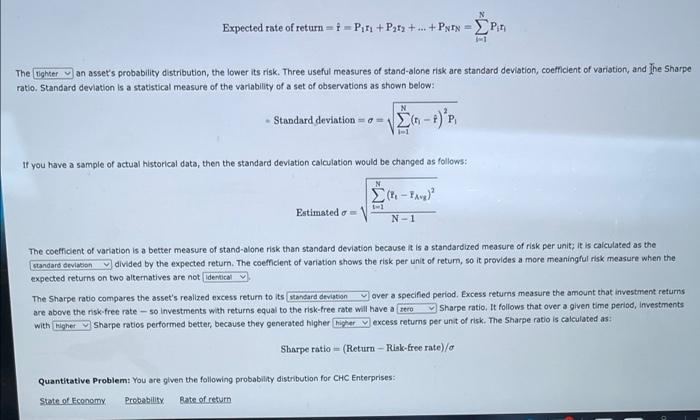

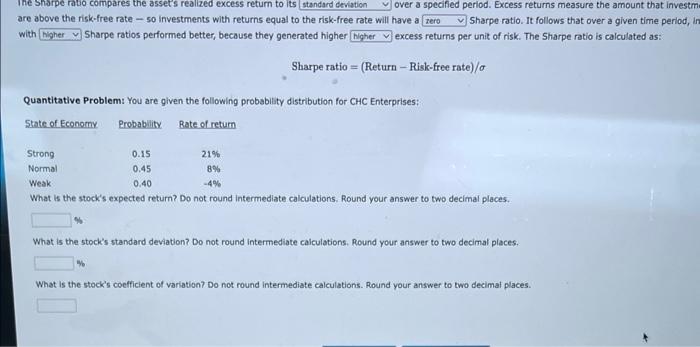

N Expected rate of return = + Piti + P212 + ... + Pyry - Pin - PA The lighter van asset's probability distribution, the lower its risk. Three useful measures of stand-alone risk are standard deviation, coefficient of variation, and The Sharpe ratio. Standard deviation is a statistical measure of the variability of a set of observations as shown below: N - Standard deviation = 0 - 3 (n-) p If you have a sample of actual historical data, then the standard deviation calculation would be changed as follows: N Estimated o N-1 The coefficient of variation is a better measure of stand-alone risk than standard deviation because it is a standardized measure of risk per unit, it is calculated as the standard deviations divided by the expected return. The coefficient of variation shows the risk per unit of retum, so it provides a more meaningful risk measure when the expected returns on two alternatives are not identical The Sharpe ratio compares the asset's realized excess return to its standard deviation over a specified period. Excess returns measure the amount that investment returns are above the risk-free rate - so Investments with returns equal to the risk-free rate will have a zero Sharpe ratio. It follows that over a given time period, Investments with higher Sharpe ratios performed better, because they generated Higher Higher excess returns per unit of risk. The Sharpe ratio is calculated as: Sharpe ratio - (Return - Rink-free rate) Quantitative Problem: You are given the following probability distribution for CHC Enterprises: State of Economy Probability Bate of return The Sharpe ratio compares the asset's realized excess return to its standard deviation over a specified period. Excess returns measure the amount that investm are above the risk-free rate - so investments with returns equal to the risk-free rate will have a rero Sharpe ratio. It follows that over a given time period, in with higher Sharpe ratios performed better, because they generated higher higher excess returns per unit of risk. The Sharpe ratio is calculated as: Sharpe ratio = (Return - Risk-free rate)/ Quantitative Problem: You are given the following probability distribution for CHC Enterprises: State of Economy Probability Bate of return Strong 0.15 21% Normal 0.45 8% Weak 0.40 -4% What is the stock's expected return? Do not round intermediate calculations. Round your answer to two decimal places. What is the stock's standard deviation? Do not round Intermediate calculations. Round your answer to two decimal places. What is the stock's coefficient of variation? Do not round intermediate calculations. Round your answer to two decimat places