Answered step by step

Verified Expert Solution

Question

1 Approved Answer

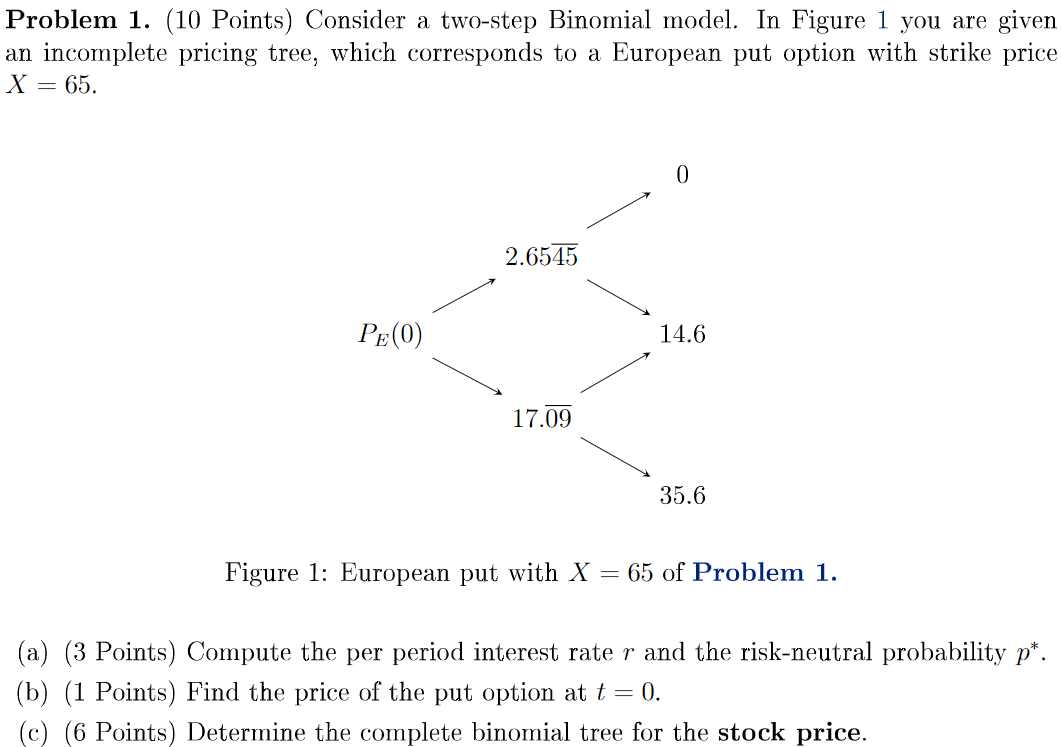

Mathematical finance question on options Problem 1. (10 Points) Consider a two-step Binomial model. In Figure 1 you are given an incomplete pricing tree, which

Mathematical finance question on options

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Macroeconomics Principles and Applications

Authors: Robert e. hall, marc Lieberman

5th edition

1111397465, 9781439038970, 1439038988, 978-1111397463, 143903897X, 9781439038987, 978-1133265238