Question: Mirabella, Inc. sells security equipment, usually along with computer integration services. It does not sell these separately. The equipment cannot operate without being fully integrated

Mirabella, Inc. sells security equipment, usually along with computer integration services. It does not sell these separately. The equipment cannot operate without being fully integrated with a computer system. Significant customization is required during this integration. Other competitors could theoretically provide the computer integration services.

The sales manager for Mirabella has just obtained a signed contract from Jemison Brothers to provide and perform computer integration services for security equipment at a cost of $10 million, and to have everything operational within one year, at which time full payment is due. Jemison will not get control of the equipment until the integration is completed. Management expects to have the system fully operational and available for Jemison’s use in the 12th month of the contract.

In the initial contract negotiation stage, the contract price with Jemison was $10.1 million in cash. However, as part of the final contract negotiations, Jemison agrees to give Mirabella its old security equipment in exchange for a credit of $100,000. It is expected that this old security equipment will not be decommissioned until the new equipment is operational. Based on its extensive experience, Mirabella believes it is probable that the estimated fair value of the old equipment at the contract inception date is $115, 000.

There is a provision in the contract that Jemison will receive a discount of $500,000 from the contract price of $10 million if they pay within three days of the date the contract is signed. Jemison wired $9.5 million to Mirabella two days after the contract was signed.

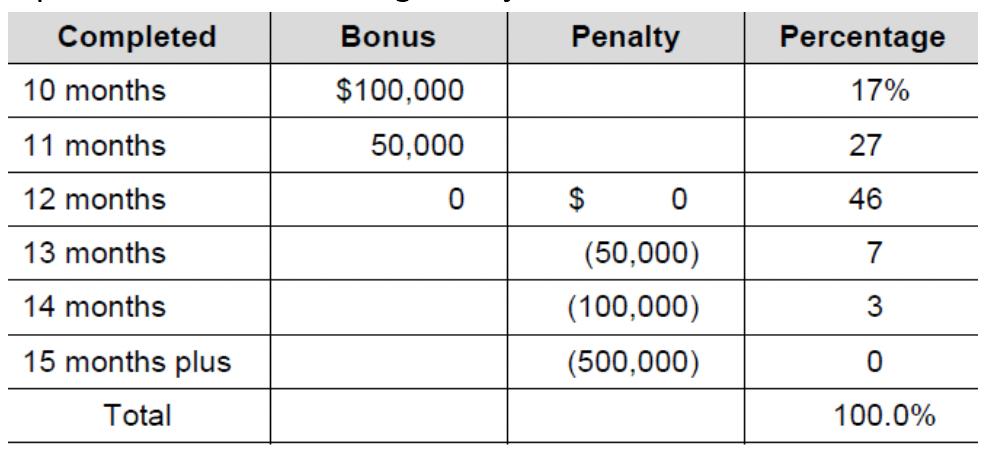

Jemison has offered a bonus to Mirabella if the integration is completed early and Mirabella agreed to pay a penalty if the integration is completed late. Mirabella has a large number of contracts with bonus characteristics similar to the contract with Jemison. The following is the schedule of the potential bonus or penalty. While no specific outcome is probable, Mirabella’s management assessment of the likelihood of completing the integration in the specified time fame is based on significant historical experience with similar integration jobs.

Analyze steps 1 through 3 of the revenue recognition model, i.e. identify the contract, identify the performance obligations, and determine the transaction price. Make sure to address, among the other issues, how the variable consideration issues should be treated and how the non-cash consideration of the old equipment should be treated. For purposes of this case, you can ignore time value of money issues.

Completed Bonus Penalty Percentage 10 months $100,000 17% 11 months 50,000 27 12 months $ 46 13 months (50,000) 7 14 months (100,000) 15 months plus (500,000) Total 100.0%

Step by Step Solution

There are 3 Steps involved in it

Prior to recognition of revenue the following criteria must be fulfilled in accordance to generally accepted accounting practices GAAPs A Risks and rewards benefits of ownership have been transferred ... View full answer

Get step-by-step solutions from verified subject matter experts