Answered step by step

Verified Expert Solution

Question

1 Approved Answer

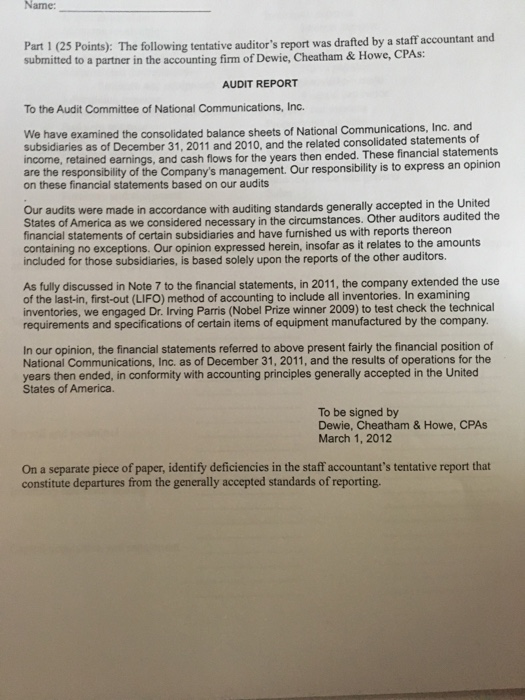

Name: Part 1 (25 submitted to a partner in the accounting firm o Points): The following tentative auditor's report was drafted by a staff accountant

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bio Technology Audit In Hungary Guidelines Implementation Results

Authors: Ulrike Bross, Annamaria Inzelt, Thomas Reiß

1st Edition

3790810924, 978-3790810929