Answered step by step

Verified Expert Solution

Question

1 Approved Answer

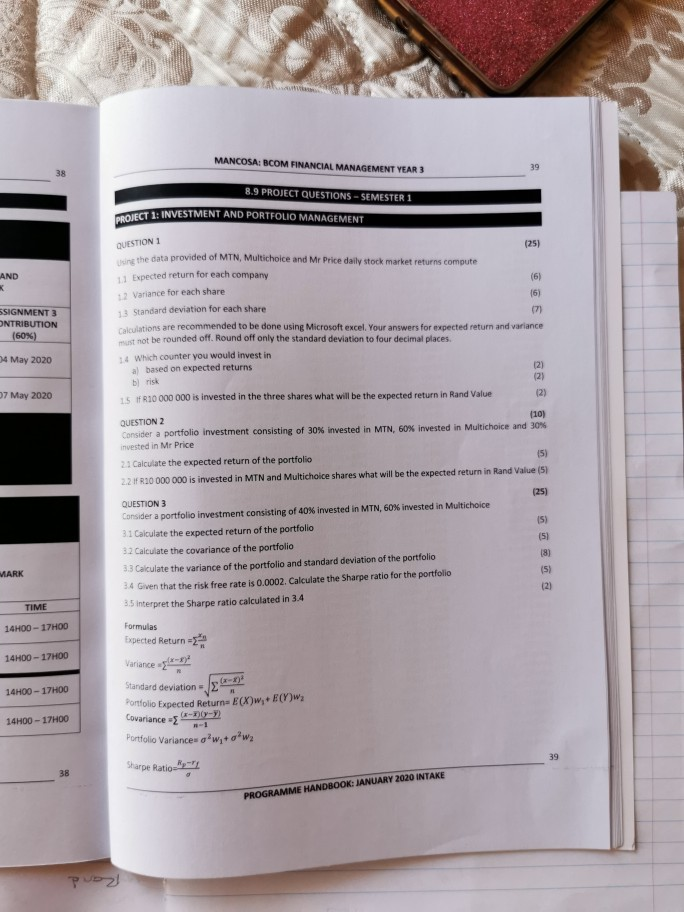

MANCOSA: BCOM FINANCIAL MANAGEMENT YEAR 3 8.9 PROJECT QUESTIONS - SEMESTER 1 IECT 1: INVESTMENT AND PORTFOLIO MANAGEMENT QUESTION1 AND SSIGNMENT 3 ONTRIBUTION the data

MANCOSA: BCOM FINANCIAL MANAGEMENT YEAR 3 8.9 PROJECT QUESTIONS - SEMESTER 1 IECT 1: INVESTMENT AND PORTFOLIO MANAGEMENT QUESTION1 AND SSIGNMENT 3 ONTRIBUTION the data provided of MTN, Multichoice and Mr Price daily stock market returns compute 11 Expected return for each company 12 Variance for each share 13 Standard deviation for each share rations are recommended to be done using Microsoft excel, Your answers for expected return and variance ust not be rounded off. Round off only the standard deviation to four decimal places 14 Which counter you would invest in a) based on expected returns b) risk 15 if R10 000 000 is invested in the three shares what will be the expected return in Rand Value (2) (60%) 04 May 2020 07 May 2020 (10) QUESTION 2 Consider a portfolio investment consisting of 30% invested in MTN, 60% invested in Multichoice and 30% invested in Mr Price 21 Calculate the expected return of the portfolio (5) 22 R10 000 000 is invested in MTN and Multichoice shares what will be the expected return in Rand Value (51 QUESTION 3 Consider a portfolio investment consisting of 40% invested in MTN, 60% invested in Multichoice 31 Calculate the expected return of the portfolio 32 Calculate the covariance of the portfolio 3.3 Calculate the variance of the portfolio and standard deviation of the portfolio 14 Given that the risk free rate is 0.0002. Calculate the Sharpe ratio for the portfolio 3.5 Interpret the Sharpe ratio calculated in 3.4 MARK TIME 14H00 - 17H00 14H00 - 17HOD 14H00-17H00 Formulas Expected Return=2 Variance Standard deviation Portfolio Expected Return= E(X)w, Covariance - - - Portfolio Variance o'w,+ ow2 Sharpe Ratio-By- E(V) 14H00 - 17H00 PROGRAMME HANDBOOK: JANUARY 2020 INTAKE 3 MANCOSA: BCOM FINANCIAL MANAGEMENT YEAR 3 8.9 PROJECT QUESTIONS - SEMESTER 1 IECT 1: INVESTMENT AND PORTFOLIO MANAGEMENT QUESTION1 AND SSIGNMENT 3 ONTRIBUTION the data provided of MTN, Multichoice and Mr Price daily stock market returns compute 11 Expected return for each company 12 Variance for each share 13 Standard deviation for each share rations are recommended to be done using Microsoft excel, Your answers for expected return and variance ust not be rounded off. Round off only the standard deviation to four decimal places 14 Which counter you would invest in a) based on expected returns b) risk 15 if R10 000 000 is invested in the three shares what will be the expected return in Rand Value (2) (60%) 04 May 2020 07 May 2020 (10) QUESTION 2 Consider a portfolio investment consisting of 30% invested in MTN, 60% invested in Multichoice and 30% invested in Mr Price 21 Calculate the expected return of the portfolio (5) 22 R10 000 000 is invested in MTN and Multichoice shares what will be the expected return in Rand Value (51 QUESTION 3 Consider a portfolio investment consisting of 40% invested in MTN, 60% invested in Multichoice 31 Calculate the expected return of the portfolio 32 Calculate the covariance of the portfolio 3.3 Calculate the variance of the portfolio and standard deviation of the portfolio 14 Given that the risk free rate is 0.0002. Calculate the Sharpe ratio for the portfolio 3.5 Interpret the Sharpe ratio calculated in 3.4 MARK TIME 14H00 - 17H00 14H00 - 17HOD 14H00-17H00 Formulas Expected Return=2 Variance Standard deviation Portfolio Expected Return= E(X)w, Covariance - - - Portfolio Variance o'w,+ ow2 Sharpe Ratio-By- E(V) 14H00 - 17H00 PROGRAMME HANDBOOK: JANUARY 2020 INTAKE 3

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Overcoming Debt Achieving Financial Freedom

Authors: Cindy Zuniga-Sanchez

1st Edition

1119902320, 978-1119902324