Answered step by step

Verified Expert Solution

Question

1 Approved Answer

MY NOTES ASK YOUR TEACHER PRACTICE ANOTHER 2. [2/11 Points] DETAILS PREVIOUS ANSWERS You want to buy a house that has a purchase price

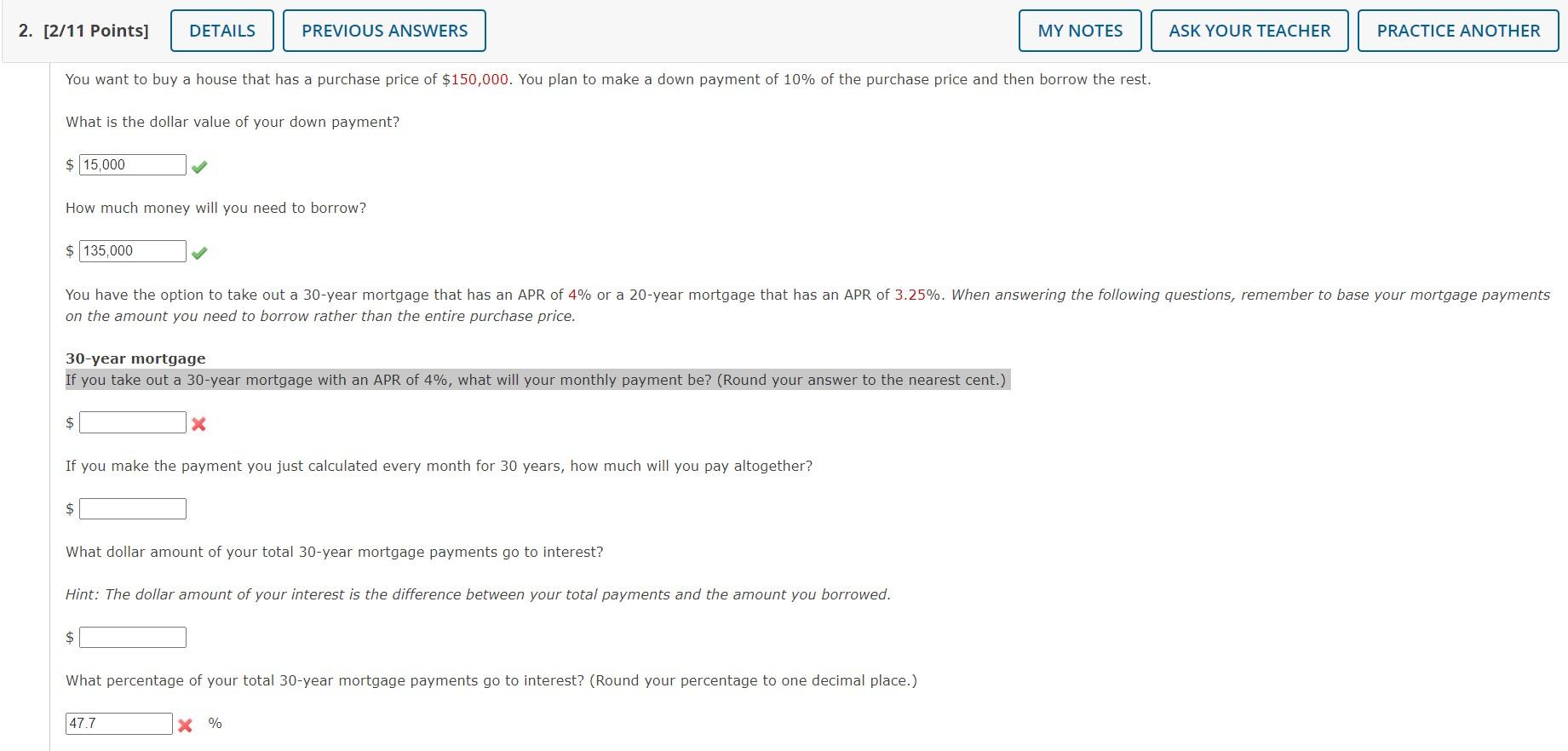

MY NOTES ASK YOUR TEACHER PRACTICE ANOTHER 2. [2/11 Points] DETAILS PREVIOUS ANSWERS You want to buy a house that has a purchase price of $150,000. You plan to make a down payment of 10% of the purchase price and then borrow the rest. What is the dollar value of your down payment? $ 15,000 How much money will you need to borrow? $ 135,000 You have the option to take out a 30-year mortgage that has an APR of 4% or a 20-year mortgage that has an APR of 3.25%. When answering the following questions, remember to base your mortgage payments on the amount you need to borrow rather than the entire purchase price. 30-year mortgage If you take out a 30-year mortgage with an APR of 4%, what will your monthly payment be? (Round your answer to the nearest cent.) $ If you make the payment you just calculated every month for 30 years, how much will you pay altogether? $ What dollar amount of your total 30-year mortgage payments go to interest? Hint: The dollar amount of your interest is the difference between your total payments and the amount you borrowed. $ What percentage of your total 30-year mortgage payments go to interest? (Round your percentage to one decimal place.) 47.7 %

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction to Finance Markets Investments and Financial Management

Authors: Melicher Ronald, Norton Edgar

15th edition

9781118800720, 1118492676, 1118800729, 978-1118492673