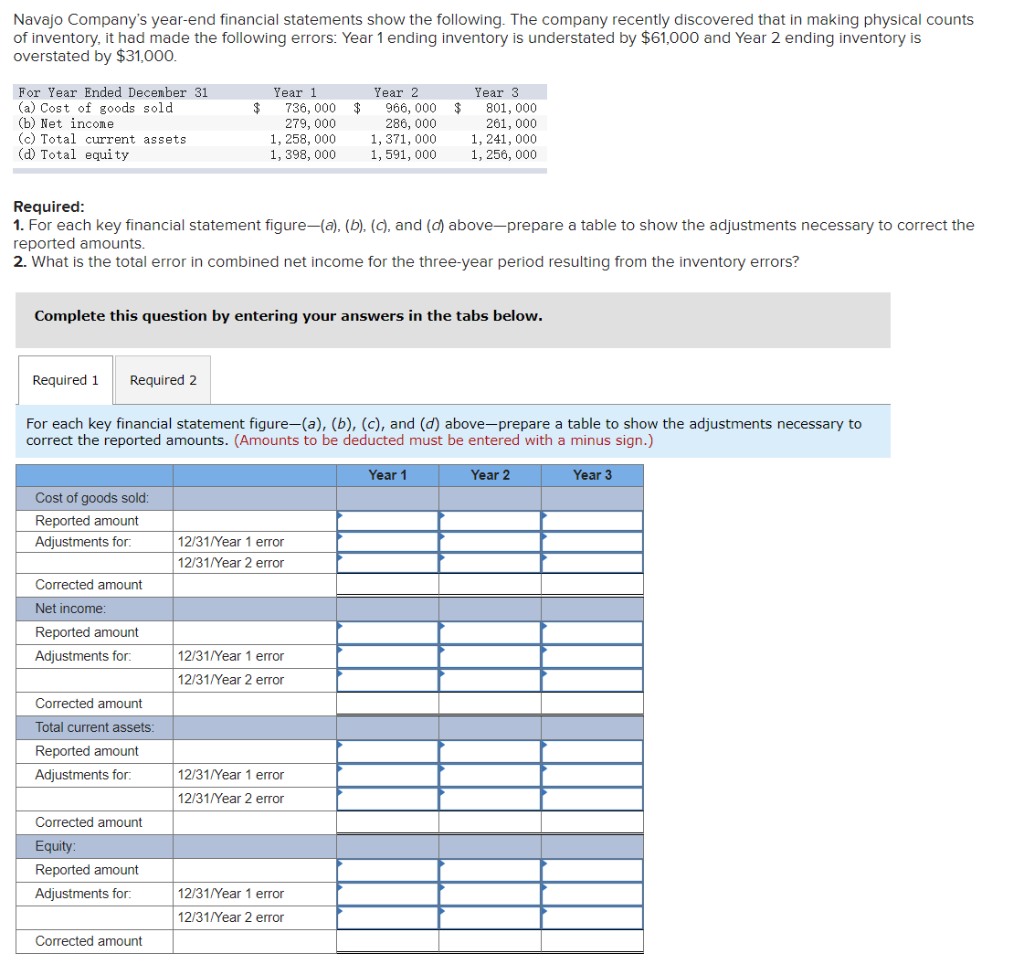

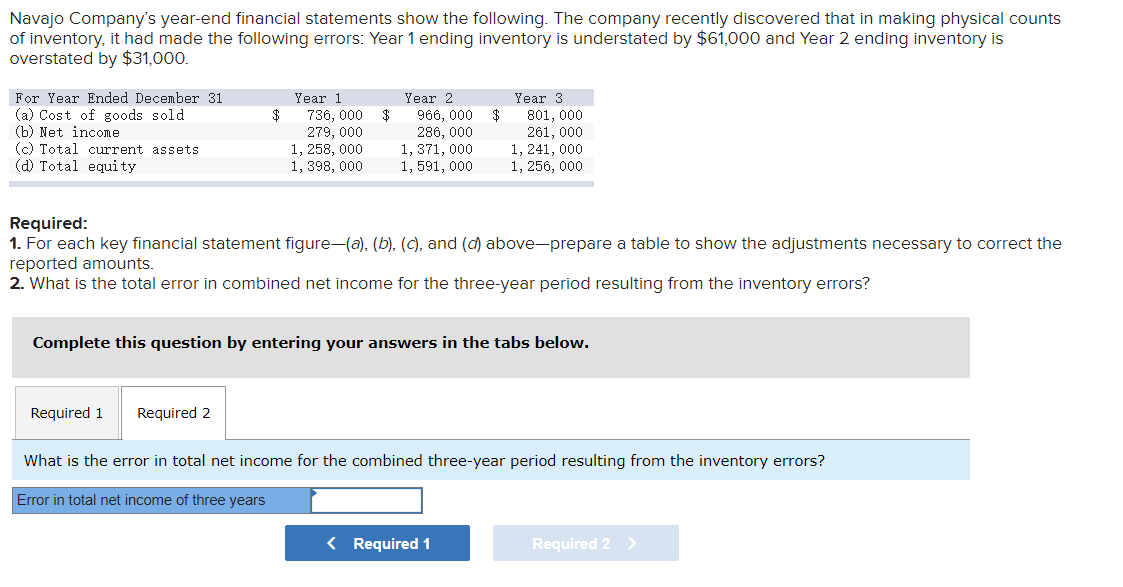

Navajo Company's year-end financial statements show the following. The company recently discovered that in making physical counts of inventory, it had made the following errors: Year 1 ending inventory is understated by $61,000 and Year 2 ending inventory is overstated by $31.000. $ $ For Year Ended December 31 (a) Cost of goods sold (b) Net income (c) Total current assets (d) Total equity Year 1 736, 000 $ 279,000 1,258,000 1, 398,000 Year 2 966,000 286,000 1, 371, 000 1,591, 000 Year 3 801, 000 261, 000 1, 241,000 1,256,000 Required: 1. For each key financial statement figure-(a), (b), (c), and (d) above-prepare a table to show the adjustments necessary to correct the reported amounts. 2. What is the total error in combined net income for the three-year period resulting from the inventory errors? Complete this question by entering your answers in the tabs below. Required 1 Required 2 For each key financial statement figure-(a), (b), (c), and (d) above-prepare a table to show the adjustments necessary to correct the reported amounts. (Amounts to be deducted must be entered with a minus sign.) Year 1 Year 2 Year 3 Cost of goods sold: Reported amount Adjustments for 12/31/Year 1 error 12/31/Year 2 error Corrected amount Net income: Reported amount Adjustments for: 12/31/Year 1 error 12/31/Year 2 error Corrected amount Total current assets: Reported amount Adjustments for 12/31/Year 1 error 12/31/Year 2 error Corrected amount Equity Reported amount Adjustments for 12/31/Year 1 error 12/31/Year 2 error Corrected amount Navajo Company's year-end financial statements show the following. The company recently discovered that in making physical counts of inventory, it had made the following errors: Year 1 ending inventory is understated by $61,000 and Year 2 ending inventory is overstated by $31,000. $ $ For Year Ended December 31 (a) Cost of goods sold (b) Net income (c) Total current assets (d) Total equity Year 1 736, 000 $ 279,000 1, 258,000 1, 398,000 Year 2 966, 000 286,000 1, 371,000 1, 591,000 Year 3 801, 000 261,000 1, 241,000 1, 256, 000 Required: 1. For each key financial statement figure-(a), (b), (c), and (d) above-prepare a table to show the adjustments necessary to correct the reported amounts. 2. What is the total error in combined net income for the three-year period resulting from the inventory errors? Complete this question by entering your answers in the tabs below. Required 1 Required 2 What is the error in total net income for the combined three-year period resulting from the inventory errors? Error in total net income of three years