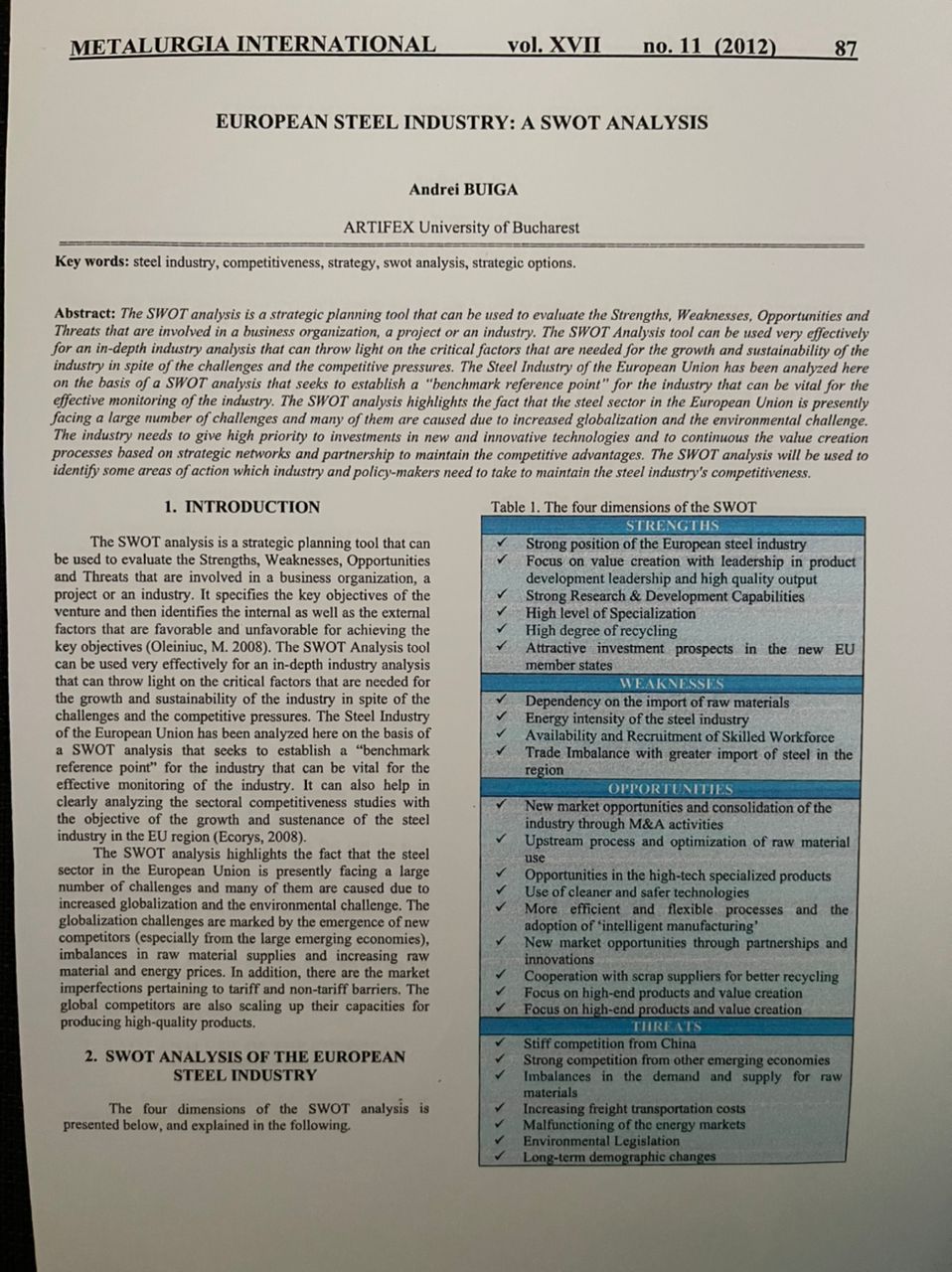

making SWOT analysis of one organization considering the below formats

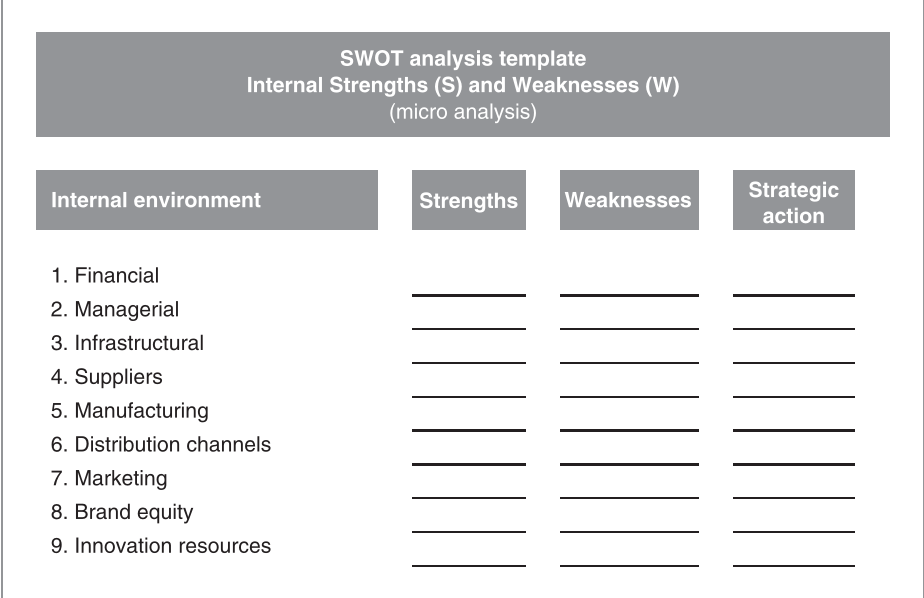

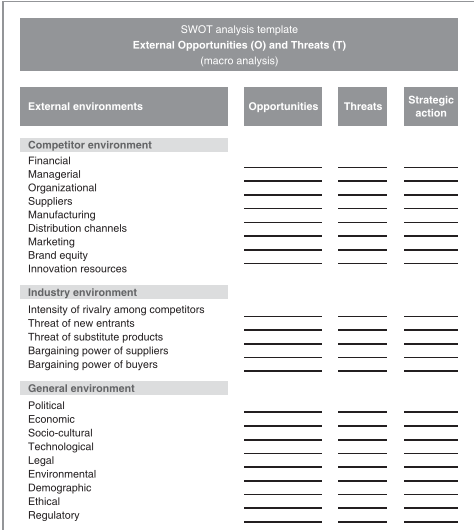

SWOT analysis template Internal Strengths (S) and Weaknesses (W) (micro analysis) Internal environment Strengths Weaknesses Strategic action 1. Financial 2. Managerial 3. Infrastructural 4. Suppliers 5. Manufacturing 6. Distribution channels 7. Marketing 8. Brand equity 9. Innovation resourcesSWOT analysis template External Opportunities (O) and Threats (T) (macro analysis) Strategic External environments Opportunities Threats action Competitor environment Financial Managerial Organizational Suppliers Manufacturing Distribution channels Marketing Brand equity Innovation resources Industry environment Intensity of rivalry among competitors Threat of new entrants Threat of substitute products Bargaining power of suppliers Bargaining power of buyers General environment Political Economic Socio-cultural Technological Legal Environmental Demographic Ethical RegulatoryMETALURGIA INTERNATIONAL vol. XVII no. 11 (2012) 87 EUROPEAN STEEL INDUSTRY: A SWOT ANALYSIS Andrei BUIGA ARTIFEX University of Bucharest Key words: steel industry, competitiveness, strategy, swot analysis, strategic options. Abstract: The SWOT analysis is a strategic planning tool that can be used to evaluate the Strengths, Weaknesses, Opportunities and Threats that are involved in a business organization, a project or an industry. The SWOT Analysis tool can be used very effectively for an in-depth industry analysis that can throw light on the critical factors that are needed for the growth and sustainability of the industry in spite of the challenges and the competitive pressures. The Steel Industry of the European Union has been analyzed here on the basis of a SWOT analysis that seeks to establish a "benchmark reference point" for the industry that can be vital for the effective monitoring of the industry. The SWOT analysis highlights the fact that the steel sector in the European Union is presently facing a large number of challenges and many of them are caused due to increased globalization and the environmental challenge. The industry needs to give high priority to investments in new and innovative technologies and to continuous the value creation processes based on strategic networks and partnership to maintain the competitive advantages. The SWOT analysis will be used to identify some areas of action which industry and policy-makers need to take to maintain the steel industry's competitiveness. 1. INTRODUCTION Table 1. The four dimensions of the SWOT STRENGTHS The SWOT analysis is a strategic planning tool that can Strong position of the European steel industry be used to evaluate the Strengths, Weaknesses, Opportunities Focus on value creation with leadership in product and Threats that are involved in a business organization, a development leadership and high quality output project or an industry. It specifies the key objectives of the Strong Research & Development Capabilities venture and then identifies the internal as well as the external High level of Specialization factors that are favorable and unfavorable for achieving the High degree of recycling key objectives (Oleiniuc, M. 2008). The SWOT Analysis tool Attractive investment prospects in the new EU can be used very effectively for an in-depth industry analysis member states that can throw light on the critical factors that are needed for WEAKNESSES the growth and sustainability of the industry in spite of the Dependency on the import of raw materials challenges and the competitive pressures. The Steel Industry Energy intensity of the steel industry of the European Union has been analyzed here on the basis of Availability and Recruitment of Skilled Workforce a SWOT analysis that seeks to establish a "benchmark Trade Imbalance with greater import of steel in the reference point" for the industry that can be vital for the region effective monitoring of the industry. It can also help in OPPORTUNITIES clearly analyzing the sectoral competitiveness studies with New market opportunities and consolidation of the the objective of the growth and sustenance of the steel industry through M&A activities industry in the EU region (Ecorys, 2008). Upstream process and optimization of raw material The SWOT analysis highlights the fact that the steel use sector in the European Union is presently facing a large Opportunities in the high-tech specialized products number of challenges and many of them are caused due to Use of cleaner and safer technologies increased globalization and the environmental challenge. The More efficient and flexible processes and the globalization challenges are marked by the emergence of new adoption of "intelligent manufacturing' competitors (especially from the large emerging economies), New market opportunities through partnerships and imbalances in raw material supplies and increasing raw innovations material and energy prices. In addition, there are the market Cooperation with scrap suppliers for better recycling imperfections pertaining to tariff and non-tariff barriers. The Focus on high-end products and value creation global competitors are also scaling up their capacities for Focus on high-end products and value creation producing high-quality products. THREATS Stiff competition from China 2. SWOT ANALYSIS OF THE EUROPEAN Strong competition from other emerging economies STEEL INDUSTRY Imbalances in the demand and supply for raw materials The four dimensions of the SWOT analysis is Increasing freight transportation costs presented below, and explained in the following. Malfunctioning of the energy markets Environmental Legislation Long-term demographic changesMETALURGIA INTERNATIONAL vol. XVII no. 11 (2012) 89 Opportunities in the high-tech specialized products prioritize and develop the European steel industry's The steel manufacturing industry in the European Union can capabilities and strengths. The steel industry in the European undergo specialization in the high-tech and premium Union has a competitive edge in this area and most of the products segment to take advantage of new opportunities. forecasts have predicted that the demand in the high-end area Some of the innovation drivers in the manufacturing sector will continue to increase. are energy efficiency and environmental responsibility products. Wind energy is rapidly becoming more important THREATS in Europe and presently more than 100 offshore wind farms are under construction in the region, each requiring nearly Stiff competition from China 3,000 metric tons of steel. China has increased its steel output level quite significantly and its steel capacity level has also been driven Use of cleaner and safer technologies by its high economic growth and demand from its The use of more efficient technologies is an important construction sector. China has also markedly improved its opportunity for increasing energy efficiency and reducing international business relations and it has become the world's emissions during the steel production processes. Thus, largest exporter of semi-finished and finished steel products. technological innovation and the use of cleaner and safer The European Union is one of the largest export destinations technologies are important, partly needed due to legislation, for China and it has flooded the region with both flat and but also for the prospects of reducing costs and meeting the long products produced by its steel industry. increasing demand for cleaner and safer technologies. Most significantly, the cleaner and safer technologies provide an Strong competition from other emerging economies important opportunity for proactively pursuing new business The European Union's steel industry not only faces opportunities. strong competitive pressures from China but also from the By participating in the European Steel Technology other large and growing economies like India, Russia, Platform (ESTEP), the EU steel industry is presently working Ukraine and Brazil. India is at present rated among the top with the European Commission and the member nations to ten global steel producing countries and the Indian steel finance long-term projects aimed at changed process industry is expected to continue its growth and expansion technologies. The most ambitious one among the initiatives is phase in the near future. The Indian steel producers are quite the ULCOS (Ultra Low CO2 Steelmaking), that aims to cost-competitive and they have enough reserves of iron ore reduce CO2 emissions from steelmaking by 50% by 2050. and coking coal, and they are striving hard to achieve the global standards for quality, productivity, and efficiency. More efficient and flexible processes and the adoption of Brazil also has a well consolidated and low-cost steel 'intelligent manufacturing industry due to its domestic iron ore reserves, low energy and The steel industry in the European Union must keep labor costs. investing in the development of new technology and achievement of production process improvements so as to Imbalances in the demand and supply for raw materials pursue new market opportunities and to maintain and develop The increasing demand for steel, driven mostly by its competitive strength. This requires higher efficiency and China, has resulted in the present imbalances in supply and more flexibility in the downstream process. Some of the demand for the raw materials. This can result in a shift intelligent manufacturing processes for better organization towards the low-cost countries for steel production, as some and management, (such as Lean, knowledge management) of them have cheaper access to the raw materials and the and the adoption of new IT technologies are key to achieve availability of low-wage labor. this objective. Increasing freight transportation costs New market opportunities through partnerships and The steel producers in the European Union face the innovations challenge of the increasing freight transportation rates that The focus on high-quality customized steel products in also increase the relative costs and make it more difficult to close cooperation with the customers is an opportunity to compete in the competitive export markets. Moreover, differentiate and to compete with the other suppliers. Strong transport within the European Union is far more expensive and collaborative relationships help the companies to meet than in the other areas such as the US due to imperfections in the expectations of their customers by creating more value. cross-border railway transport of goods and country related Such partnerships are normally important for the differences in road regulation. Apart from increasing freight maintenance of strong business relationships with the present rates, malfunctioning logistics infrastructures and transport and potential customers. markets also are a threat to the competitiveness of the European steel industry. Cooperation with scrap suppliers for better recycling Recycling is a crucial element of steel production in the Malfunctioning of the energy markets European Union. It is strategically important to maintain a The European Union has increased the consumption well-organized recycling process (or to achieve optimum energy at a steady pace and the region is a major importer of scrap availability) due to the structural barriers of further energy (imports correspond to more than 50% of total energy replacing the iron ore by scrap and the increasing export of use). The import share of the energy consumption in the scrap to the non-EU countries. region is expected to increase steadily in the near future. The steel industry is a heavy user of energy and this increasing Focus on high-end products and value creation energy usage and dependence on imports would definitely The focus on high-quality and high value added affect it. The overall competitiveness of the steel sector is products, solutions and services is important to further also hampered due to malfunctions in the energy market sue88 vol. XVII no. 11 (2012) METALURGIA INTERNATIONAL is quite attractive to invest in business opportunities in these STRENGTHS new member countries and this is a strong growth factor for Strong position of the European steel industry the EU steel industry. According to EUROFER (2012), the steel industry in Europe is in a leading position in the world with an annual turnover WEAKNESSES of about EUR 190 billion and directly employing nearly 360 thousand highly skilled personnel, and manufacturing 200 Dependency on the import of raw materials million tons of steel per year. The 23 European Union The steel industry in the European Union is highly Member States have more than 500 steel production facilities dependent on imported raw materials and the overseas and they provide direct and indirect employment and a living supplies form a large part of its total raw material input. Thus for millions of Europeans. the industry suffers from the weakness in terms of secure raw The EU steel industry operates across national borders, and material supply and variable costs due to the continual the industry has a strong and advantageous position in fluctuations in raw material and transportation prices. domestic markets, particularly in high-end segments. The steel manufacturers in the European Union are well Energy intensity of the steel industry established in their primary home markets, and they have The European Union steel industry suffers from the strong relations with their customers all sub-sectors. This also drawback of the intense energy usage for the operation and creates a strong foundation for looking for new business other processes. As such, the industry is vulnerable to energy opportunities in high-end export markets. shocks and rising fuel prices as well as to the government policies aimed at reducing emissions. Focus on value creation with leadership in product development leadership and high quality output Availability and Recruitment of Skilled Workforce The EU's steel manufacturing industry is the world's The European Union steel industry faces a strong and second largest in terms of market size and it is increasing demand for highly skilled labor with more technologically advanced due to the focus on product quality, knowledge and expertise. Thus hiring and retaining skilled manufacturing excellence, performance of equipment, and people is getting more difficult as the supply of labor is innovative capacity. It is capable of providing complex and decreasing and the competition for highly skilled and high-quality products to the demanding customers, and the qualified personnel is constantly increasing. industry has a strong emphasis on value creation. Thus, some of the key strengths of the industry are its high-quality output Trade Imbalance with greater import of steel in the and customer focus, supported by the use of advanced region technology and high standards within service and the just-in- The European Union faces the challenge of unbalanced trade time delivery approach. flows with moderate rise in the export of steel in the global markets and significant increase in imports into the region. Strong Research & Development Capabilities Some of the factors that lead to this trade imbalance are the The steel industry in the EU is characterized by a high high labor costs and less availability of raw materials. The standard for research and development activities that keep the increasing capacity and the oversupply by the key exporting factories at the forefront of technology which is an important countries (mainly China) have also contributed significantly competitive advantage for the manufacturers. All sub sectors to this situation. of the steel industry are engaged in R&D activities in close cooperation with their customers and OEM manufacturers. OPPORTUNITIES High level of Specialization New market opportunities and consolidation of the The European Union steel industry is highly industry through M&A activities specialized with the small manufacturers providing The steel industry in the European Union has witnessed specialized products in close business relationships with their large-scale consolidations with some of the significant customers. Most of the steel foundries operate as custom- merger and acquisition activities in the recent years. The steel made suppliers for the industries they serve, and as such there industry and its sub-sectors are expected to undergo further is limited competition in the industry. consolidations through mergers and acquisitions, which can invariably enhance the steel industry's overall bargaining High degree of recycling power. More industry consolidation improves the foundation The high degree of recycling that is followed in the European for devising a business strategy that is geared to access the Union steel industry with a large-scale scrap usage is the best capabilities, knowledge, and assets and enhance the strength in all the sub-sectors of the industry. This makes the management capacity over the business cycle. European steel manufacturers quite competitive compared to the suppliers in the APAC and the Middle East who are Upstream process and optimization of raw material use increasingly becoming dependant on scrap imports. Upstream processing and optimization of raw material utilization is significant for improving the steel industry's raw Attractive investment prospects in the new EU member material efficiency. The factors also help to reduce the effects states of supply-side sensitivity. In addition, such process The new member states that have either officially improvements can also lead to lower energy consumption and joined the EU or are in the process of joining, have high lesser CO2 emission. growth rates and strong demands for steel. Moreover, in these countries the labor costs are low but the technological capacity, expertise and the skill levels are improving. Thus it90 vol. XVII no. 11 (2012) METALURGIA INTERNATIONAL to the weak connections between energy systems, national improving capacity for strategic outlook to meet the future taxations and differences in the pricing structure and risks and challenges regulation of the energy markets. 5. Setting up an even playing field and improving the functioning of energy and transport markets in the Environmental Legislation European Union region The European Union steel industry faces the challenge 6. Enhancing the skills base and strategies for lifelong of compliance to environmental regulations regarding its learning energy use, CO2 emission, pollution prevention, and waste. The new Emission Trading Scheme (ETS) legislation might 4. REFERENCES lead to the loss of competitiveness of the European steel producers compared to the other steel producers do not face [1] Deutsche Bank Research, 2009 EU steel industry - such restrictive emission legislations. The adverse Further towards high-tech products. Retrieved from environment legislations can also reduce the interest of http://www.dbresearch.de/PROD/DBR_INTERNET_DE- investors while investing in the steel industry projects. PROD/PROD0000000000248298.pdf [2] Ecorys, 2008 Study on the Competitiveness of the Long-term demographic changes European Steel Sector - Within the Framework Contract of The demographic changes in European Union Sectoral Competitiveness Studies - ENTR/06/054. Retrieved correspond to a declining workforce and consequently the from http:/ec.europa.eu/enterprise/sectors/metals- difficulty for the European industries to ensure and attract minerals/files/final_report_steel_en.pdf sufficient and qualified employees. In addition, the number of (3] Enterprise & Industry Online Magazine, 2009 young people applying for technical programs is decreasing Strengthening Europe's steel industry. European Union. across the region. These factors are threats to the steel Retrieved from industry, (as it is to the other industries as well) in terms of http://ec.europa.eu/enterprise/magazine/articles/industrial- ensuring the hiring of sufficient and qualified people for the policy/article_8748_en.htm work in the industry. It also creates a structural barrier to the 141 EUROFER, 2012 Welcome to EUROFER, the European health and competitive edge of the industry compared to Steel Association. Retrieved from http:/www.eurofer.org other countries without such difficulties. 15] EUROFER, Manifesto of the European Steel Industry for Members of the European Parliament 2009 - 2014. 3. CONCLUSION Retrieved from http://www.dunaferr.hu/Manifesto_for_MEPs_2009- The strengths of the European Union steel sector 2013.pdf constitute a strong position for meeting the challenges of [6] M. Oleiniuc, 2008 The applications of SWOT analysis globalization due to its technology leadership, high-quality in the industrial units. Retrieved from products, and a strong tradition for innovation and technical http://www.upm.ro/projecte/EEE/Conferences/papers/$231.p knowledge base. In order to maintain and strengthen the df competitive position, it is imperative for the EU steel [7] H. Shinno, H. Yoshioka, S. Marpaung, S.Hachiga industry to continue the development of its current strengths Quantitative SWOT analysis on global competitiveness of while exploring the new market opportunities. The industry machine tool industry, Journal on Engineering Design, Vol. needs to give high priority to investments in new and 17, Is 3, pp. 251-258, 2006. innovative technologies and to continuous the value creation 18] Suttle, R. (n.d.). Process of Industry Analysis. Demand processes based on strategic networks and partnership to Media. Retrieved from maintain the competitive advantages. The steel industry must http://smallbusiness.chron.com/process-industry-analysis- be encouraged to constantly improve the technologies to 809.html enhance flexibility and efficiency. The issues related to the 19] I. Verboncu, C. Protopopescu The Implications of environment legislation compliance must be met by the Management Reengineering on the Performances continuous development of cleaner technologies in the Organizations, Romanian Statistical Review - Supplement production processes, management systems, products and (December 2010), pp. 8-10, ISSN 1018-046x. transport. [10] A. Victor, Knowledge Organization Using The SWOT. The SWOT analysis can be used to identify the International Conference Modern n Approaches in following six areas of action which industry and policy- Organizational Management and Economy 2011, Vol. 5, Is. makers need to take to maintain the steel industry's 1. pp. 15-21, 2011. competitiveness (Ecorys, 2008). These are: 1. Engaging in dealing with the climate change challenge Correspondence to effectively Andrei BUIGA Upstream engagement and investments andrei.buiga@gmail.com, Universitatea ARTIFEX din Maintenance of high technology leadership and Bucuresti operational excellence 4. Enhancing knowledge sharing and engagement in strategic networks for maintaining competitive position and