Answered step by step

Verified Expert Solution

Question

1 Approved Answer

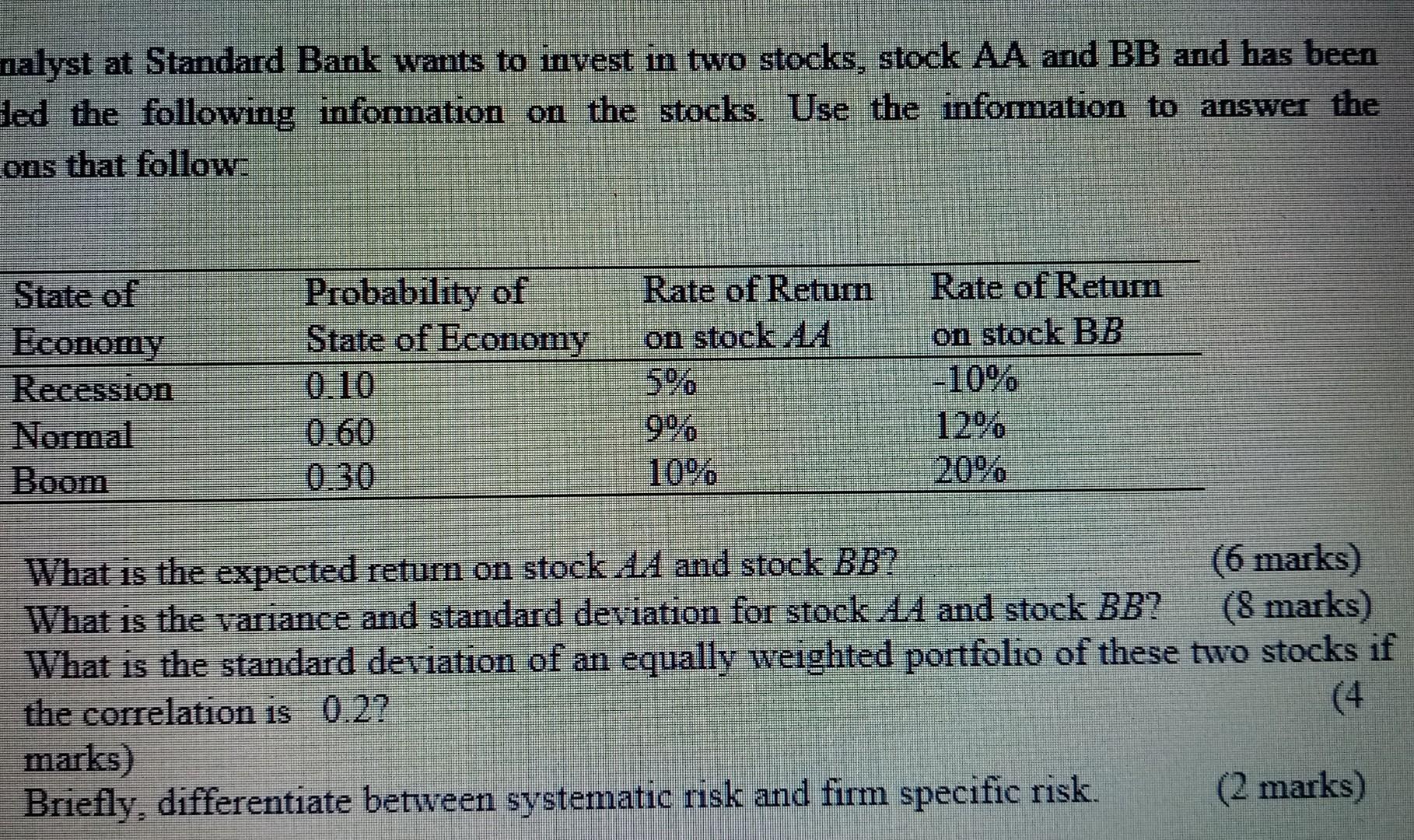

nalyst at Standard Bank wants to invest in two stocks, stock AA and BB and has been ded the following information on the stocks. Use

nalyst at Standard Bank wants to invest in two stocks, stock AA and BB and has been ded the following information on the stocks. Use the information to answer the ons that follow Rate of Retum on stock 4A State of Economy Recession Normal Boom Probability of State of Economy 0.10 0.60 0 30 Rate of Retum on stock BB -10% 100% What is the expected retum on stock 4A and stock BB? (6 marks) What is the variance and standard deviation for stock AA and stock BB? (8 marks) What is the standard deviation of an equally weighted portfolio of these two stocks if the correlation is 0.2? (4 marks) Briefly, differentiate between systematic risk and firm specific risk. (2 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Primary Science Audit And Test

Authors: Jenny Byrne, Andri Christodoulou, John Sharp

4th Edition

1446282732, 978-1446282731