Question

Machining Specialists Co. (MSC) produces bearings among other product lines. The final process of manufacturing these bearings involves assembling several component parts together. Currently, MSC

Machining Specialists Co. (MSC) produces bearings among other product lines. The final process of manufacturing these bearings involves assembling several component parts together. Currently, MSC manufactures all these component parts except for part J12.

Additional information on part J12

MSC had manufactured part J12 five years ago. Even though it no longer produces this part internally, it still has the equipment necessary for manufacturing this part.

The manager, Greg, is considering making this part again instead of buying it from an external supplier. The supplier charges $8 per unit of part J12. MSC usually purchases 90,000 units of part J12 per annum, and proposes to continue to do so in the future.

If part J12 were to be produced in-house, it would be manufactured in batches: each batch has a slightly different circumference (to fit into large, medium and small sized bearings). Therefore, 3 sizes of part J12 would have to be manufactured, i.e. large, medium and small: each size consumes the same amount of manufacturing resources. The equipment will have to be set-up each time the machinery was used to produce a different batch. The company has sufficient machining (hours) capacity to manufacture part J12 in-house.

Details of cost of manufacturing part J12:

i) Prime costs for each unit of part J12 are $4.50.

ii) The company has enough equipment to set up 3 additional production lines to produce component parts for its bearings with the available equipment: hypothetically, each line could produce 85,000 units of part J12. A supervisor would have to be hired for each production line, at a salary of $40,000/supervisor.

iii) Machining expenses (excluding supervisor/s salary in (ii) above) would amount to $1.50 per machine hour.

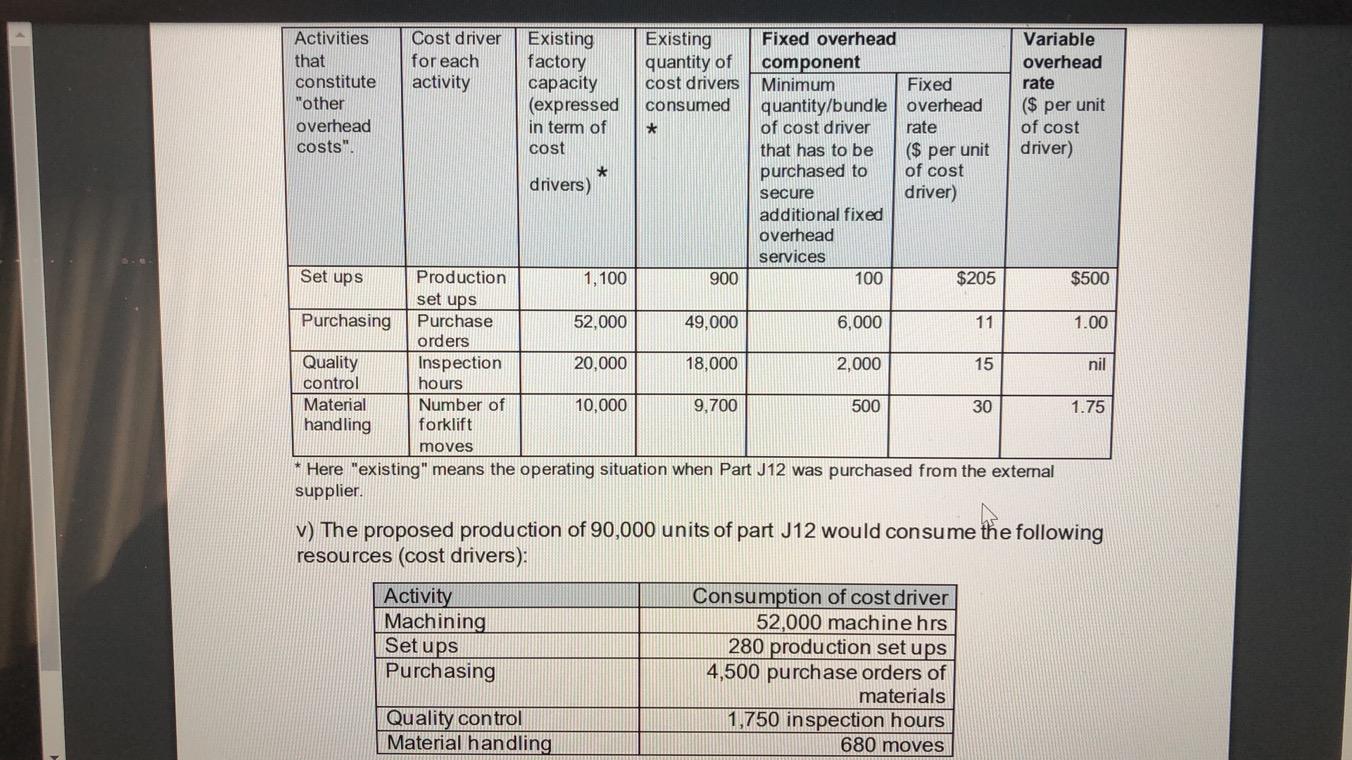

iv) The cost accountant has carried out a detailed analysis of other overhead costs. He explains that there are 2 types of "other overhead costs": fixed costs and variable costs. He adds that the fixed costs are not permanently fixed because he purchases bundles of these fixed overhead costs as and when the factory requires these overhead services. He provides a breakdown of these overhead costs and related information in the table below.

Other overhead costs:

Additional information If part J12 were to be manufactured in-house, the firm will not purchase this part from its external supplier. Therefore, purchase orders will decrease by 8,000 (which are associated with buying Part J12 from the external supplier). Similarly, moves in handling stock of part J12 freighted-in will decrease by 400. Inspection hours freed up from having to inspect stock of part J12 freighted in from the supplier, will be used to inspect raw material used to produce part J12.

Required:

1.1.) Leaving aside qualitative considerations, should Company MSC make or buy part J12 (based on quantitative analysis alone)? Show all relevant calculations. You must explain (in words) your numerical calculations and any assumptions you have made in your calculations

1.2) Would your analysis in (1.1) be different, if MSC did not have the capacity of machining hours to manufacture part J12? Explain in full in words - do not carry out additional calculations.

* Activities Cost driver Existing Existing Fixed overhead Variable that for each factory quantity of component overhead constitute activity capacity cost drivers Minimum Fixed rate "other (expressed consumed quantity/bundle overhead ($ per unit overhead in term of * of cost driver rate of cost costs". cost that has to be ($ per unit driver) purchased to of cost drivers) secure driver) additional fixed overhead services Production 1,100 900 100 $205 $500 set ups Purchasing Purchase 52,000 49,000 6,000 11 1.00 orders Quality Inspection 20,000 18,000 2,000 15 nil control hours Material Number of 10,000 9,700 500 30 1.75 handling forklift moves * Here "existing" means the operating situation when Part J12 was purchased from the external supplier. Set ups v) The proposed production of 90,000 units of part J12 would consume the following resources (cost drivers): Activity Consumption of cost driver Machining 52,000 machine hrs Set ups 280 production set ups Purchasing 4,500 purchase orders of materials Quality control 1,750 inspection hours Material handling 680 moves * Activities Cost driver Existing Existing Fixed overhead Variable that for each factory quantity of component overhead constitute activity capacity cost drivers Minimum Fixed rate "other (expressed consumed quantity/bundle overhead ($ per unit overhead in term of * of cost driver rate of cost costs". cost that has to be ($ per unit driver) purchased to of cost drivers) secure driver) additional fixed overhead services Production 1,100 900 100 $205 $500 set ups Purchasing Purchase 52,000 49,000 6,000 11 1.00 orders Quality Inspection 20,000 18,000 2,000 15 nil control hours Material Number of 10,000 9,700 500 30 1.75 handling forklift moves * Here "existing" means the operating situation when Part J12 was purchased from the external supplier. Set ups v) The proposed production of 90,000 units of part J12 would consume the following resources (cost drivers): Activity Consumption of cost driver Machining 52,000 machine hrs Set ups 280 production set ups Purchasing 4,500 purchase orders of materials Quality control 1,750 inspection hours Material handling 680 movesStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The New International Financial System Analyzing The Cumulative Impact Of Regulatory Reform

Authors: Douglas Evanoff , Douglas D Evanoff , Andrew G Haldane , George G Kaufman

1st Edition

9814678325,9814678341