Question

Morelli Electric Motor Corporation manufactures electric motors for commercial use. The company produces three models, designated as standard, deluxe, and heavy-duty. The company uses a

Morelli Electric Motor Corporation manufactures electric motors for commercial use. The company produces three models, designated as standard, deluxe, and heavy-duty. The company uses a job-order cost-accounting system with manufacturing overhead applied on the basis of direct-labor hours. The system has been in place with little change for 25 years. Product costs and annual sales data are as follows:

Standard ModelDeluxe ModelHeavy-Duty ModelAnnual sales (units) 19,000 1,300 9,200 Product costs: Raw material $10 $25 $50 Direct labor 10(0.5 hr. at $20) 20(1 hr. at $20) 20(1 hr. at $20)Manufacturing overhead* 50 100 100 Total product cost $70 $145 $170

*The calculation of the predetermined overhead rate is as follows:

Manufacturing-overhead budget: Depreciation, machinery$1,320,000 Maintenance, machinery 120,000 Depreciation, taxes, and insurance for factory 200,000 Engineering 250,000 Purchasing, receiving and shipping 200,000 Inspection and repair of defects 290,000 Material handling 350,000 Miscellaneous manufacturing overhead costs 270,000 Total$3,000,000

Direct-labor budget: Standard model: 13,000 hours Deluxe model: 4,000 hours Heavy-duty model: 13,000 hours Total 30,000 hours

Predetermined overhead rate:Budgeted overhead=$3,000,000= $100 per hourBudgeted direct-labor hours30,000 hours

For the past 10 years, the companys pricing formula has been to set each products target price at 115 percent of its full product cost. Recently, however, the standard-model motor has come under increasing price pressure from offshore competitors. The result was that the price on the standard model has been lowered to $115. The company president recently asked the controller, Why cant we compete with these other companies? Theyre selling motors just like our standard model for 97 dollars. Thats only a buck more than our production cost. Are we really that inefficient? What gives? The controller responded by saying, I think this is due to an outmoded product-costing system. As you may remember, I raised a red flag about our system when I came on board last year. But the decision was to keep our current system in place. In my judgment, our product-costing system is distorting our product costs. Let me run a few numbers to demonstrate what I mean. Getting the presidents go-ahead, the controller compiled the basic data needed to implement an activity-based costing system. These data are displayed in the following table. The percentages are the proportion of each cost driver consumed by each product line.

Product Lines Activity Cost PoolCost DriverStandard ModelDeluxe ModelHeavy-Duty ModelI.Depreciation, machinery Maintenance, machineryMachine time 38% 16% 46% II.Engineering Inspection and repair of defectsEngineering hours 46% 8% 46% III.Purchasing, receiving, and shipping Material handlingNumber of material orders 46% 10% 44% IV.Depreciation, taxes, and insurance for factory Miscellaneous manufacturing overheadFactory space usage 40% 19% 41%

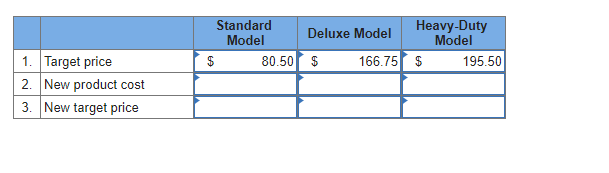

Required: 1. Compute the target prices for the three models, based on the traditional, volume-based product-costing system. 2. Compute new product costs for the three products, based on the new data collected by the controller. 3. Calculate a new target price for the three products, based on the activity-based costing system. (For all requirements, round your intermediate calculations and final answers to 2 decimal places.)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

CA FOUNDATION FINANCIAL ACCOUNTING BY NSHAH MODULE I

Authors: Sanjay Nanak Chand Thadhani

1st Edition

172887419X, 978-1728874197