Answered step by step

Verified Expert Solution

Question

1 Approved Answer

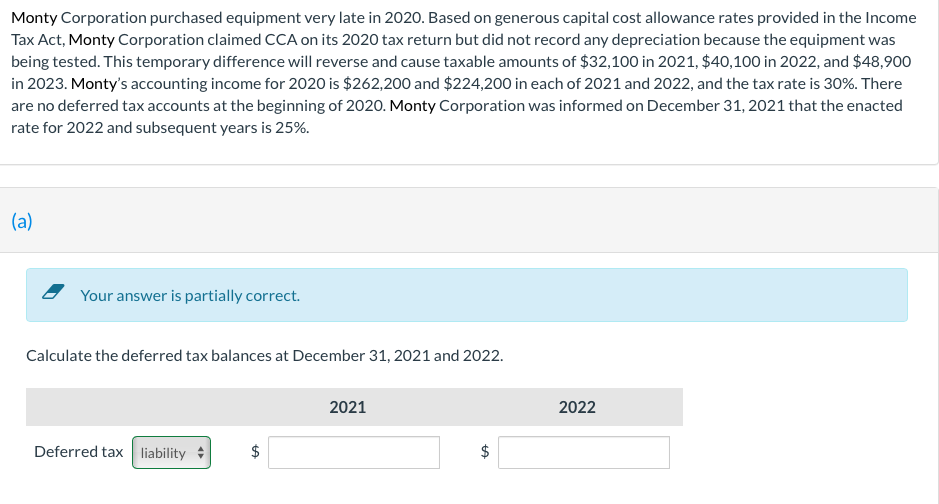

Monty Corporation purchased equipment very late in 2020. Based on generous capital cost allowance rates provided in the Income Tax Act, Monty Corporation claimed CCA

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Management Accounting

Authors: Donna K. Ulmer

7th Edition

0324234880, 978-0324234886