Answered step by step

Verified Expert Solution

Question

1 Approved Answer

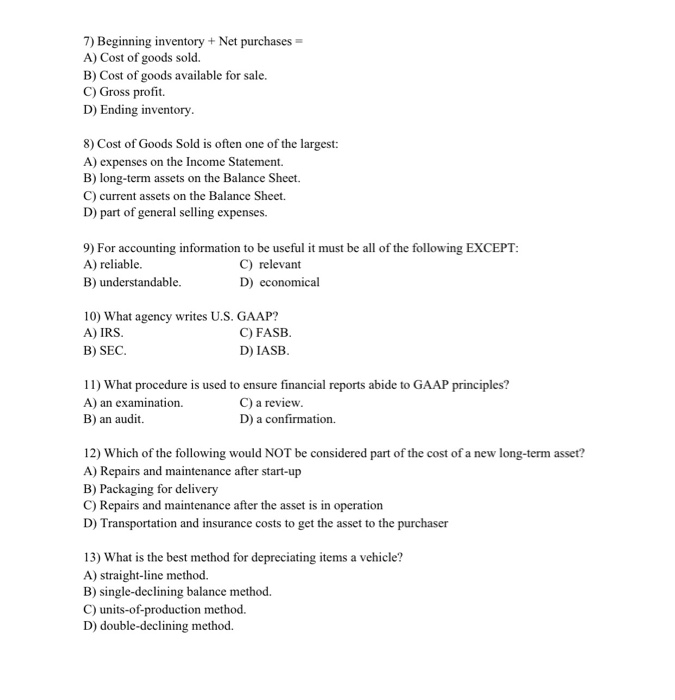

Multiple Choice 7) Beginning inventory + Net purchases = A) Cost of goods sold. B) Cost of goods available for sale. C) Gross profit. D)

Multiple Choice

7) Beginning inventory + Net purchases = A) Cost of goods sold. B) Cost of goods available for sale. C) Gross profit. D) Ending inventory. 8) Cost of Goods Sold is often one of the largest: A) expenses on the Income Statement. B) long-term assets on the Balance Sheet C) current assets on the Balance Sheet. D) part of general selling expenses. 9) For accounting information to be useful it must be all of the following EXCEPT: A) reliable. C) relevant B) understandable. D) economical 10) What agency writes U.S. GAAP? A) IRS C) FASB. B) SEC. D) IASB. 11) What procedure is used to ensure financial reports abide to GAAP principles? A) an examination. C) a review. B) an audit. D) a confirmation. 12) Which of the following would NOT be considered part of the cost of a new long-term asset? A) Repairs and maintenance after start-up B) Packaging for delivery C) Repairs and maintenance after the asset is in operation D) Transportation and insurance costs to get the asset to the purchaser 13) What is the best method for depreciating items a vehicle? A) straight-line method. B) single-declining balance method. C) units-of-production method. D) double-declining method Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

FINANCIAL ACCOUNTING AND COSTING

Authors: Meera Gopi Krishna

1st Edition

979-8604687369