Question

MAGIC TIMBER AND STEEL: INVESTMENT EVALUATION WITH NET PRESENT VALUE THE COMPANY Magic Timber and Steel (Magic) was formed in 1999 in Caloundra on the

MAGIC TIMBER AND STEEL: INVESTMENT EVALUATION WITH NET PRESENT VALUE

THE COMPANY

Magic Timber and Steel (Magic) was formed in 1999 in Caloundra on the Queensland Sunshine Coast, Australia.' Located about 100 kilometres (60 miles) north of the state capital of Brisbane, the coast was known for its clean, protected beaches and safe waters. The business peaked in terms of sales revenue in about 2011 and went on to experience a steady decrease in turnover that was attributed to a number of reasons, including infrastructure issues on the coast and a slowing in the tourism market.

To reinvigorate the business, in early 2015, Magic's owner, John Davidson, believed his company required investment in fixed assets, specifically, a large finisher that would increase capacity and reduce maintenance. Since the new machine required a large financial investment, Davidson used the net present value method to determine whether the purchase would add value to the firm. In addition, he needed to consider some important qualitative factors before a decision could be made.

MAGIC TIMBER AND STEEL PTY. LTD.

Magic's original owners, John Davidson and Kelly Peters leased the company's first premises on the site of a disused service station and specialized in packs of "seconds" timber that was sold to the retail market at discounted prices. The business was successful and eventually outgrew the small premises.

In July 2002, Magic purchased an industrial block of land that was approximately 10 times the size of the leased premises and on which was built a large, secure shed. The owners decided to move on from the timber packs and instead set up the new location as a timber yard. As the business continued to grow, Davidson and Peters began stocking hardware supplies and purchased a large Scania truck that could be used for picking up products and providing delivery service. Magic also invested in a range of machinery. While the owners were happy to pay out a large sum of money for a new Scania, they decided to purchase only secondhand machinery. As the business grew, they preferred to limit the staff to themselves, one other permanent employee, and two casual employees who would work on an on-call basis, as demand required.

For Magic, the timing of its growth was fortuitous because the Sunshine Coast was undergoing a rapid residential building expansion in response to a 10 percent per annum population growth in 2002, 2003, and

2004.3 During this growth phase for the company, Magic earned a reputation for being a supplier of discount products, and soon, the company acquired a substantial core of builders as its customers. The smaller retail market continued to grow but proportionally became a lower contributor to Magic's sales activity. In 2005, Davidson bought Peters' share of the company and became the sole shareholder. As part of the agreement, Peters kept the Scania truck, along with the debt associated with it

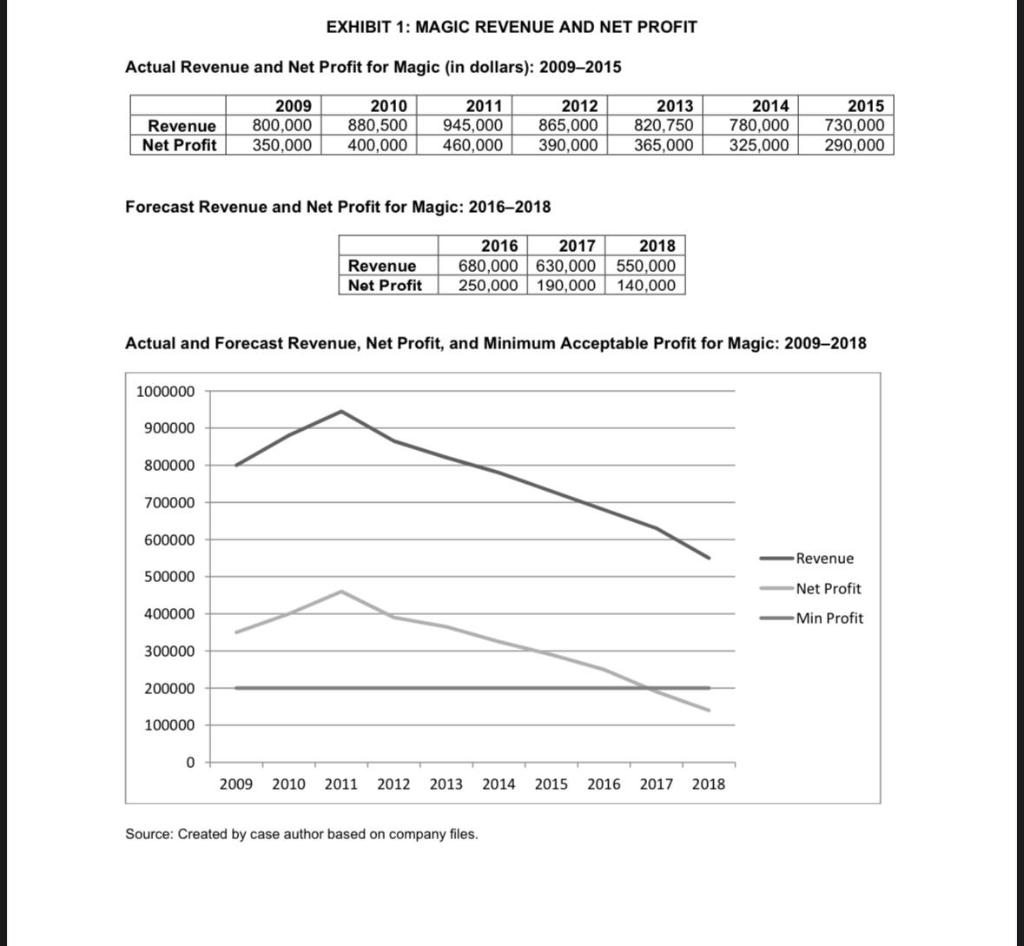

Around 2011, Magic's business peaked in terms of sales revenue and then experienced a steady decrease in turnover (see Exhibit 1)3 This decline was attributed to a number of reasons, including infrastructure issues on the coast, a slowdown in the tourism industry, and a decrease in population growth (less than 4 percent in 2011); however, the Sunshine Coast still remained one of Australia's fastest-growing regions.

As a result of the declining economic environment, a number of builders who held accounts with Magic went into liquidation, leaving the company with bad debts that had to be written off or placed on payment plans, a situation that had a significant impact on Magic's own financial situation. Around the same time, a large Australian publicly listed retailer, Wesfarmers Limited, opened one of its large Bunnings Warehouse Stores (Bunnings) within two kilometres of Magic's premises. Bunnings was similar to North America's Home Depot and was a direct competitor to Magic.

During 2013 and 2014, in an effort to reinvigorate Magic, Davidson undertook an increased marketing campaign that included print and radio. He also added steel to Magic's product line, which necessitated the purchase of a large laser-cutting machine that required a significant capital outlay of $300.000.4. Davidson continued to promote his business as distinguishing itself from the larger competitors by providing personal service. and he strived to give an impression of a successful, professional business.

While a number of similar-sized competitors left the market, thanks to Davidson's experience and the company's significant stock holding, Magic was able to stay solvent. Subsequently, as the business became more difficult, Davidson actively sought to reduce Magic's stock levels, replacing them only as the market demand rather than holding a diverse range. Not surprisingly, this approach to inventory control meant that some customers shopped elsewhere since Magic did not stock what they needed to purchase. Davidson accepted this reality and continued with his strategy of stocking core items at good prices and offering expert, friendly assistance.

THE ISSUE

While the move into the steel business had proved relatively successful due to Magic's state-of-the-art machinery, the older timber equipment was showing its age and becoming more troublesome - in particular, the large finisher. A report offered by the machine's manufacturer suggested that the machine could be reinvigorated; however, Davidson wondered whether the company should instead invest in a new machine that would offer the increased capability and reduced maintenance. Davidson believed this new machine would turn Magic's fortunes around and return it to the revenue levels achieved a number of years ago. The new machine required a significant outlay, however, and it was this investment decision that Davidson had to consider

Existing Machine

The existing machine was a Matrix 750. The Matrix had been purchased secondhand when it was five years old. Davidson was particularly concerned with staff safety and was reluctant to allow other staff members to use this machine because this particular model was known to be very sensitive to the angle of the timber and would kick back severely if the lumber was not correctly positioned. Davidson had not experienced this particular problem since owning the machine.

A competitor had offered $35,000 cash for the machine, an amount that represented its current book value.

If Davidson opted to keep the machine, Magic would continue to claim depreciation of $6,000 per year for each of the next five years, at which point the machine would be unserviceable and would be sold for $5,000 as scrap. If Davidson elected to keep and repair the old machine, it would require $28,000 to be spent immediately and $7,000 in regular maintenance in each of the next five years. In Year 3, the machine would require another investment of $4,000 for a larger scheduled service.

New Machine

The new machine under consideration was a Delta A390, which offered an increase in capacity of 40 percent. This capacity was probably in excess of Magic's needs, although the business would make some use of it. Also, the new machine allowed the possibility of obtaining some custom work for a specialist wood crafter.

The new machine cost $145,000, and the tax office allowed straight-line depreciation of 10 percent per annum. After five years, Magic would sell the Delta for $60,000. Given that the company selling the machine to Magic operated in a very competitive market, it was willing to negotiate the terms of a maintenance plan. The seller offered fixed pricing starting at $2,000 in the first year, increasing by $1,000 per year (payable at year-end). To fund the purchase, Magic's bank offered a 6 percent per annum loan to be repaid as interest-only payments for five years, with the full principal repayable at the end of the loan

period

Given the technological advancements of the Delta over the Matrix, Davidson expected that he could achieve significant savings in both labour and electricity costs. For labour, in the first year, Davidson forecasted a 10 percent cost reduction (the existing rate was $30 per hour), based on a 35-hour week in a

50-week year. This labour saving would then increase by a fixed $250 each year.

For electricity, in the first year, the saving was expected to be 10 percent as well. Electricity costs averaged $5.625 per hour, 24 hours a day, seven days a week, in a 50-week year. This electricity saving would then increase by a fixed $75 each year.

THE DECISION

While Davidson felt enthusiastic about the upcoming possibilities for Magic, he had some concerns about the new level of debt, not just regarding the size of the loan, but also with respect to what that commitment meant for the business in terms of future opportunities. Davidson believed that if new business arose as a result of the increased capacity, the debt repayments could be comfortably met - but the market conditions and the competitive nature of Bunnings concerned him. However, he also realized that if he opted to do nothing, the company's declining revenue trend of the last few years would most likely continue. Should Magic go ahead with the investment in the new machinery?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Use The News To Separate The Noise From The Investment Nuggets And Make Money In Any Economy

Authors: Maria Bartiromo

1st Edition

0061873489