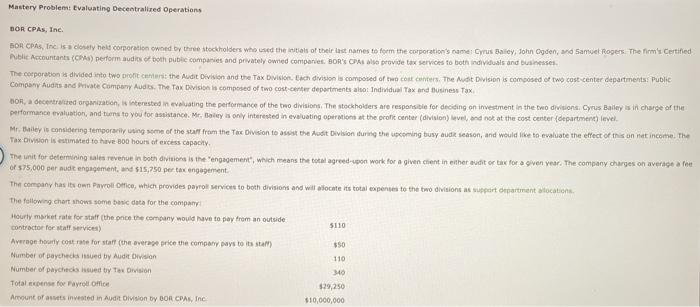

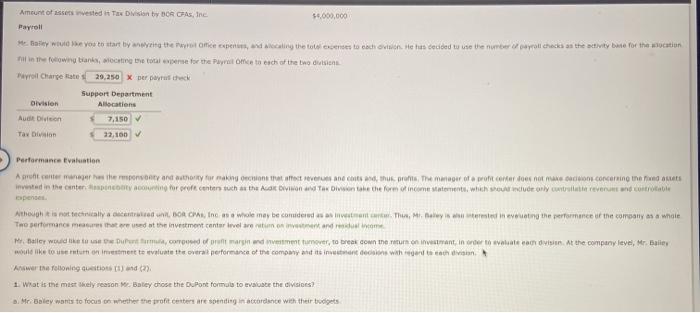

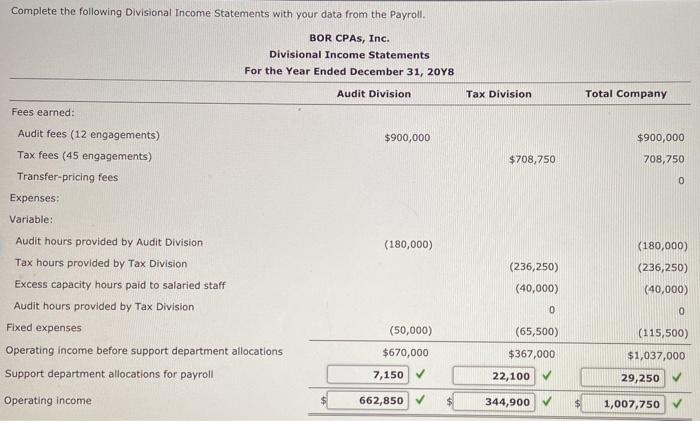

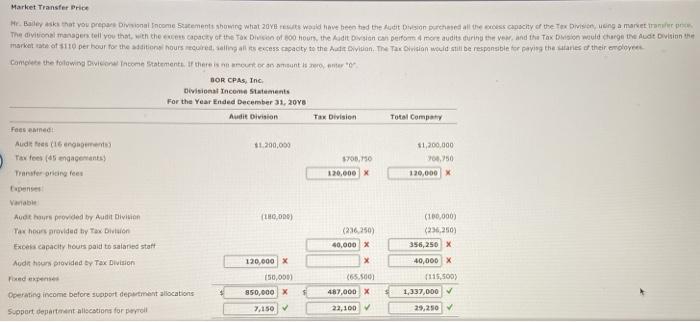

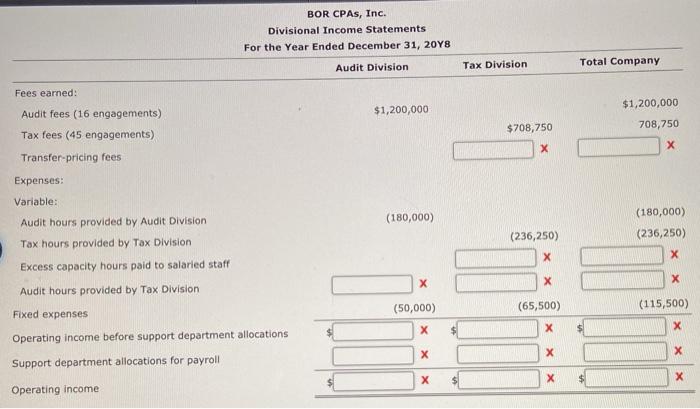

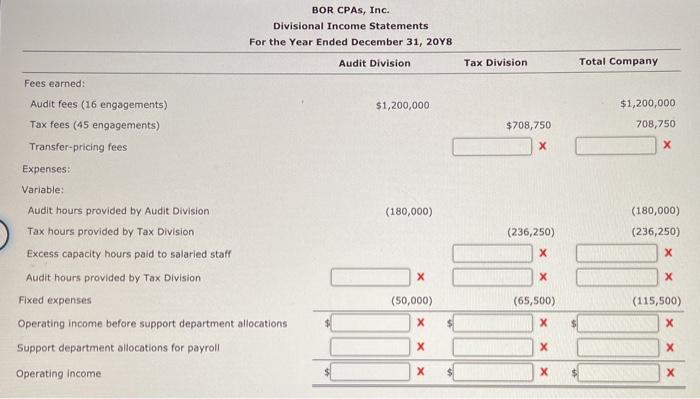

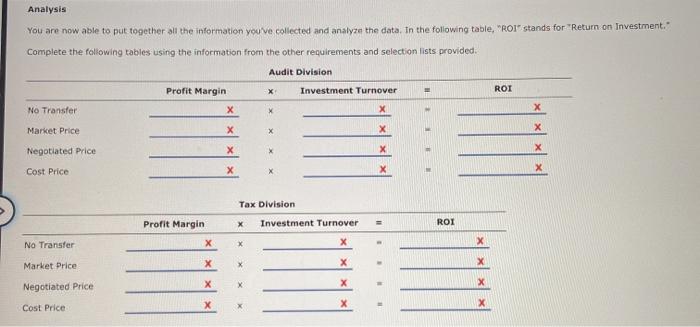

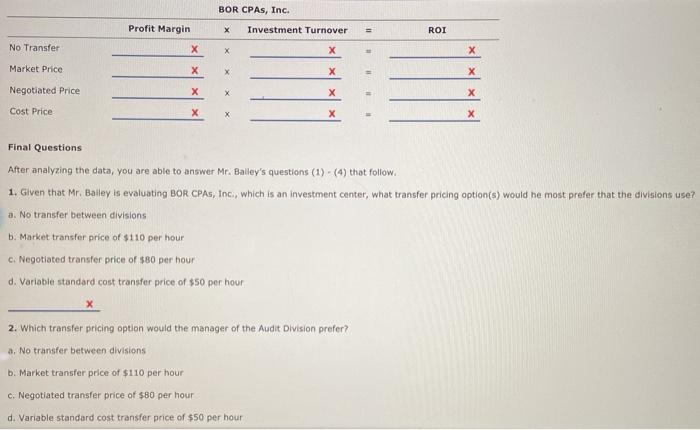

Mastery Problem: Evaluating Decentralized Operations BOR CPAS, Inc. BORCA, Te is closely held corporation owned by the stockholders who used the tal of their last names to form the corporation's name: Cyrus Daley, John Ogden, Samuel Rogers. The firm's Certified Public Accountants (CPA) perform audits of both public companies and privately owned companies. BORCA o provide tax services to both individuals and businesses The corporation is divided into two brot cantat the Audit Division and the Tax Division, a division is composed of two costantes. The Not Division is composed of two cost center departments Public Company Audits and Private Company Audits. The Tax Division is composed of two cost center departments also individual Tax and Business Tax BOR, a decentred organications interested in vaivating the performance of the two divisions. The stockholders are responsible for deciding on investment in the two divisions. Cyrus Balley is in charge of the performance evaluation, and turns to you for assistance. Mr. Bly only interested in evaluating operations at the profit center (division), and not at the cost center department) uvel Mr. Barley is considering temporarily wing some of the start from the Tae Division to set the Audit Division during the coming busy audie season, and would like to evaluate the effect of this on net income. The Tax Division is estimated to have 800 hours of excess capacity The unit for determining sales revenue in both avion is the engagement, which means the total agreed-upon work for a given cient in either audit or tax for a given year. The company charges on average for of 375,000 per audit engagement and $15,750 per tax engagement The company has its own Payroll Office, which provides payroll service to both divisions and will stocate its total expenses to the two division sport martinent location The following chart shows some basic data for the company Hourly market rate for stat (the once the company would have to pay from an outside contractor for at services) Average cost rate for staff (the average price the company is to its stall) $50 Number of paytheissued by Audition Number of paychecked by Tax Division 340 Total mense for Payroll om $29,250 Amount of an invested in Audit Division by OOR CPAS, Inc 510,000,000 5110 110 Amount of assets wested it to Do by BO CHAS, Inc. $4,000,000 Payroll Haley wise you to start by www.ets the wronice experts, Mecany the low cenies to each owon. He has decided to use the number oyroll checks as the activity be for the auction not in the flowing banks, recting the totale for the Pyramice to each of the tradition Payroll Charge are 29.250 x per para teck Support Department Division Allocations Audit Division 7.150 Tax Divaton 22,100 Performance Evaluation Articole remonty and how many contratatect everanca, u pro The age of a profit comer does normas de concerning the facts inted in the content coloring for groft center tuth as the Audit Division and Tablete the form of income statements, which we only controllati revert and controle expenses Atheis por technical centre. BORC, Inows whole may be comidered as an investments, Medinewwing the performance of the comes a wote Teo sartormance measures that are used at the investment center vel rerum inter and some Mballer would like to turtom, cod for margin and ment amover, to break cown the run on investment in the cay vision at the company leyes, Mr baie would like to run on investment to use the overall performance of the company and its indecisions with than Answer the rotoning and (3) 1. Wat is the most cely reason Batey chose the DuPont formats to evaluate the division 2. Mr Beley wants to focus on whether the trofit centers are spending in accordance with their budgets Mc Doney beleves that the investiment tumower with provide a good usmerite each one ofitabil c. Mr. Boty would like to analyse derecesitan on investment condivisions X 2. W the mountains the many as a whole Hairy would like to strmine which in the highest net come B. Return on investment wil weyts mesure the income (return) on est dosar vested us the di valors, and decide where to investitional spand operator Complete the following Divisional Income Statements with your data from the Payroll BOR CPAS, Inc. Divisional Income Statements For the Year Ended December 31, 2048 Audit Division Tax Division Total Company Fees earned: $900,000 $900,000 Audit fees (12 engagements) Tax fees (45 engagements) Transfer pricing fees $708,750 708,750 0 Expenses Variable: (180,000) Audit hours provided by Audit Division Tax hours provided by Tax Division Excess capacity hours paid to salaried staff Audit hours provided by Tax Division Fixed expenses Operating income before support department allocations (236,250) (40,000) 0 (180,000) (236,250) (40,000) 0 (50,000) (115,500) (65,500) $367,000 $670,000 $1,037,000 Support department allocations for payroll 7,150 22,100 29,250 Operating income 662,850 344,900 $ 1,007,750 Market Transfer Price Mi Baileys that you prepare Divisional Income Statements showing what 20 results would have been had the Audit Division Duched all the capacity of the Tex Diving a marvet trane The vivonal manager tell you that, win the scene capacity of the Tax DC 200 nours, the Auditorio con perform.. more audits during the vow, and the Tax Dion would charge the Audit Division market rate of $110 per hour for the addition pour record selling all its excess capacity to the Advision. The action would still be responsible for paying tha tantes e their employees Complete the following income Statements. If there is no mount counts on BOR CPAS, Inc Divisional Income Statements For the Year Ended December 31, 2018 Audit Division Tax Division Total Company Fossed Auditores (16 ngent 11.200,000 $1,200.000 Texfees (5 engagements) 5708,50 900,250 Transferring fees 120,000 120,000 (10,000) Variable Audit hours provided by Audit Division Tax hors provided by Tax Divin Excel capacity hours paid to salaried staff Audith provided by Tax Division (236.250) (100,000) (236,250) 356,250 X 40,000 X 40,000 x 120,000 x X 150,000 850,000 X (65.500) 487,000 X 22,100 115.500) 1,337,000 Operating income before support department allocations Support department allocations for payroll 7.150 29,250 OLU 7.150 22,100 29,250 Soport department allocation for roll Operating come 342,050 X 464,100 x 1,307,750 Negotiated Transfer Price Mr. Balast vous come Statements showing what results would have twen had the Austin purchased the cosity of Tax Division, in antiated trane price. The dancer til you that with the spot of the Tax Divion of hours, the Aude Division can perform a more di dung the year, and that inition would agree to swiated O S80 per hour to be paid to the Tax Division for the additional hours required, with the Tax Division selling capacity to the Adwon. The Tex Dion would still be responsible for saving the BOR CPAs, Inc. Divisional Income Statements For the Year Ended December 31, 2018 Audit Division Tax Division Total Company Fees earned: $1,200,000 $1,200,000 708,750 Audit fees (16 engagements) Tax fees (45 engagements) Transfer pricing fees $708,750 X X (180,000) (236,250) Expenses: Variable: Audit hours provided by Audit Division Tax hours provided by Tax Division Excess capacity hours paid to salaried staff Audit hours provided by Tax Division Fixed expenses (180,000) (236,250) X X (50,000) (65,500) (115,500) X $ X Operating income before support department allocations Support department allocations for payroll $ Operating income Cast Transfer Price Methet vuur Ovnemessing what we would have the capact of the world. The don muerto you that with the city of the Teen 0 hours, the de avion can perform a mere die dating the year and the button as the Taxi's internal of per hour for the house with Townseng cere a www.esponsible for wing the starter mething in the same for an BOR CPAs, Inc. Divisional Income Statements For the Year Ended December 31, 20Y8 Audit Division Tax Division Total Company $1,200,000 $1,200,000 Fees earned: Audit fees (16 engagements) Tax fees (45 engagements) Transfer pricing fees $708,750 708,750 X Expenses: Variable: Audit hours provided by Audit Division (180,000) (180,000) (236,250) Tax hours provided by Tax Division (236,250) X Excess capacity hours paid to salaried staff Audit hours provided by Tax Division Fixed expenses Operating income before support department allocations Support department allocations for payroll (50,000) (65,500) (115,500) X X X Operating income Analysis You are now able to put together all the information you've collected and analyze the data. In the following table, ROI stands for "Return on Investment." Complete the following tables using the information from the other requirements and selection lists provided. Audit Division Profit Margin Investment Turnover ROI No Transfer X X X Market Price X X X Negotiated Price Cost Price X X Tax Division X Investment Turnover ROI Profit Margin X X No Transfer Market Price X X X X Negotiated Price Cost Price BOR CPAs, Inc. Profit Margin X Investment Turnover ROI No Transfer X X X Market Price x Negotiated Price X Cost Price X Final Questions After analyzing the data, you are able to answer Mr. Bailey's questions (1) - (4) that follow 1. Given that Mr. Balley is evaluating BOR CPAS, toc, which is an investment center, what transfer pricing option(s) would be most prefer that the divisions use? a. No transfer between divisions b. Market transfer price of $110 per hour c. Negotiated transfer price of $80 per hour d. Variable standard cost transfer price of $50 per hour 2. Which transfer pricing option would the manager of the Audit Division prefer? a. No transfer between divisions b. Market transfer price of $110 per hour c. Negotiated transfer price of $80 per hour d. Variable standard cost transfer price of $50 per hour 3. Which transfer pricing option would the manager of the Tax Division . No transfer between divisions Market transfer price sito per hour Negotiated transfer price of 50 per hour d. Variable anderd cost transfer price of $50 per hour 4. civen the prefrences of the manager of the Audit and Tax Divi, considering the presence of BORC, Inc., what might be the declan that provides the best outcome for at Wels and entities within the company 3. Use the negotiated transfer price, so that nach entity is better offan it would be without any transfer between division If the divisional managers cannot come to opreme, iry best to forge any tres visions in order to reduce cont within the company The company should use the market for since it's important for the interate under al market condition d. The company should use the variable standard contraher prion, because it would be for fort Taxi to make a pronti deving with the Meditation, sincere in the company Mastery Problem: Evaluating Decentralized Operations BOR CPAS, Inc. BORCA, Te is closely held corporation owned by the stockholders who used the tal of their last names to form the corporation's name: Cyrus Daley, John Ogden, Samuel Rogers. The firm's Certified Public Accountants (CPA) perform audits of both public companies and privately owned companies. BORCA o provide tax services to both individuals and businesses The corporation is divided into two brot cantat the Audit Division and the Tax Division, a division is composed of two costantes. The Not Division is composed of two cost center departments Public Company Audits and Private Company Audits. The Tax Division is composed of two cost center departments also individual Tax and Business Tax BOR, a decentred organications interested in vaivating the performance of the two divisions. The stockholders are responsible for deciding on investment in the two divisions. Cyrus Balley is in charge of the performance evaluation, and turns to you for assistance. Mr. Bly only interested in evaluating operations at the profit center (division), and not at the cost center department) uvel Mr. Barley is considering temporarily wing some of the start from the Tae Division to set the Audit Division during the coming busy audie season, and would like to evaluate the effect of this on net income. The Tax Division is estimated to have 800 hours of excess capacity The unit for determining sales revenue in both avion is the engagement, which means the total agreed-upon work for a given cient in either audit or tax for a given year. The company charges on average for of 375,000 per audit engagement and $15,750 per tax engagement The company has its own Payroll Office, which provides payroll service to both divisions and will stocate its total expenses to the two division sport martinent location The following chart shows some basic data for the company Hourly market rate for stat (the once the company would have to pay from an outside contractor for at services) Average cost rate for staff (the average price the company is to its stall) $50 Number of paytheissued by Audition Number of paychecked by Tax Division 340 Total mense for Payroll om $29,250 Amount of an invested in Audit Division by OOR CPAS, Inc 510,000,000 5110 110 Amount of assets wested it to Do by BO CHAS, Inc. $4,000,000 Payroll Haley wise you to start by www.ets the wronice experts, Mecany the low cenies to each owon. He has decided to use the number oyroll checks as the activity be for the auction not in the flowing banks, recting the totale for the Pyramice to each of the tradition Payroll Charge are 29.250 x per para teck Support Department Division Allocations Audit Division 7.150 Tax Divaton 22,100 Performance Evaluation Articole remonty and how many contratatect everanca, u pro The age of a profit comer does normas de concerning the facts inted in the content coloring for groft center tuth as the Audit Division and Tablete the form of income statements, which we only controllati revert and controle expenses Atheis por technical centre. BORC, Inows whole may be comidered as an investments, Medinewwing the performance of the comes a wote Teo sartormance measures that are used at the investment center vel rerum inter and some Mballer would like to turtom, cod for margin and ment amover, to break cown the run on investment in the cay vision at the company leyes, Mr baie would like to run on investment to use the overall performance of the company and its indecisions with than Answer the rotoning and (3) 1. Wat is the most cely reason Batey chose the DuPont formats to evaluate the division 2. Mr Beley wants to focus on whether the trofit centers are spending in accordance with their budgets Mc Doney beleves that the investiment tumower with provide a good usmerite each one ofitabil c. Mr. Boty would like to analyse derecesitan on investment condivisions X 2. W the mountains the many as a whole Hairy would like to strmine which in the highest net come B. Return on investment wil weyts mesure the income (return) on est dosar vested us the di valors, and decide where to investitional spand operator Complete the following Divisional Income Statements with your data from the Payroll BOR CPAS, Inc. Divisional Income Statements For the Year Ended December 31, 2048 Audit Division Tax Division Total Company Fees earned: $900,000 $900,000 Audit fees (12 engagements) Tax fees (45 engagements) Transfer pricing fees $708,750 708,750 0 Expenses Variable: (180,000) Audit hours provided by Audit Division Tax hours provided by Tax Division Excess capacity hours paid to salaried staff Audit hours provided by Tax Division Fixed expenses Operating income before support department allocations (236,250) (40,000) 0 (180,000) (236,250) (40,000) 0 (50,000) (115,500) (65,500) $367,000 $670,000 $1,037,000 Support department allocations for payroll 7,150 22,100 29,250 Operating income 662,850 344,900 $ 1,007,750 Market Transfer Price Mi Baileys that you prepare Divisional Income Statements showing what 20 results would have been had the Audit Division Duched all the capacity of the Tex Diving a marvet trane The vivonal manager tell you that, win the scene capacity of the Tax DC 200 nours, the Auditorio con perform.. more audits during the vow, and the Tax Dion would charge the Audit Division market rate of $110 per hour for the addition pour record selling all its excess capacity to the Advision. The action would still be responsible for paying tha tantes e their employees Complete the following income Statements. If there is no mount counts on BOR CPAS, Inc Divisional Income Statements For the Year Ended December 31, 2018 Audit Division Tax Division Total Company Fossed Auditores (16 ngent 11.200,000 $1,200.000 Texfees (5 engagements) 5708,50 900,250 Transferring fees 120,000 120,000 (10,000) Variable Audit hours provided by Audit Division Tax hors provided by Tax Divin Excel capacity hours paid to salaried staff Audith provided by Tax Division (236.250) (100,000) (236,250) 356,250 X 40,000 X 40,000 x 120,000 x X 150,000 850,000 X (65.500) 487,000 X 22,100 115.500) 1,337,000 Operating income before support department allocations Support department allocations for payroll 7.150 29,250 OLU 7.150 22,100 29,250 Soport department allocation for roll Operating come 342,050 X 464,100 x 1,307,750 Negotiated Transfer Price Mr. Balast vous come Statements showing what results would have twen had the Austin purchased the cosity of Tax Division, in antiated trane price. The dancer til you that with the spot of the Tax Divion of hours, the Aude Division can perform a more di dung the year, and that inition would agree to swiated O S80 per hour to be paid to the Tax Division for the additional hours required, with the Tax Division selling capacity to the Adwon. The Tex Dion would still be responsible for saving the BOR CPAs, Inc. Divisional Income Statements For the Year Ended December 31, 2018 Audit Division Tax Division Total Company Fees earned: $1,200,000 $1,200,000 708,750 Audit fees (16 engagements) Tax fees (45 engagements) Transfer pricing fees $708,750 X X (180,000) (236,250) Expenses: Variable: Audit hours provided by Audit Division Tax hours provided by Tax Division Excess capacity hours paid to salaried staff Audit hours provided by Tax Division Fixed expenses (180,000) (236,250) X X (50,000) (65,500) (115,500) X $ X Operating income before support department allocations Support department allocations for payroll $ Operating income Cast Transfer Price Methet vuur Ovnemessing what we would have the capact of the world. The don muerto you that with the city of the Teen 0 hours, the de avion can perform a mere die dating the year and the button as the Taxi's internal of per hour for the house with Townseng cere a www.esponsible for wing the starter mething in the same for an BOR CPAs, Inc. Divisional Income Statements For the Year Ended December 31, 20Y8 Audit Division Tax Division Total Company $1,200,000 $1,200,000 Fees earned: Audit fees (16 engagements) Tax fees (45 engagements) Transfer pricing fees $708,750 708,750 X Expenses: Variable: Audit hours provided by Audit Division (180,000) (180,000) (236,250) Tax hours provided by Tax Division (236,250) X Excess capacity hours paid to salaried staff Audit hours provided by Tax Division Fixed expenses Operating income before support department allocations Support department allocations for payroll (50,000) (65,500) (115,500) X X X Operating income Analysis You are now able to put together all the information you've collected and analyze the data. In the following table, ROI stands for "Return on Investment." Complete the following tables using the information from the other requirements and selection lists provided. Audit Division Profit Margin Investment Turnover ROI No Transfer X X X Market Price X X X Negotiated Price Cost Price X X Tax Division X Investment Turnover ROI Profit Margin X X No Transfer Market Price X X X X Negotiated Price Cost Price BOR CPAs, Inc. Profit Margin X Investment Turnover ROI No Transfer X X X Market Price x Negotiated Price X Cost Price X Final Questions After analyzing the data, you are able to answer Mr. Bailey's questions (1) - (4) that follow 1. Given that Mr. Balley is evaluating BOR CPAS, toc, which is an investment center, what transfer pricing option(s) would be most prefer that the divisions use? a. No transfer between divisions b. Market transfer price of $110 per hour c. Negotiated transfer price of $80 per hour d. Variable standard cost transfer price of $50 per hour 2. Which transfer pricing option would the manager of the Audit Division prefer? a. No transfer between divisions b. Market transfer price of $110 per hour c. Negotiated transfer price of $80 per hour d. Variable standard cost transfer price of $50 per hour 3. Which transfer pricing option would the manager of the Tax Division . No transfer between divisions Market transfer price sito per hour Negotiated transfer price of 50 per hour d. Variable anderd cost transfer price of $50 per hour 4. civen the prefrences of the manager of the Audit and Tax Divi, considering the presence of BORC, Inc., what might be the declan that provides the best outcome for at Wels and entities within the company 3. Use the negotiated transfer price, so that nach entity is better offan it would be without any transfer between division If the divisional managers cannot come to opreme, iry best to forge any tres visions in order to reduce cont within the company The company should use the market for since it's important for the interate under al market condition d. The company should use the variable standard contraher prion, because it would be for fort Taxi to make a pronti deving with the Meditation, sincere in the company