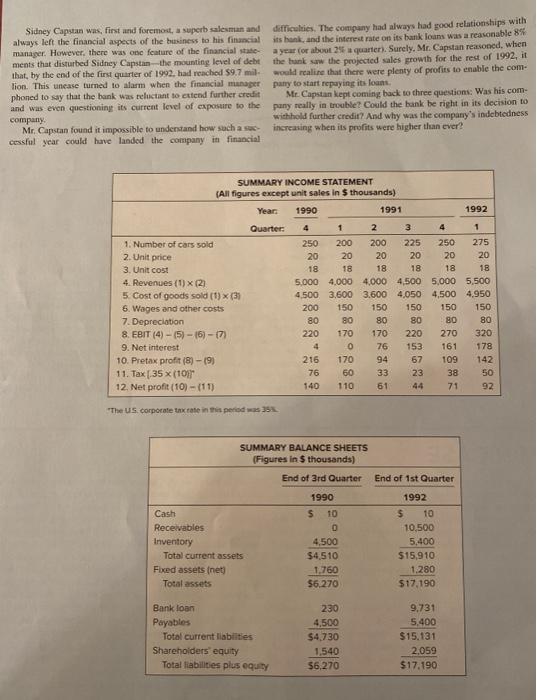

MINICASE Capstan Autos operated an East Coast dealership for a major Japa- dealers in imported cars. Capstan, more than most firms, foresaw the nese car manufacturer. Capstan's owner, Sidney Capstan, attributed difficulties ahead and reacted at once by offering 6 months free much of the business's success to its no-frills policy of competitive credit while holding the sale price of its cars constant. Wages and pricing and immediate cash payment. The business was basically a other costs were pared by 25% to $150,000 a quarter, and the com- simple one-the firm imported cars at the beginning of each quar- pany effectively eliminated all capital expenditures. The policy ter and paid the manufacturer at the end of the quarter. The reve- appeared successful. Unit sales fell by 20% to 200 units a quarter, but nues from the sale of these cars covered the payment to the the company continued to operate at a satisfactory profit (see table). manufacturer and the expenses of running the business, as well as The slump in sales lasted for 6 months, but as consumer confi- providing Sidney Capstan with a good return on his equity dence began to return, auto sales began to recover. The company's Investment. new policy of 6 months free credit was proving sufficiently popu- By the fourth quarter of 1990, sales were running at 250 cars a lar that Sidney Capstan decided to maintain the policy. In the third quarter. Because the average sale price of each car was about quarter of 1991. sales had recovered to 225 units: by the fourth $20,000, this translated into quarterly revenues of 250 x $20,000 = quarter, they were 250 units; and by the first quarter of the next $5 million. The average cost to Capstan of each imported car was year, they had reached 275 units. It looked as if, by the second $18,000. After paying wages, rent, and other recurring costs of quarter of 1992, the company could expect to sell 300 cars. Earn- $200.000 per quarter and deducting depreciation of $80,000, the ings before interest and taxes were already in excess of their previ- company was left with earnings before interest and taxes (EBIT) of ous high, and Sidney Capstan was able to congratulate himself on $220,000 a quarter and net profits of $140,000 weathering what looked to be a tricky period. Over the 18-month The year 1991 was not a happy year for car importers in the period, the firm had earned net profits of more than half a million United States. Recession led to a general decline in auto sales, while dollars, and the equity had grown from just over $1.5 million to the fall in the value of the dollar shaved profit margins for many about $2 million Sidney Capstan was, first and foremost, a superb salesman and always left the financial aspects of the business to his financial manager. However, there was one feature of the financial state ments that disturbed Sidney Capstan the mounting level of debt that, by the end of the first quarter of 1992, had reached $9.7 mill. lion. This unease turned to alarm when the financial manager phoned to say that the bank was rectant to extend further credit and was even questioning its current level of exposure to the company Mr. Capstan found it impossible to understand how such as cessful year could have landed the company in financial difficulties. The company had always had good relationships with itshank, and the interest rate on its bank loans was a reasonable 8% a year for about 25 quarters. Surely. Mr. Capstan reasoned, when the bun saw the projected sales growth for the rest of 1992, it would realise that there were plenty of profits to enable the com- patry to start repaying its louns Mt. Capstan kept coming back to three questions: Was his com- pany really in trouble? Could the bank be right in its decision to withhold further credit? And why was the company's indebtedness increasing when its profits were higher than ever? 225 SUMMARY INCOME STATEMENT (All figures except unit sales in 5 thousands) Year: 1990 1991 1992 Quarter: 4 1 2 3 4 1 1. Number of cars sold 250 200 200 250 275 2. Unit price 20 20 20 20 20 20 3. Unit cost 18 18 18 18 18 18 4. Revenues (1) x (2) 5,000 4,000 4,000 4,500 5,000 5.500 5. Cost of goods sold (1) X (3) 4.500 3.600 3.600 4.050 4,500 4.950 6. Wages and other costs 200 150 150 150 150 150 7. Depreciation 80 80 80 80 80 80 8. EBIT (4) -(5)-15) - 7 220 170 170 220 270 320 9. Net interest 4 0 76 153 178 10. Pretax profit (8) - 19) 216 170 94 67 109 142 11. Tax [.35 x (107 76 60 33 23 38 50 12. Net profit (10) - (11) 140 110 61 44 71 92 161 "The US. corporate tax rate in this period was 35% SUMMARY BALANCE SHEETS (Figures in thousands) End of 3rd Quarter End of 1st Quarter 1990 1992 Cash $ 10 $ 10 Receivables 0 10,500 Inventory 4.500 5,400 Total current assets $4,510 $15,910 Fixed assets (net 1,760 1.280 Total assets $6.270 $17,190 Bank loan Payables Total current liabilities Shareholders' equity Total liabilities plus equity 230 4,500 $4.730 1,540 $6,270 9.731 5,400 $15.131 2,059 $17,190 MINICASE Capstan Autos operated an East Coast dealership for a major Japa- dealers in imported cars. Capstan, more than most firms, foresaw the nese car manufacturer. Capstan's owner, Sidney Capstan, attributed difficulties ahead and reacted at once by offering 6 months free much of the business's success to its no-frills policy of competitive credit while holding the sale price of its cars constant. Wages and pricing and immediate cash payment. The business was basically a other costs were pared by 25% to $150,000 a quarter, and the com- simple one-the firm imported cars at the beginning of each quar- pany effectively eliminated all capital expenditures. The policy ter and paid the manufacturer at the end of the quarter. The reve- appeared successful. Unit sales fell by 20% to 200 units a quarter, but nues from the sale of these cars covered the payment to the the company continued to operate at a satisfactory profit (see table). manufacturer and the expenses of running the business, as well as The slump in sales lasted for 6 months, but as consumer confi- providing Sidney Capstan with a good return on his equity dence began to return, auto sales began to recover. The company's Investment. new policy of 6 months free credit was proving sufficiently popu- By the fourth quarter of 1990, sales were running at 250 cars a lar that Sidney Capstan decided to maintain the policy. In the third quarter. Because the average sale price of each car was about quarter of 1991. sales had recovered to 225 units: by the fourth $20,000, this translated into quarterly revenues of 250 x $20,000 = quarter, they were 250 units; and by the first quarter of the next $5 million. The average cost to Capstan of each imported car was year, they had reached 275 units. It looked as if, by the second $18,000. After paying wages, rent, and other recurring costs of quarter of 1992, the company could expect to sell 300 cars. Earn- $200.000 per quarter and deducting depreciation of $80,000, the ings before interest and taxes were already in excess of their previ- company was left with earnings before interest and taxes (EBIT) of ous high, and Sidney Capstan was able to congratulate himself on $220,000 a quarter and net profits of $140,000 weathering what looked to be a tricky period. Over the 18-month The year 1991 was not a happy year for car importers in the period, the firm had earned net profits of more than half a million United States. Recession led to a general decline in auto sales, while dollars, and the equity had grown from just over $1.5 million to the fall in the value of the dollar shaved profit margins for many about $2 million Sidney Capstan was, first and foremost, a superb salesman and always left the financial aspects of the business to his financial manager. However, there was one feature of the financial state ments that disturbed Sidney Capstan the mounting level of debt that, by the end of the first quarter of 1992, had reached $9.7 mill. lion. This unease turned to alarm when the financial manager phoned to say that the bank was rectant to extend further credit and was even questioning its current level of exposure to the company Mr. Capstan found it impossible to understand how such as cessful year could have landed the company in financial difficulties. The company had always had good relationships with itshank, and the interest rate on its bank loans was a reasonable 8% a year for about 25 quarters. Surely. Mr. Capstan reasoned, when the bun saw the projected sales growth for the rest of 1992, it would realise that there were plenty of profits to enable the com- patry to start repaying its louns Mt. Capstan kept coming back to three questions: Was his com- pany really in trouble? Could the bank be right in its decision to withhold further credit? And why was the company's indebtedness increasing when its profits were higher than ever? 225 SUMMARY INCOME STATEMENT (All figures except unit sales in 5 thousands) Year: 1990 1991 1992 Quarter: 4 1 2 3 4 1 1. Number of cars sold 250 200 200 250 275 2. Unit price 20 20 20 20 20 20 3. Unit cost 18 18 18 18 18 18 4. Revenues (1) x (2) 5,000 4,000 4,000 4,500 5,000 5.500 5. Cost of goods sold (1) X (3) 4.500 3.600 3.600 4.050 4,500 4.950 6. Wages and other costs 200 150 150 150 150 150 7. Depreciation 80 80 80 80 80 80 8. EBIT (4) -(5)-15) - 7 220 170 170 220 270 320 9. Net interest 4 0 76 153 178 10. Pretax profit (8) - 19) 216 170 94 67 109 142 11. Tax [.35 x (107 76 60 33 23 38 50 12. Net profit (10) - (11) 140 110 61 44 71 92 161 "The US. corporate tax rate in this period was 35% SUMMARY BALANCE SHEETS (Figures in thousands) End of 3rd Quarter End of 1st Quarter 1990 1992 Cash $ 10 $ 10 Receivables 0 10,500 Inventory 4.500 5,400 Total current assets $4,510 $15,910 Fixed assets (net 1,760 1.280 Total assets $6.270 $17,190 Bank loan Payables Total current liabilities Shareholders' equity Total liabilities plus equity 230 4,500 $4.730 1,540 $6,270 9.731 5,400 $15.131 2,059 $17,190