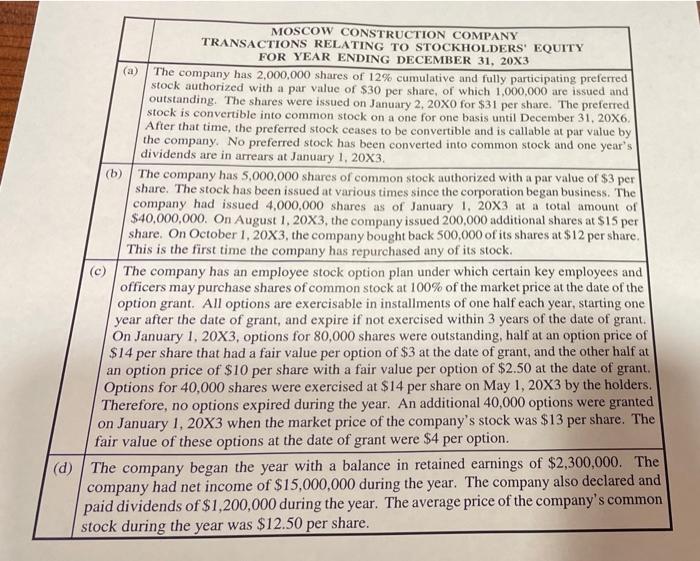

Moscow Construction Company had the attached information related to its stockholders' equity for the year ending December 31, 20X3. REQUIRED: (1) (2) Calculate the amount of dividends that should have been paid to the preferred stockholders and the amount of dividends that should have been paid to the common stockholders during the year. Show appropriate supporting calculations Prepare the stockholders' equity section of the balance sheet for the company, in proper form, at December 31, 20X3. Calculate the basic earnings per share and the diluted earnings per share for the company that should be reported on the income statement for the year ending December 31, 20X3. Round all computations for shares to the nearest whole share and the earnings per share amount to the nearest cent. Show all supporting calculations. (3) MOSCOW CONSTRUCTION COMPANY TRANSACTIONS RELATING TO STOCKHOLDERS' EQUITY FOR YEAR ENDING DECEMBER 31, 20X3 (a) The company has 2,000,000 shares of 12% cumulative and fully participating preferred stock authorized with a par value of $30 per share, of which 1,000,000 are issued and outstanding. The shares were issued on January 2, 20X0 for $31 per share. The preferred stock is convertible into common stock on a one for one basis until December 31, 20X6. After that time, the preferred stock ceases to be convertible and is callable at par value by the company. No preferred stock has been converted into common stock and one year's dividends are in arrears at January 1, 20X3. (b) The company has 5,000,000 shares of common stock authorized with a par value of $3 per share. The stock has been issued at various times since the corporation began business. The company had issued 4,000,000 shares as of January 1, 20X3 at a total amount of $40,000,000. On August 1, 20X3, the company issued 200,000 additional shares at $15 per share. On October 1, 20X3, the company bought back 500,000 of its shares at $12 per share. This is the first time the company has repurchased any of its stock (c) The company has an employee stock option plan under which certain key employees and officers may purchase shares of common stock at 100% of the market price at the date of the option grant. All options are exercisable in installments of one half each year, starting one year after the date of grant, and expire if not exercised within 3 years of the date of grant. On January 1, 20X3, options for 80,000 shares were outstanding, half at an option price of $14 per share that had a fair value per option of $3 at the date of grant, and the other half at an option price of $10 per share with a fair value per option of $2.50 at the date of grant. Options for 40,000 shares were exercised at $14 per share on May 1, 20X3 by the holders. Therefore, no options expired during the year. An additional 40,000 options were granted on January 1, 20X3 when the market price of the company's stock was $13 per share. The fair value of these options at the date of grant were $4 per option. (d) The company began the year with a balance in retained earnings of $2,300,000. The company had net income of $15,000,000 during the year. The company also declared and paid dividends of $1,200,000 during the year. The average price of the company's common stock during the year was $12.50 per share. a