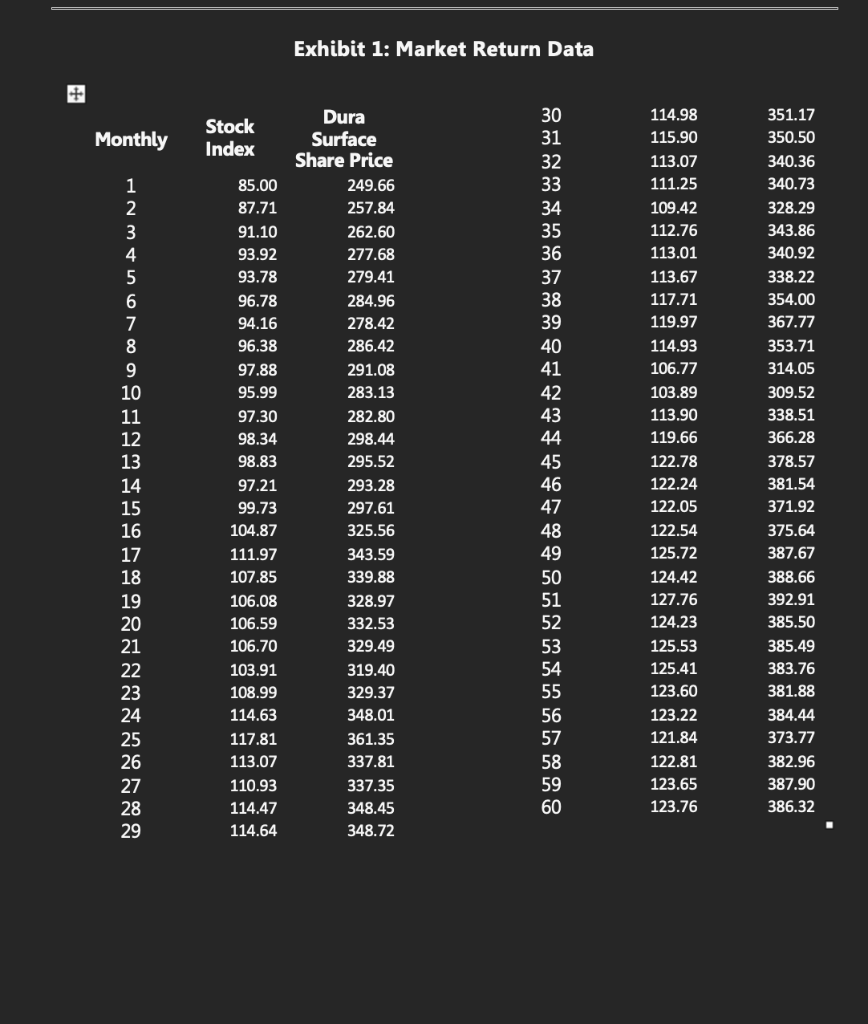

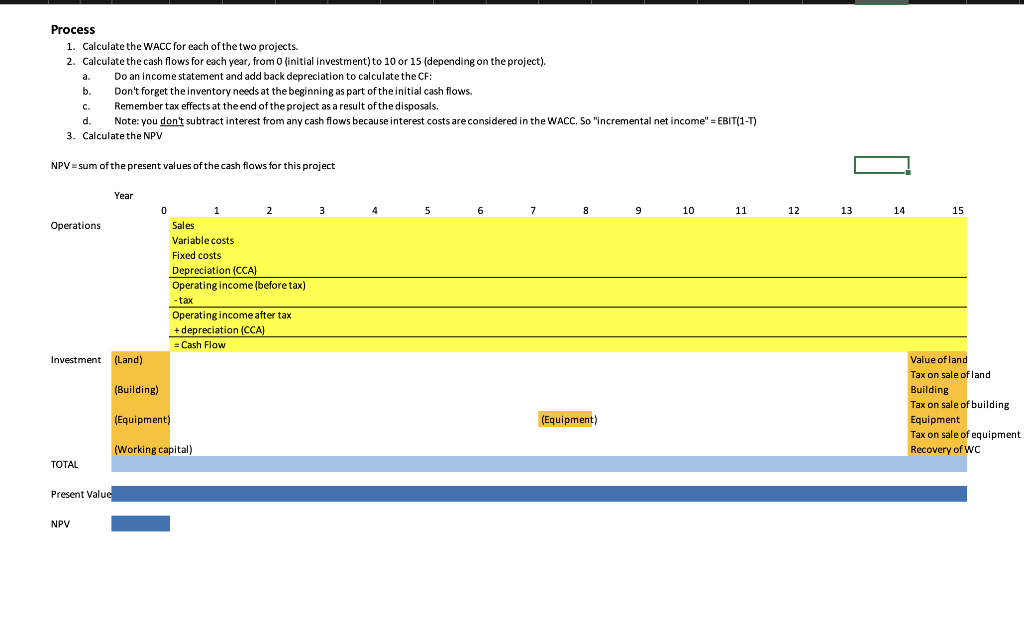

Machine Design and Factory Automation Hailey Denison, CPA, has recently accepted a position as a financial analyst with Machine Design and Factory Automation (MDFA) Ltd. Reporting to Dexter Reid, P. Eng., Vice-President of New Product Development, Denison is responsible for preparing detailed feasibility studies of all new products to determine if they are commercially viable prior to being approved for launch. Company policy requires that analysts use the net present value (NPV) method. Product Review Process MDFA is an industrial equipment design and manufacturing firm with a reputation for providing its customers with innovative solutions to complex operational problems. The company is divided into three business units: - the Ventilation Division produces heating, cooling, and air purification systems: - the Surfaces Division makes equipment used to surface roads and pedestrian walkways; and - the Factory Automation Division manufactures machine tools and system integration software. MDFA's divisions are autonomous and are expected to work closely with current and prospective customers to originate new product proposals. These proposals are presented to MDFA's New Product Screening Committee (NPSC) for approval in three stages. In the first stage, the division tries to convince the NPSC of the product's technical and commercial potential in general terms. If approved, the NPSC provides funding to design a prototype. In the second stage, the prototype is reviewed to determine if it is technically viable. The product is normally sent back to the division for further refinements based on input from the committee. If these issues are addressed successfully, the product moves on to stage 3 where a detailed feasibility study of the commercial viability of the new product is completed by an independent financial analyst from the Office of the Vice-President of New Product Development. If approved at stage 3, the division receives funding to launch the product. Once a new product is launched, each division must provide a monthly progress report to the NPSC where the committee can decide to maintain, increase, decrease or discontinue funding based on their progress. The new product approval and monitoring processes at MDFA are rigorous, and divisional managers and financial analysts know to be well prepared whenever they present to the NPSC. New Product Proposals Denison is currently preparing two new product feasibility studies. One product is an industrial air filtration system that is used in sawmills and grain storage terminals. Wood and grain particles pose serious health and safety concerns for employees in these facilities if not properly controlled. Numerous systems are available to keep particle counts to an acceptable level, but MDFA has designed a new system based on vacuum cleaner technology that extracts and bags the particles and allows the clients to recycle them as inputs in particle board manufacturing and as animal feed. The second product is an automated paving stone installer. Increasingly cities are substituting paving stones for concrete when installing pedestrian walkways. Not only are paving stones visually more appealing than concrete or pebbled aggregate, they do not crack in the winter months, can be easily repaired if damaged, and can be moved and then replaced in order to access water and sewage services. Ventilation Division: Industrial Air Filtration System (IAFS) Projections The Ventilation Division will manufacture the IAFS using idle facilities. This plant can produce up to 260 units per year over the product's 10-year life. An outside appraiser indicated that the plant is worth $3,000,000, which breaks down as $1,400,000 for the land and $1,600,000 for the building. New production equipment costing $5,800,000 is also required. It is believed that the land will have a residual value of $1,800,000 at the end of the project's life, while the building and equipment will be worth $500,000 and $250,000. The building is subject to a CCA rate of 4.0% and the equipment is subject to a CCA rate of 20.0%. Incremental net working capital of $600,000 is also needed which will be liquidated at the end of the product's life. IAFS sales are estimated to be 70 units in the first year and will grow by 25.0% a year until plant capacity is reached. The unit price is $120,000 and unit costs are $100,000 per unit, which includes direct materials, direct labour, and manufacturing overhead. The Ventilation Division must also pay a $10,000 licensing fee per unit for the vacuum cleaner technology. Incremental selling and administration costs will be $350,000 per year. Automated Paving Stone Installer (APSI) Projections A new factory is needed to manufacture the APSI. The facility can produce up to 300 machines each year over the product's 15-year life. A parcel of land worth $400,000 will be purchased, and a building constructed for $1,800,000. Equipment costing $3,500,000 is also be required. At the end of the project's life, it is estimated the land can be sold for $780,000, while the building will have a residual value of $620,000 and the equipment's residual value will be negligible (i.e., zero). Building and equipment costs are subject to CCA rates of 4.0% and 20.0% respectfully. An investment of $370,000 in net working capital is needed to support production that will be liquidated at the end of the product's life. APSI sales are forecasted to be 100 units in the first year, 150 in the second year, 200 in the third year, 250 in the fourth year, and then reach factory capacity of 300 units in the fifth year. The product's list price is $350,000 and its unit cost is $340,000, which includes direct materials, direct labour and factory overhead. Incremental selling and administration costs to support the business will be $1,600,000. Existing corporate overhead of $230,000 per year will be allocated to the product as per company policy. Factory equipment will be overhauled at a cost of $1,500,000 at the end of year 8 . Discount Rate In the past, MDFA used a corporate cost of capital to evaluate the feasibility of its new product proposals. Denison felt this rate was inaccurate as it reflected the weighted-average cost of capital of the three MDFA divisions. The Ventilation Division likely has a higher cost of capital since its products are sold primarily to private-sector companies with greater exposure to the business cycle. In comparison, the Surfaces Division likely has a lower cost of capital as it sells its products primarily to city and municipal governments with relatively stable tax revenues and public works budgets. To be more precise, Denison decided to use divisional costs of capital to evaluate each project. To determine the cost of capital for the Ventilation Division, Denison collected information on the betas and credit spread on Treasuries for five public companies in the industry: For the Surfaces Division, MDFA only has one publicly-traded North American company for comparison. Dura Surface Ltd. has been in existence for 30 years selling road and sidewalk surfacing machinery. Exhibit 1 provides share prices for Dura Surface and national stock index values for the last five years. Dura Surface issues bonds to finance its operations, which currently trade at $998.57 with a par value of $1000 and have a coupon rate of 5.01% and a term of 12 years with a semiannual payment. The interest rate on the 20-year Government of Canada bond is currently 3.00% and the market risk premium is 5.60%. MDFA has a marginal tax rate of 25.0% and a debt-to-total capitalization ratio of 30.0% which approximates the company's target capital structure. Exhibit 1: Market Return Data Process 1. Calculate the WACc for each of the two projects. 2. Calculate the cash flows for each year, from 0 (initial investment) to 10 or 15 (depending on the project). a. Do an income statement and add back depreciation to calculate the CF: b. Don't forget the inventory needs at the beginning as part of the initial cash flows. c. Remember tax effects at the end of the project as a result of the disposals. d. Note: you don't subtract interest from any cash flows because interest costs are considered in the WACC. So "incremental net income" = EBIT(1-T) 3. Calculate the NPV NPV= sum of the present values of the cash flows for this project Machine Design and Factory Automation Hailey Denison, CPA, has recently accepted a position as a financial analyst with Machine Design and Factory Automation (MDFA) Ltd. Reporting to Dexter Reid, P. Eng., Vice-President of New Product Development, Denison is responsible for preparing detailed feasibility studies of all new products to determine if they are commercially viable prior to being approved for launch. Company policy requires that analysts use the net present value (NPV) method. Product Review Process MDFA is an industrial equipment design and manufacturing firm with a reputation for providing its customers with innovative solutions to complex operational problems. The company is divided into three business units: - the Ventilation Division produces heating, cooling, and air purification systems: - the Surfaces Division makes equipment used to surface roads and pedestrian walkways; and - the Factory Automation Division manufactures machine tools and system integration software. MDFA's divisions are autonomous and are expected to work closely with current and prospective customers to originate new product proposals. These proposals are presented to MDFA's New Product Screening Committee (NPSC) for approval in three stages. In the first stage, the division tries to convince the NPSC of the product's technical and commercial potential in general terms. If approved, the NPSC provides funding to design a prototype. In the second stage, the prototype is reviewed to determine if it is technically viable. The product is normally sent back to the division for further refinements based on input from the committee. If these issues are addressed successfully, the product moves on to stage 3 where a detailed feasibility study of the commercial viability of the new product is completed by an independent financial analyst from the Office of the Vice-President of New Product Development. If approved at stage 3, the division receives funding to launch the product. Once a new product is launched, each division must provide a monthly progress report to the NPSC where the committee can decide to maintain, increase, decrease or discontinue funding based on their progress. The new product approval and monitoring processes at MDFA are rigorous, and divisional managers and financial analysts know to be well prepared whenever they present to the NPSC. New Product Proposals Denison is currently preparing two new product feasibility studies. One product is an industrial air filtration system that is used in sawmills and grain storage terminals. Wood and grain particles pose serious health and safety concerns for employees in these facilities if not properly controlled. Numerous systems are available to keep particle counts to an acceptable level, but MDFA has designed a new system based on vacuum cleaner technology that extracts and bags the particles and allows the clients to recycle them as inputs in particle board manufacturing and as animal feed. The second product is an automated paving stone installer. Increasingly cities are substituting paving stones for concrete when installing pedestrian walkways. Not only are paving stones visually more appealing than concrete or pebbled aggregate, they do not crack in the winter months, can be easily repaired if damaged, and can be moved and then replaced in order to access water and sewage services. Ventilation Division: Industrial Air Filtration System (IAFS) Projections The Ventilation Division will manufacture the IAFS using idle facilities. This plant can produce up to 260 units per year over the product's 10-year life. An outside appraiser indicated that the plant is worth $3,000,000, which breaks down as $1,400,000 for the land and $1,600,000 for the building. New production equipment costing $5,800,000 is also required. It is believed that the land will have a residual value of $1,800,000 at the end of the project's life, while the building and equipment will be worth $500,000 and $250,000. The building is subject to a CCA rate of 4.0% and the equipment is subject to a CCA rate of 20.0%. Incremental net working capital of $600,000 is also needed which will be liquidated at the end of the product's life. IAFS sales are estimated to be 70 units in the first year and will grow by 25.0% a year until plant capacity is reached. The unit price is $120,000 and unit costs are $100,000 per unit, which includes direct materials, direct labour, and manufacturing overhead. The Ventilation Division must also pay a $10,000 licensing fee per unit for the vacuum cleaner technology. Incremental selling and administration costs will be $350,000 per year. Automated Paving Stone Installer (APSI) Projections A new factory is needed to manufacture the APSI. The facility can produce up to 300 machines each year over the product's 15-year life. A parcel of land worth $400,000 will be purchased, and a building constructed for $1,800,000. Equipment costing $3,500,000 is also be required. At the end of the project's life, it is estimated the land can be sold for $780,000, while the building will have a residual value of $620,000 and the equipment's residual value will be negligible (i.e., zero). Building and equipment costs are subject to CCA rates of 4.0% and 20.0% respectfully. An investment of $370,000 in net working capital is needed to support production that will be liquidated at the end of the product's life. APSI sales are forecasted to be 100 units in the first year, 150 in the second year, 200 in the third year, 250 in the fourth year, and then reach factory capacity of 300 units in the fifth year. The product's list price is $350,000 and its unit cost is $340,000, which includes direct materials, direct labour and factory overhead. Incremental selling and administration costs to support the business will be $1,600,000. Existing corporate overhead of $230,000 per year will be allocated to the product as per company policy. Factory equipment will be overhauled at a cost of $1,500,000 at the end of year 8 . Discount Rate In the past, MDFA used a corporate cost of capital to evaluate the feasibility of its new product proposals. Denison felt this rate was inaccurate as it reflected the weighted-average cost of capital of the three MDFA divisions. The Ventilation Division likely has a higher cost of capital since its products are sold primarily to private-sector companies with greater exposure to the business cycle. In comparison, the Surfaces Division likely has a lower cost of capital as it sells its products primarily to city and municipal governments with relatively stable tax revenues and public works budgets. To be more precise, Denison decided to use divisional costs of capital to evaluate each project. To determine the cost of capital for the Ventilation Division, Denison collected information on the betas and credit spread on Treasuries for five public companies in the industry: For the Surfaces Division, MDFA only has one publicly-traded North American company for comparison. Dura Surface Ltd. has been in existence for 30 years selling road and sidewalk surfacing machinery. Exhibit 1 provides share prices for Dura Surface and national stock index values for the last five years. Dura Surface issues bonds to finance its operations, which currently trade at $998.57 with a par value of $1000 and have a coupon rate of 5.01% and a term of 12 years with a semiannual payment. The interest rate on the 20-year Government of Canada bond is currently 3.00% and the market risk premium is 5.60%. MDFA has a marginal tax rate of 25.0% and a debt-to-total capitalization ratio of 30.0% which approximates the company's target capital structure. Exhibit 1: Market Return Data Process 1. Calculate the WACc for each of the two projects. 2. Calculate the cash flows for each year, from 0 (initial investment) to 10 or 15 (depending on the project). a. Do an income statement and add back depreciation to calculate the CF: b. Don't forget the inventory needs at the beginning as part of the initial cash flows. c. Remember tax effects at the end of the project as a result of the disposals. d. Note: you don't subtract interest from any cash flows because interest costs are considered in the WACC. So "incremental net income" = EBIT(1-T) 3. Calculate the NPV NPV= sum of the present values of the cash flows for this project