Answered step by step

Verified Expert Solution

Question

1 Approved Answer

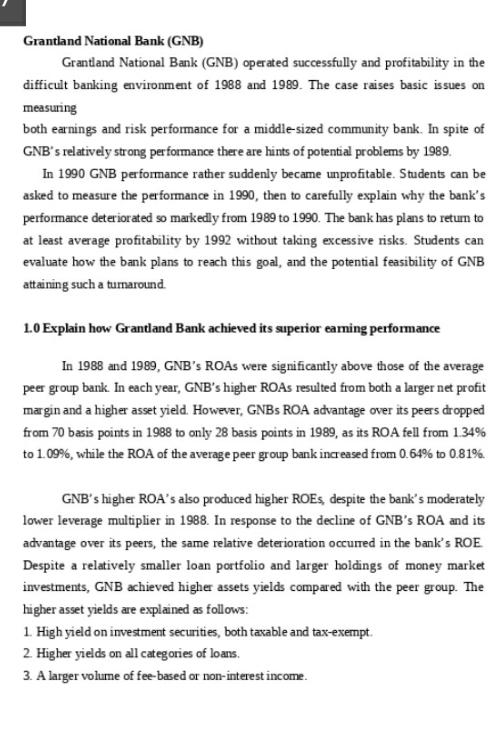

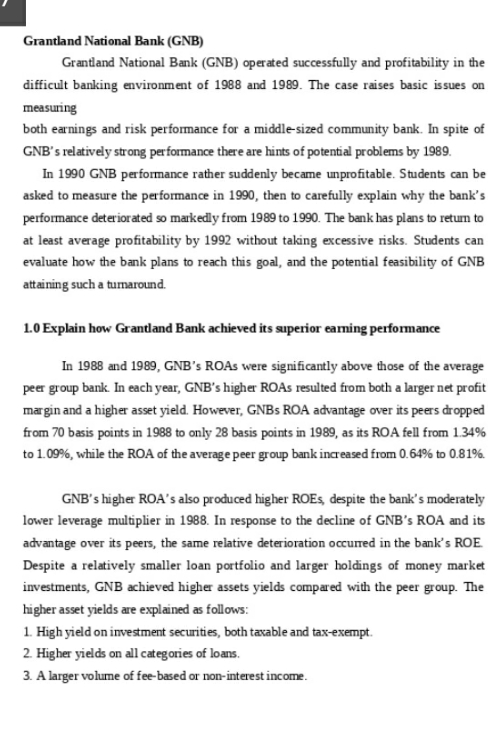

my case study Grantland National Bank (GNB) Grantland National Bank (GNB) operated successfully and profitability in the difficult banking environment of 1988 and 1989. The

my case study

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Legitimacy Of Family Rights In Strasbourg Case Law Living Instrument Or Extinguished Sovereignty?

Authors: Carmen Draghici

1st Edition

150992891X, 978-1509928910