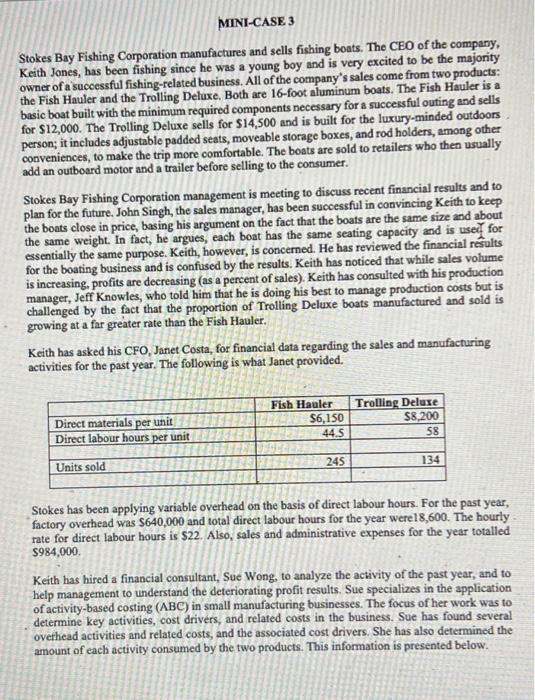

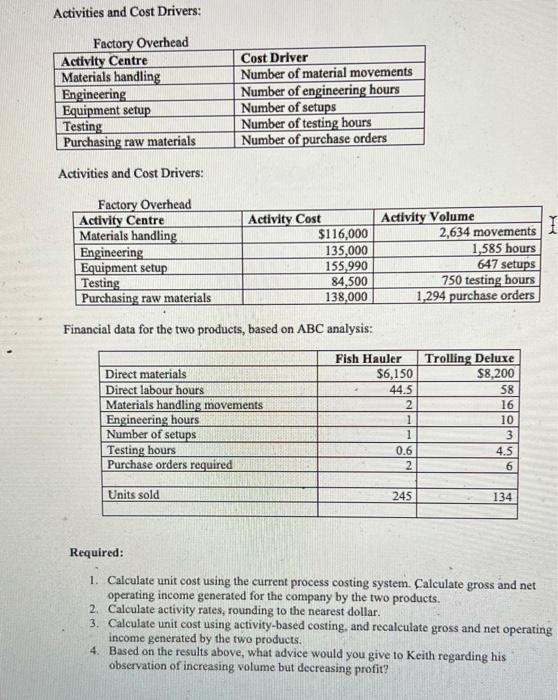

MINI-CASE 3 Stokes Bay Fishing Corporation manufactures and sells fishing boats. The CEO of the company, Keith Jones, has been fishing since he was a young boy and is very excited to be the majority owner of a successful fishing-related business. All of the company's sales come from two products: the Fish Hauler and the Trolling Deluxe. Both are 16-foot aluminum boats. The Fish Hauler is a basic boat built with the minimum required components necessary for a successful outing and sells for $12,000. The Trolling Deluxe sells for $14,500 and is built for the luxury-minded outdoors person; it includes adjustable padded seats, moveable storage boxes, and rod holders, among other conveniences, to make the trip more comfortable. The boats are sold to retailers who then usually add an outboard motor and a trailer before selling to the consumer. Stokes Bay Fishing Corporation management is meeting to discuss recent financial results and to plan for the future. John Singh, the sales manager, has been successful in convincing Keith to keep the boats close in price, basing his argument on the fact that the boats are the same size and about the same weight. In fact, he argues, each boat has the same seating capecity and is user for essentially the same purpose. Keith, however, is concerned. He has reviewed the financial results for the boating business and is confused by the results. Keith has noticed that while sales volume is increasing, profits are decreasing (as a percent of sales). Keith has consulted with his production manager, Jeff Knowles, who told him that he is doing his best to manage production costs but is challenged by the fact that the proportion of Trolling Deluxe boats manufactured and sold is growing at a far greater rate than the Fish Hauler. Keith has asked his CFO, Janet Costa, for financial data regarding the sales and manufacturing activities for the past year. The following is what Janet provided. Stokes has been applying variable overhead on the basis of direct labour hours. For the past year, factory overhead was $640,000 and total direct labour hours for the year were 18,600 . The hourly rate for direct labour hours is \$22. Also, sales and administrative expenses for the year totalled $984,000. Keith has hired a financial consultant, Sue Wong, to analyze the activity of the past year, and to help management to understand the deteriorating profit results. Sue specializes in the application of activity-based costing ( ABC ) in small manufacturing businesses. The focus of her work was to determine key activities, cost drivers, and related costs in the business. Sue has found several overhead activities and related costs, and the associated cost drivers. She has also determined the amount of each activity consumed by the two products. This information is presented below. Activities and Cost Drivers: Activities and Cost Drivers: Financial data for the two products, based on ABC analysis: Required: 1. Calculate unit cost using the current process costing system. Calculate gross and net operating income generated for the company by the two products. 2. Calculate activity rates, rounding to the nearest dollar. 3. Calculate unit cost using activity-based costing, and recalculate gross and net operating income generated by the two products. 4. Based on the results above, what advice would you give to Keith regarding his observation of increasing volume but decreasing profit