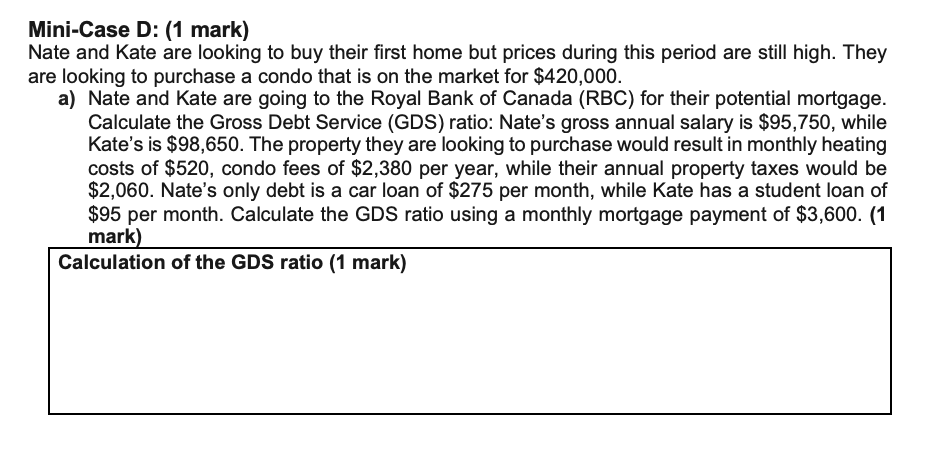

Mini-Case D: (1 mark) Nate and Kate are looking to buy their first home but prices during this period are still high. They are looking

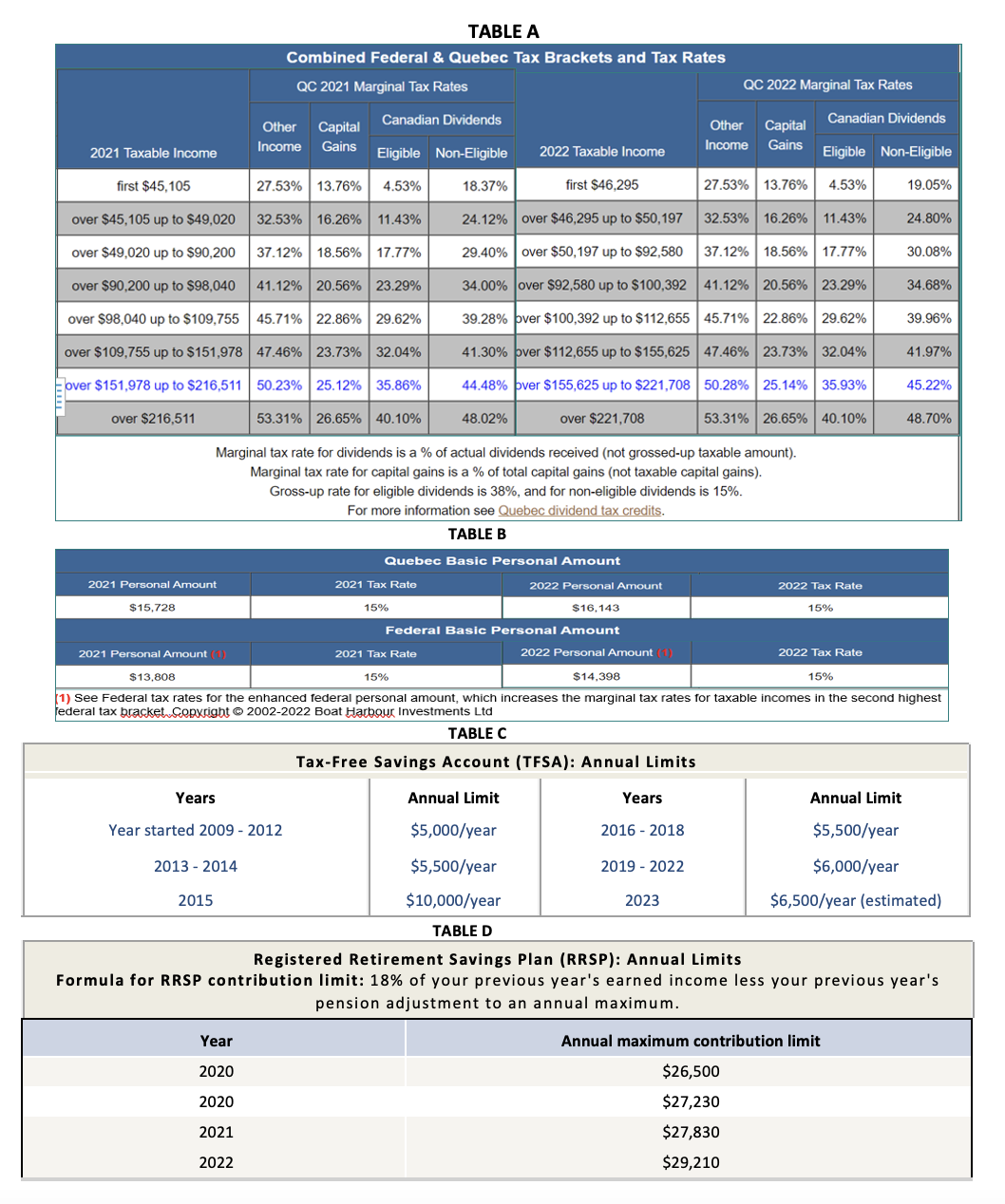

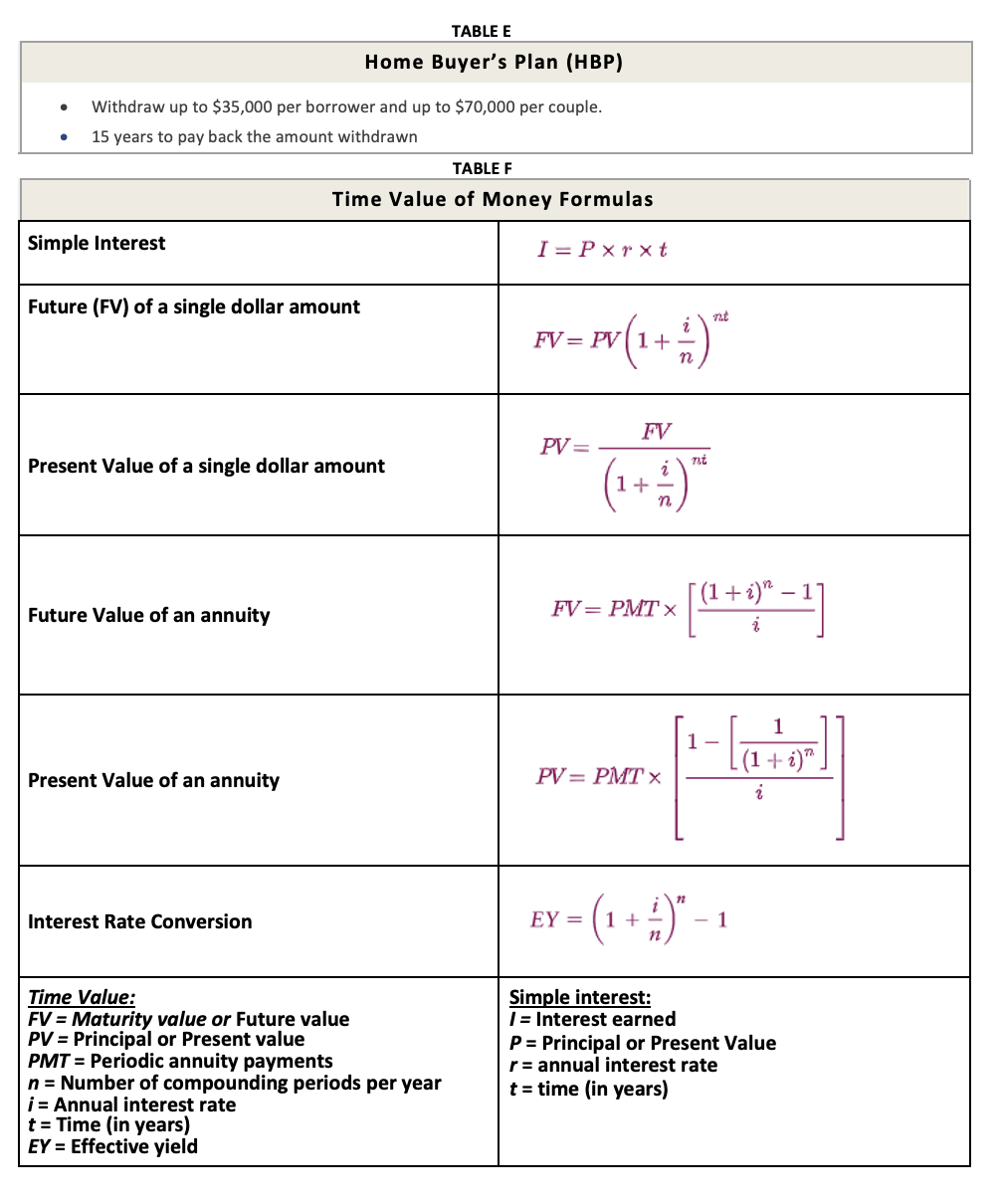

Mini-Case D: (1 mark) Nate and Kate are looking to buy their first home but prices during this period are still high. They are looking to purchase a condo that is on the market for $420,000. a) Nate and Kate are going to the Royal Bank of Canada (RBC) for their potential mortgage. Calculate the Gross Debt Service (GDS) ratio: Nate's gross annual salary is $95,750, while Kate's is $98,650. The property they are looking to purchase would result in monthly heating costs of $520, condo fees of $2,380 per year, while their annual property taxes would be $2,060. Nate's only debt is a car loan of $275 per month, while Kate has a student loan of $95 per month. Calculate the GDS ratio using a monthly mortgage payment of $3,600. (1 mark) Calculation of the GDS ratio (1 mark)TABLE A Combined Federal & Quebec Tax Brackets and Tax Rates QC 2021 Marginal Tax Rates QC 2022 Marginal Tax Rates Canadian Dividends Other Capital Canadian Dividends Other Capital 2021 Taxable Income Income Gains 2022 Taxable Income Gains Eligible Non-Eligible Income Eligible Non-Eligible first $45,105 27.53% 13.76% 4.53% 18.37% first $46,295 27.53% 13.76% 4.53% 19.05% over $45,105 up to $49,020 32.53% 16.26% 11.43% 24.12% over $46,295 up to $50, 197 32.53% 16.26% 11.43% 24.80% over $49,020 up to $90,200 37.12% 18.56% 17.77% 29.40% over $50, 197 up to $92,580 37.12% 18.56% 17.77% 30.08% over $90,200 up to $98,040 41.12% 20.56% 23.29% 34.00% over $92,580 up to $100,392 41.12% 20.56% 23.29% 34.68% over $98,040 up to $109,755 45.71% 22.86% 29.62% 39.28% over $100,392 up to $112,655 45.71% 22.86% 29.62% 39.96% over $109,755 up to $151,978 47.46% 23.73% 32.04% 41.30% over $112,655 up to $155,625 47.46% 23.73% 32.04% 41.97% over $151,978 up to $216,511 50.23% 25.12% 35.86% 44.48% over $155,625 up to $221,708 50.28% 25.14% 35.93% 45.22% over $216,511 53.31% 26.65% 40.10% 48.02% over $221,708 53.31% 26.65% 40.10% 48.70% Marginal tax rate for dividends is a % of actual dividends received (not grossed-up taxable amount). Marginal tax rate for capital gains is a % of total capital gains (not taxable capital gains). Gross-up rate for eligible dividends is 38%, and for non-eligible dividends is 15%. For more information see Quebec dividend tax credits. TABLE B Quebec Basic Personal Amount 2021 Personal Amount 2021 Tax Rate 2022 Personal Amount 2022 Tax Rate $15,728 15% $16,143 15% Federal Basic Personal Amount 2021 Personal Amount (1) 2021 Tax Rate 2022 Personal Amount (1) 2022 Tax Rate $13,808 15% $14,398 15% 1) See Federal tax rates for the enhanced federal personal amount, which increases the marginal tax rates for taxable incomes in the second highest federal tax bracket Copyright @ 2002-2022 Boat Harbour Investments Lid TABLE C Tax-Free Savings Account (TFSA): Annual Limits Years Annual Limit Year Annual Limit Year started 2009 - 2012 $5,000/year 2016 - 2018 $5,500/year 2013 - 2014 $5,500/year 2019 - 2022 $6,000/year 2015 $10,000/year 2023 $6,500/year (estimated) TABLE D Registered Retirement Savings Plan (RRSP): Annual Limits Formula for RRSP contribution limit: 18% of your previous year's earned income less your previous year's pension adjustment to an annual maximum. Year Annual maximum contribution limit 2020 $26,500 2020 $27,230 2021 $27,830 2022 $29,210TABLEE Home Buyer's Plan (HBP) - Withdraw up to $35,000 per borrower and up to $70,000 per couple. a 15 years to pay back the amount withdrawn TABLE F Time Value of Money Formulas Future (FV) of a single dollar amount Present Value of a single dollar amount Future Value of an annuity Present Value of an annuity Interest Rate Conversion Time Value: Simple interest: FV= Maturity value or Future value i: Interest earned PV= Principal or Present value p = Principal or Present Value PMT= Periodic annuity payments r = annual interest rate n = Number of compounding periods per year t = time (in years) if: Annual interest rate r = Time (in years) EY = Effective yield

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance