Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Mill, Inc., has the following plant asset accounts: Land, Buildings, and Equipment, with a separate accumulated depreciation account for each of these except Land. Mill

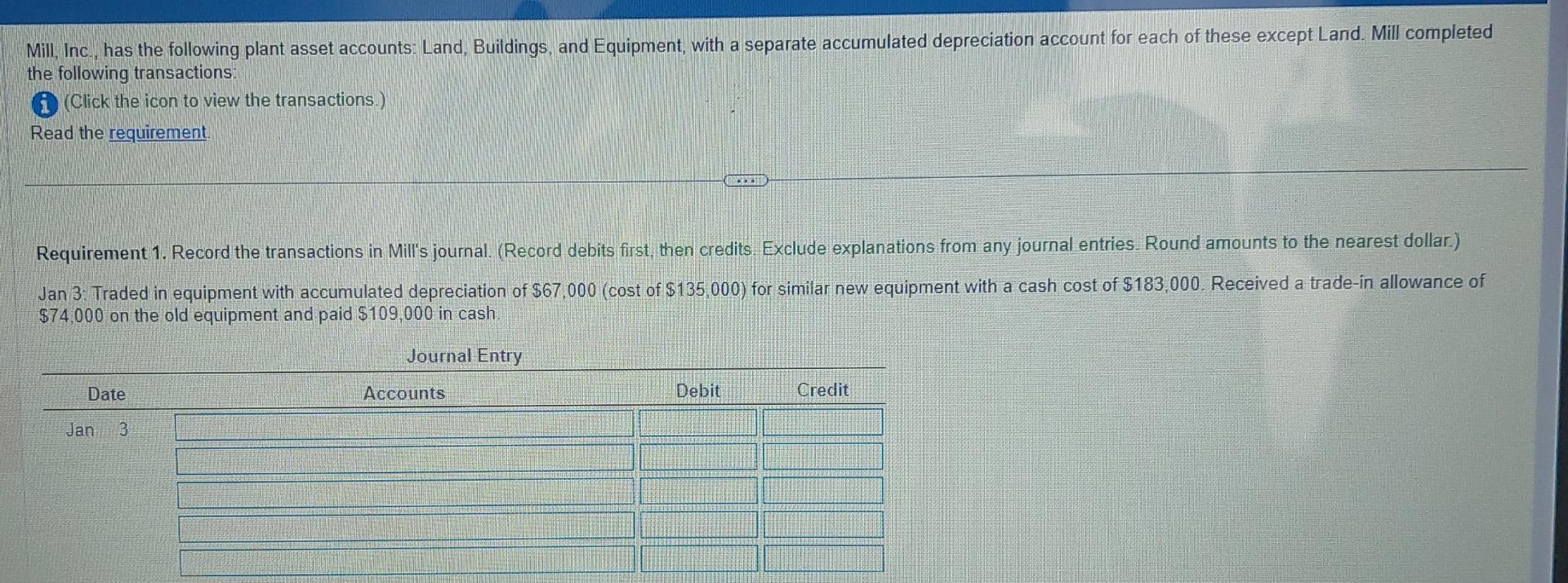

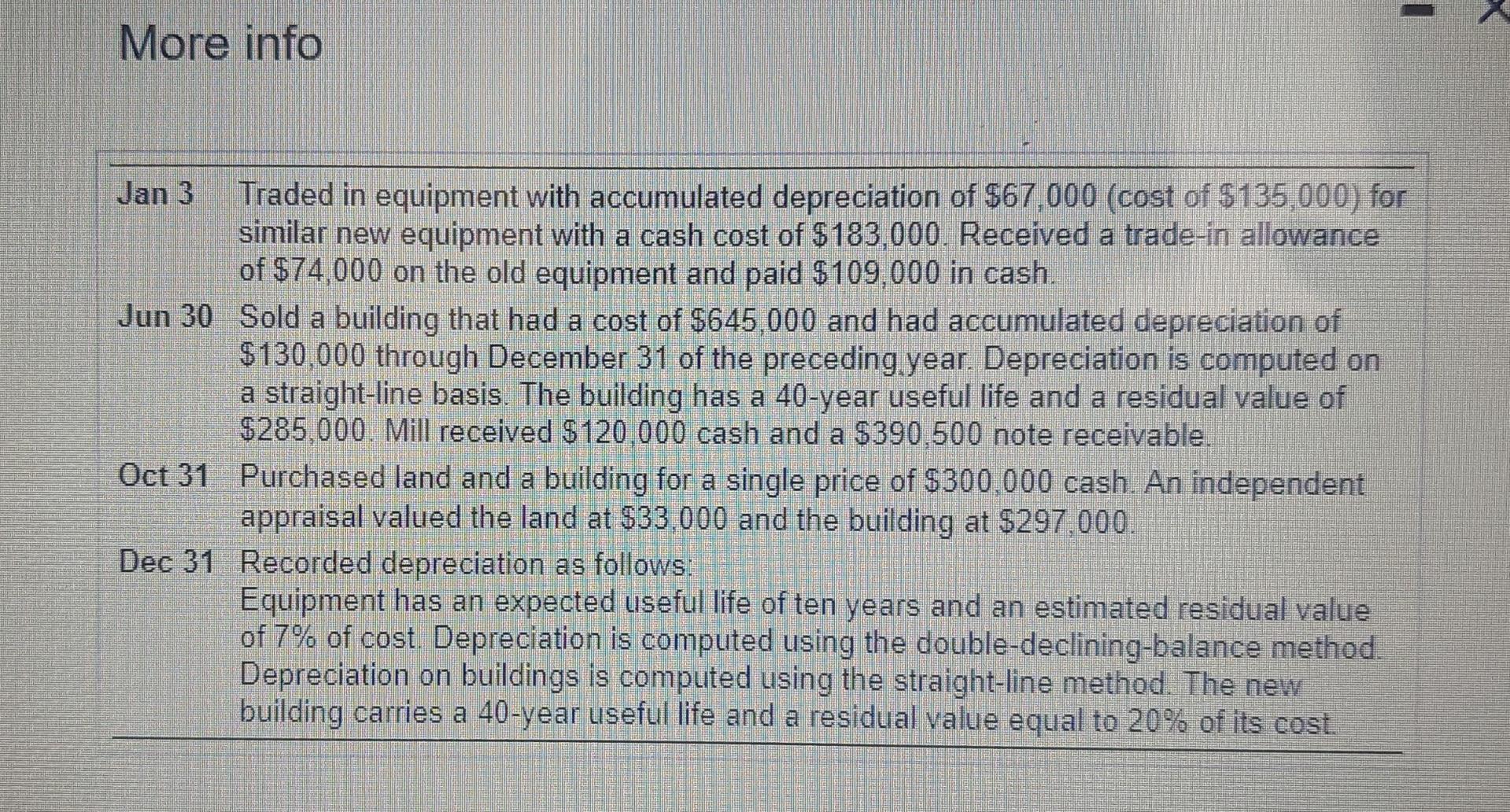

Mill, Inc., has the following plant asset accounts: Land, Buildings, and Equipment, with a separate accumulated depreciation account for each of these except Land. Mill completed the following transactions: (i) (Click the icon to view the transactions.) Requirement 1. Record the transactions in Mill's journal. (Record debits first, then credits. Exclude explanations from any journal entries. Round amounts to the nearest dollar.) Jan 3. Traded in equipment with accumulated depreciation of $67,000 (cost of $135,000 ) for similar new equipment with a cash cost of $183,000. Received a trade-in allowance of $74,000 on the old equipment and paid $109,000 in cash. More info Jan 3 Traded in equipment with accumulated depreciation of $67,000 (cost of $135,000 ) for similar new equipment with a cash cost of $183,000. Received a trade-in allowance of $74,000 on the old equipment and paid $109,000 in cash. Jun 30 Sold a building that had a cost of $645,000 and had accumulated depreciation of $130,000 through December 31 of the preceding.year. Depreciation is computed on a straight-line basis. The building has a 40 -year useful life and a residual value of $285,000. Mill received $120,000 cash and a $390,500 note receivable. Oct 31 Purchased land and a building for a single price of $300,000 cash. An independent appraisal valued the land at $33,000 and the building at $297,000. Dec 31 Recorded depreciation as follows: Equipment has an expected useful life of ten years and an estimated residual value of 7% of cost. Depreciation is computed using the double-declining-balance method. Depreciation on buildings is computed using the straight-line method. The new building carries a 40 -year useful life and a residual value equal to 20% of its cost. Requirement 1. Record the transactions in Mill's journal

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Knowledge Audit A Complete Guide

Authors: The Art Of Service - Knowledge Audit Publishing

2021 Edition

1867424010, 978-1867424017