May I please have help with the following question given with the answers in the last 3 photos... can someone please help me understand how to get the answers that do not have explanations or brackets with the math and especially the answer circled in blue?

Answer given to textbook question:

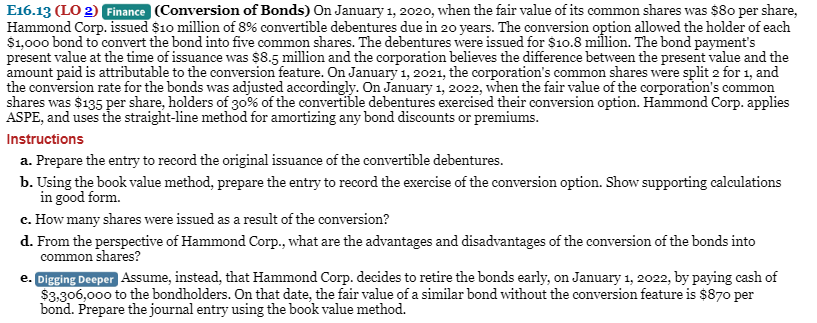

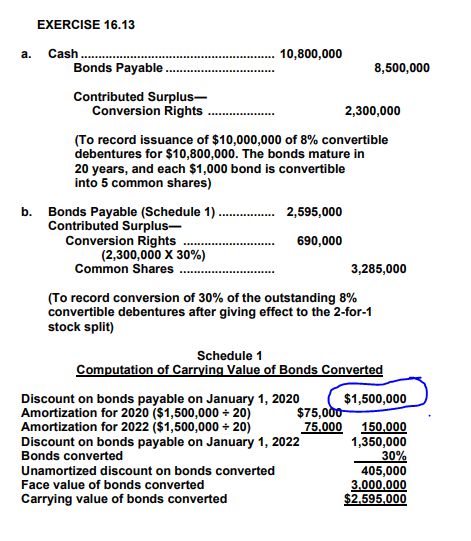

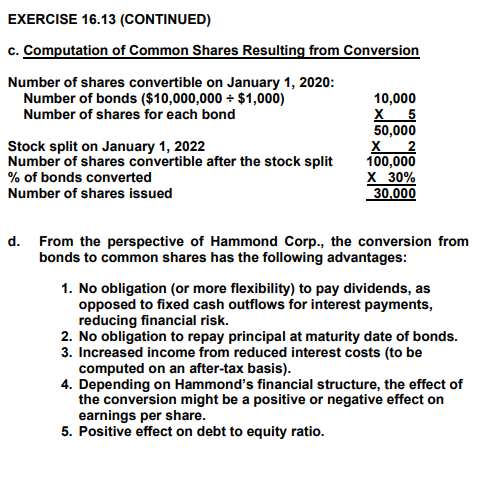

E16.13 (LO 2) Finance (Conversion of Bonds) On January 1, 2020, when the fair value of its common shares was $80 per share, Hammond Corp. issued $10 million of 8% convertible debentures due in 20 years. The conversion option allowed the holder of each $1,000 bond to convert the bond into five common shares. The debentures were issued for $10.8 million. The bond payment's present value at the time of issuance was $8.5 million and the corporation believes the difference between the present value and the amount paid is attributable to the conversion feature. On January 1, 2021, the corporation's common shares were split 2 for 1, and the conversion rate for the bonds was adjusted accordingly. On January 1, 2022, when the fair value of the corporation's common shares was $135 per share, holders of 30% of the convertible debentures exercised their conversion option. Hammond Corp. applies ASPE, and uses the straight-line method for amortizing any bond discounts or premiums. Instructions a. Prepare the entry to record the original issuance of the convertible debentures. b. Using the book value method, prepare the entry to record the exercise of the conversion option. Show supporting calculations in good form. c. How many shares were issued as a result of the conversion? d. From the perspective of Hammond Corp., what are the advantages and disadvantages of the conversion of the bonds into common shares? e. Digging Deeper Assume, instead, that Hammond Corp. decides to retire the bonds early, on January 1, 2022, by paying cash of $3,306,000 to the bondholders. On that date, the fair value of a similar bond without the conversion feature is $870 per bond. Prepare the journal entry using the book value method. EXERCISE 16.13 a. Cash Bonds Payable 10,800,000 8,500,000 Contributed Surplus- Conversion Rights 2,300,000 (To record issuance of $10,000,000 of 8% convertible debentures for $10,800,000. The bonds mature in 20 years, and each $1,000 bond is convertible into 5 common shares) b. Bonds Payable (Schedule 1). 2,595,000 Contributed Surplus- Conversion Rights 690,000 (2,300,000 X 30%) Common Shares 3,285,000 (To record conversion of 30% of the outstanding 8% convertible debentures after giving effect to the 2-for-1 stock split) Schedule 1 Computation of Carrying Value of Bonds Converted Discount on bonds payable on January 1, 2020 $1,500,000 Amortization for 2020 ($1,500,000 + 20) $75,000 Amortization for 2022 ($1,500,000 + 20) 75.000 150,000 Discount on bonds payable on January 1, 2022 1,350,000 Bonds converted 30% Unamortized discount on bonds converted 405,000 Face value of bonds converted 3,000,000 Carrying value of bonds converted $2.595,000 EXERCISE 16.13 (CONTINUED) C. Computation of Common Shares Resulting from Conversion Number of shares convertible on January 1, 2020: Number of bonds ($10,000,000 = $1,000) Number of shares for each bond Stock split on January 1, 2022 Number of shares convertible after the stock split % of bonds converted Number of shares issued 10,000 X 5 50,000 X 2 100,000 X 30% 30.000 d. From the perspective of Hammond Corp., the conversion from bonds to common shares has the following advantages: 1. No obligation (or more flexibility) to pay dividends, as opposed to fixed cash outflows for interest payments, reducing financial risk. 2. No obligation to repay principal at maturity date of bonds. 3. Increased income from reduced interest costs (to be computed on an after-tax basis). 4. Depending on Hammond's financial structure, the effect of the conversion might be a positive or negative effect on earnings per share. 5. Positive effect on debt to equity ratio. EXERCISE 16.13 (CONTINUED) d. (continued) The disadvantages of the conversion to Hammond Corporation include: 1. Dilution of earnings for existing shareholders might make shareholders unhappy; offset at least in part by higher income because less interest is paid. Existing shareholders will conceivably pressure the company not to dilute their ownership (this may actually be unlikely, as the fact of the conversion feature would have been fully disclosed since the initial issuance of the bonds, and the possibility of conversion would be fully reflected in the price of the shares). 2. Pressure from new shareholders for dividend payout. e. 15,000 2,595,000 Loss on Retirement of Bonds.......... Bonds Payable........ Contributed Surplus- Conversion Rights Retained Earnings Cash "(3,000 x $870 - $2,595,000) 690,000 6,000 3,306,000 LO 2 BT: AP Difficulty: M Time: 25 min. AACSB: Analytic CPA: CPA: cpa-001 cpa-005 CM: Reporting and Finance E16.13 (LO 2) Finance (Conversion of Bonds) On January 1, 2020, when the fair value of its common shares was $80 per share, Hammond Corp. issued $10 million of 8% convertible debentures due in 20 years. The conversion option allowed the holder of each $1,000 bond to convert the bond into five common shares. The debentures were issued for $10.8 million. The bond payment's present value at the time of issuance was $8.5 million and the corporation believes the difference between the present value and the amount paid is attributable to the conversion feature. On January 1, 2021, the corporation's common shares were split 2 for 1, and the conversion rate for the bonds was adjusted accordingly. On January 1, 2022, when the fair value of the corporation's common shares was $135 per share, holders of 30% of the convertible debentures exercised their conversion option. Hammond Corp. applies ASPE, and uses the straight-line method for amortizing any bond discounts or premiums. Instructions a. Prepare the entry to record the original issuance of the convertible debentures. b. Using the book value method, prepare the entry to record the exercise of the conversion option. Show supporting calculations in good form. c. How many shares were issued as a result of the conversion? d. From the perspective of Hammond Corp., what are the advantages and disadvantages of the conversion of the bonds into common shares? e. Digging Deeper Assume, instead, that Hammond Corp. decides to retire the bonds early, on January 1, 2022, by paying cash of $3,306,000 to the bondholders. On that date, the fair value of a similar bond without the conversion feature is $870 per bond. Prepare the journal entry using the book value method. EXERCISE 16.13 a. Cash Bonds Payable 10,800,000 8,500,000 Contributed Surplus- Conversion Rights 2,300,000 (To record issuance of $10,000,000 of 8% convertible debentures for $10,800,000. The bonds mature in 20 years, and each $1,000 bond is convertible into 5 common shares) b. Bonds Payable (Schedule 1). 2,595,000 Contributed Surplus- Conversion Rights 690,000 (2,300,000 X 30%) Common Shares 3,285,000 (To record conversion of 30% of the outstanding 8% convertible debentures after giving effect to the 2-for-1 stock split) Schedule 1 Computation of Carrying Value of Bonds Converted Discount on bonds payable on January 1, 2020 $1,500,000 Amortization for 2020 ($1,500,000 + 20) $75,000 Amortization for 2022 ($1,500,000 + 20) 75.000 150,000 Discount on bonds payable on January 1, 2022 1,350,000 Bonds converted 30% Unamortized discount on bonds converted 405,000 Face value of bonds converted 3,000,000 Carrying value of bonds converted $2.595,000 EXERCISE 16.13 (CONTINUED) C. Computation of Common Shares Resulting from Conversion Number of shares convertible on January 1, 2020: Number of bonds ($10,000,000 = $1,000) Number of shares for each bond Stock split on January 1, 2022 Number of shares convertible after the stock split % of bonds converted Number of shares issued 10,000 X 5 50,000 X 2 100,000 X 30% 30.000 d. From the perspective of Hammond Corp., the conversion from bonds to common shares has the following advantages: 1. No obligation (or more flexibility) to pay dividends, as opposed to fixed cash outflows for interest payments, reducing financial risk. 2. No obligation to repay principal at maturity date of bonds. 3. Increased income from reduced interest costs (to be computed on an after-tax basis). 4. Depending on Hammond's financial structure, the effect of the conversion might be a positive or negative effect on earnings per share. 5. Positive effect on debt to equity ratio. EXERCISE 16.13 (CONTINUED) d. (continued) The disadvantages of the conversion to Hammond Corporation include: 1. Dilution of earnings for existing shareholders might make shareholders unhappy; offset at least in part by higher income because less interest is paid. Existing shareholders will conceivably pressure the company not to dilute their ownership (this may actually be unlikely, as the fact of the conversion feature would have been fully disclosed since the initial issuance of the bonds, and the possibility of conversion would be fully reflected in the price of the shares). 2. Pressure from new shareholders for dividend payout. e. 15,000 2,595,000 Loss on Retirement of Bonds.......... Bonds Payable........ Contributed Surplus- Conversion Rights Retained Earnings Cash "(3,000 x $870 - $2,595,000) 690,000 6,000 3,306,000 LO 2 BT: AP Difficulty: M Time: 25 min. AACSB: Analytic CPA: CPA: cpa-001 cpa-005 CM: Reporting and Finance