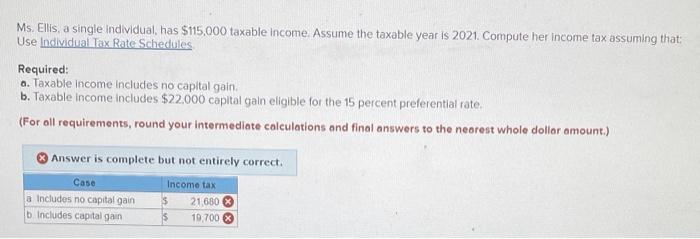

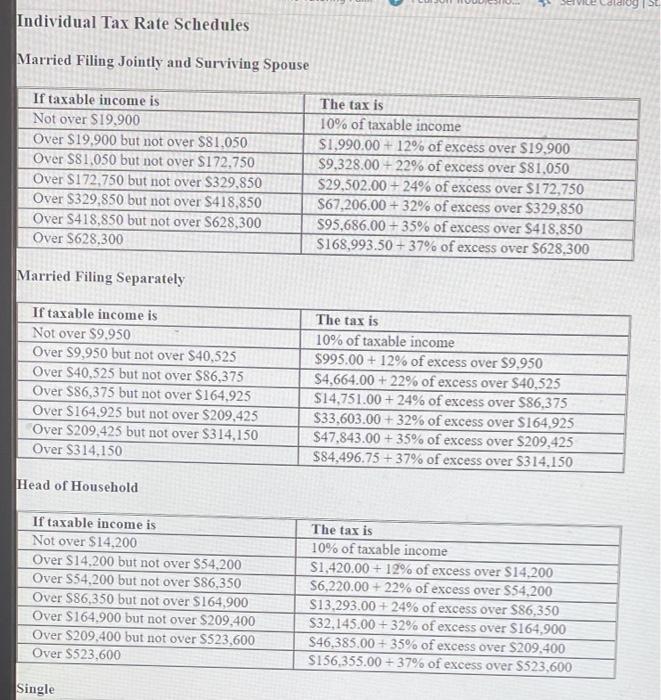

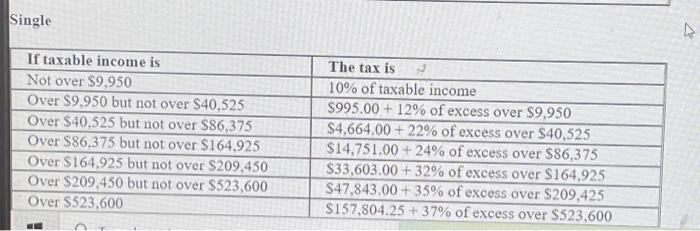

Ms. Ellis, a single individual, has $115,000 taxable income Assume the taxable year is 2021. Compute her income tax assuming that: Use Individual Tax Rate Schedules Required: a. Taxable income includes no capital gain b. Taxable income includes $22,000 capital gain eligible for the 15 percent preferential rate, (For all requirements, round your intermediate calculations and final answers to the nearest whole dollar amount.) Answer is complete but not entirely correct. Case Income tax la Includes no capital gain $ 21.680 b Includes capital gain 19,700 Individual Tax Rate Schedules Married Filing Jointly and Surviving Spouse If taxable income is Not over $19,900 Over $19.900 but not over $81,050 Over $81,050 but not over $172.750 Over $172.750 but not over $329,850 Over $329,850 but not over $418,850 Over S418,850 but not over S628,300 Over $628,300 The tax is 10% of taxable income $1.990.00 +12% of excess over $19,900 $9,328.00 +22% of excess over $81,050 $29,502.00 +24% of excess over $172,750 $67,206.00 +32% of excess over $329,850 595,686,00 + 35% of excess over $418,850 $168.993.50 +37% of excess over $628,300 Married Filing Separately If taxable income is Not over $9.950 Over $9,950 but not over $40,525 Over $40,525 but not over $86,375 Over $86,375 but not over $164.925 Over $164.925 but not over $209,425 Over $209,425 but not over $314,150 Over $314,150 The tax is 10% of taxable income $995.00 + 12% of excess over $9.950 $4,664.00 +22% of excess over $40,525 $14,751.00 +24% of excess over $86,375 $33,603.00 + 32% of excess over $164.925 $47,843.00 + 35% of excess over $209,425 $84,496.75 +37% of excess over $314.150 Head of Household If taxable income is Not over $14,200 Over $14,200 but not over $54,200 Over $54,200 but not over $86,350 Over $86,350 but not over $164.900 Over $164.900 but not over $209,400 Over $209,400 but not over S523,600 Over $523,600 The tax is 10% of taxable income $1,420.00+ 12% of excess over $14.200 56,220.00 + 22% of excess over S54,200 S13.293.00 + 24% of excess over $86,350 $32.145.00 + 32% of excess over $164,900 S46,385.00+ 35% of excess over $209.400 $156,355.00 +37% of excess over S523,600 Single Single If taxable income is Not over $9.950 Over $9.950 but not over $40,525 Over $40,525 but not over $86,375 Over $86,375 but not over $164.925 Over $164.925 but not over $209,450 Over $209,450 but not over S523,600 Over $523,600 The tax is 10% of taxable income $995.00 +12% of excess over $9.950 S4,664.00 +22% of excess over $40,525 $14,751.00 +24% of excess over $86,375 $33,603.00 + 32% of excess over $164.925 S47,843.00 + 35% of excess over $209,425 $157,804.25 +37% of excess over $523,600