Answered step by step

Verified Expert Solution

Question

1 Approved Answer

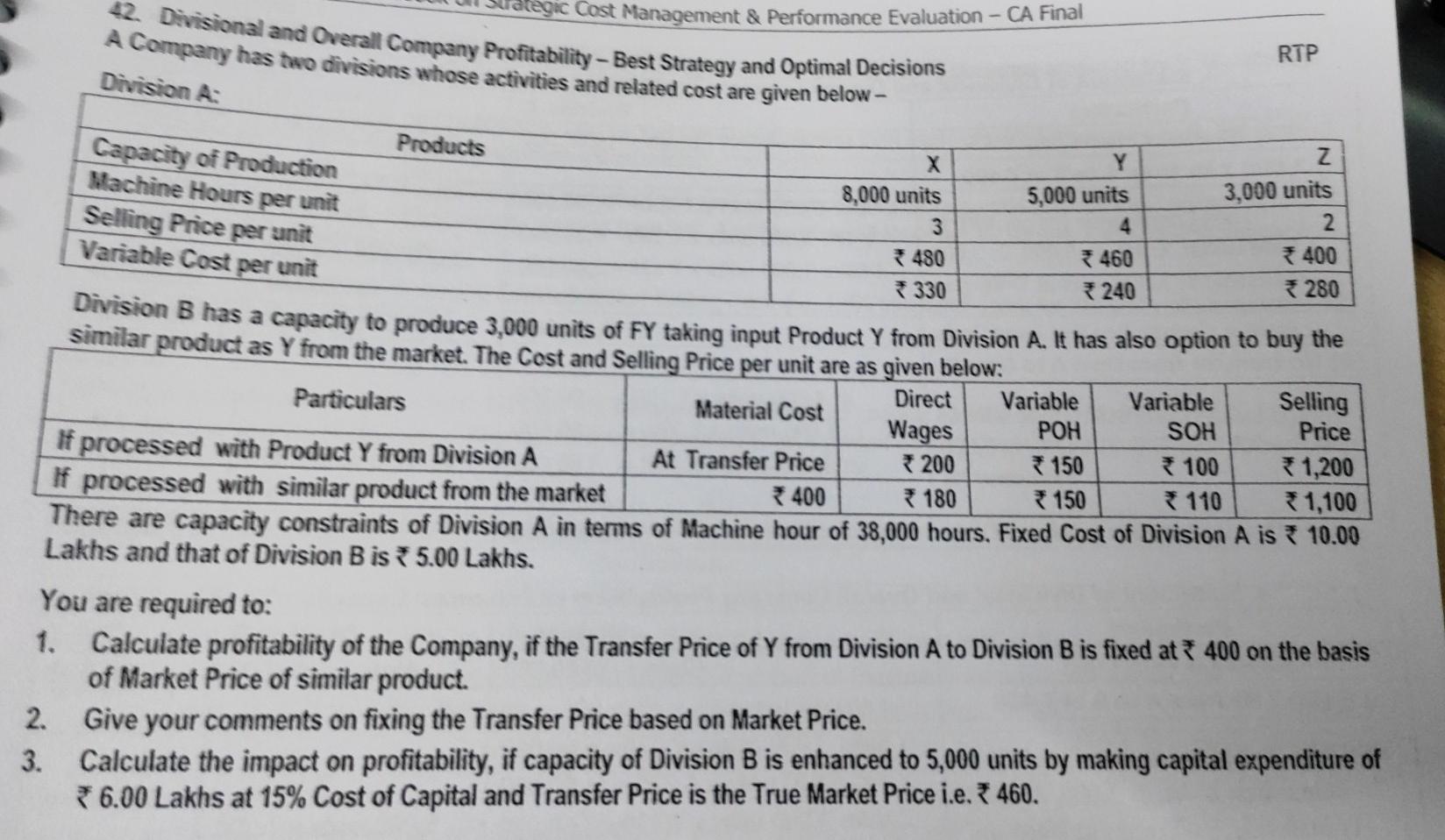

need all otherwise downvoted ategic Cost Management & Performance Evaluation - CA Final RTP 42. Divisional and Overall Company Profitability - Best Strategy and Optimal

need all otherwise downvoted

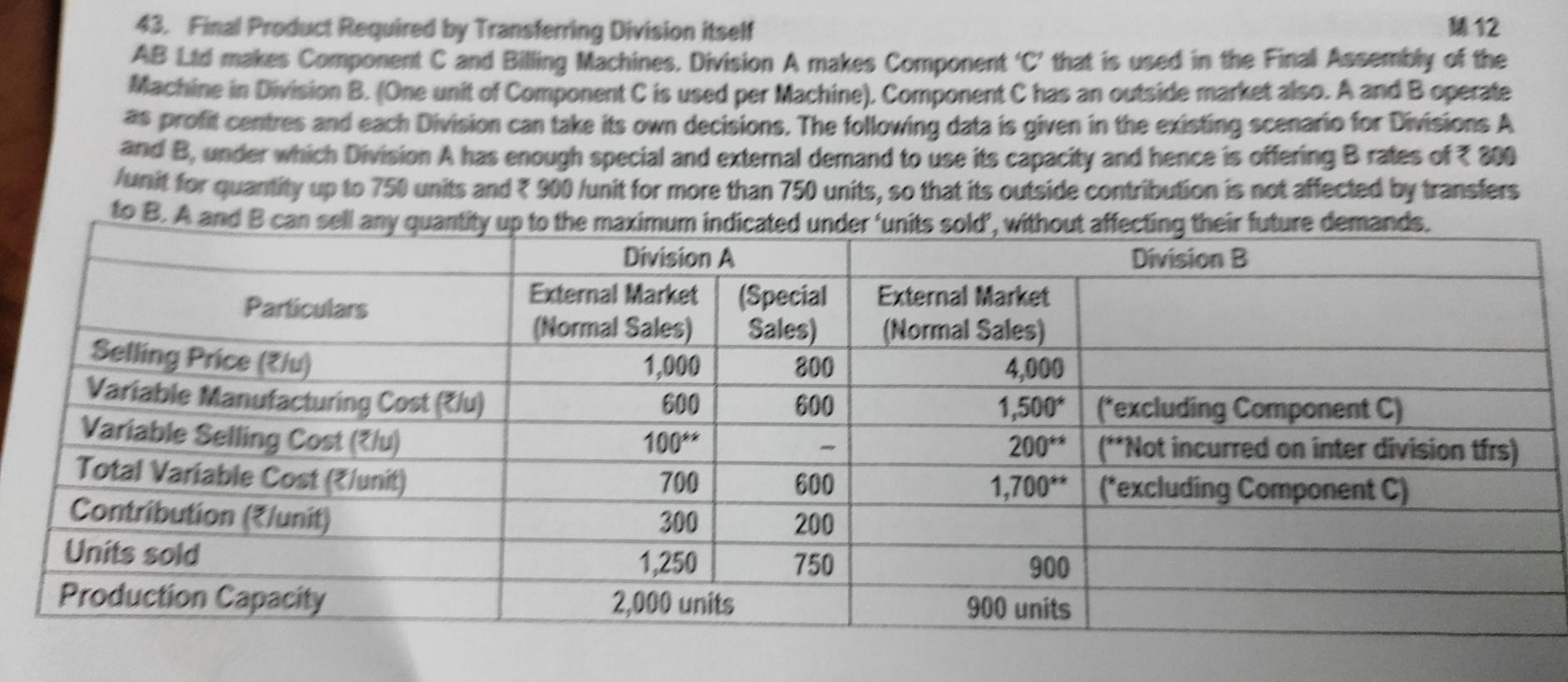

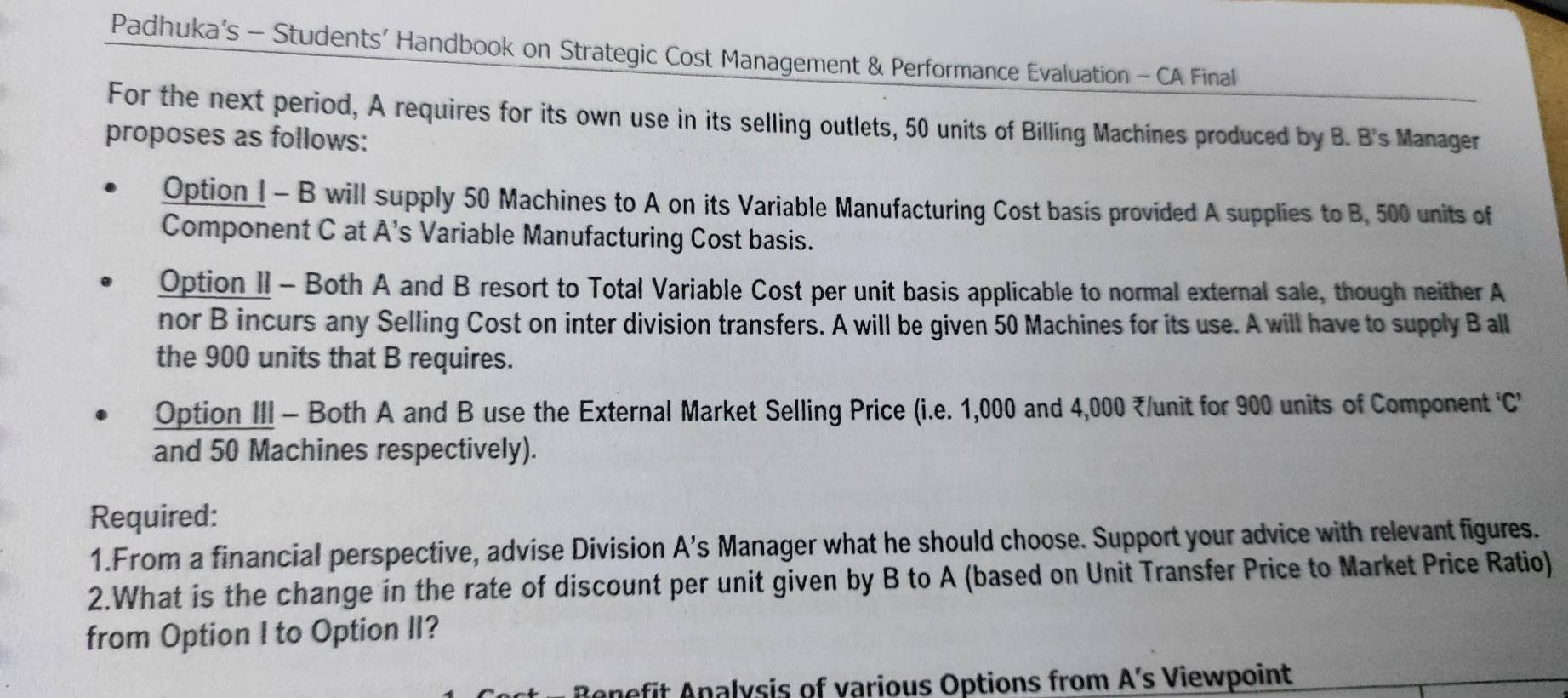

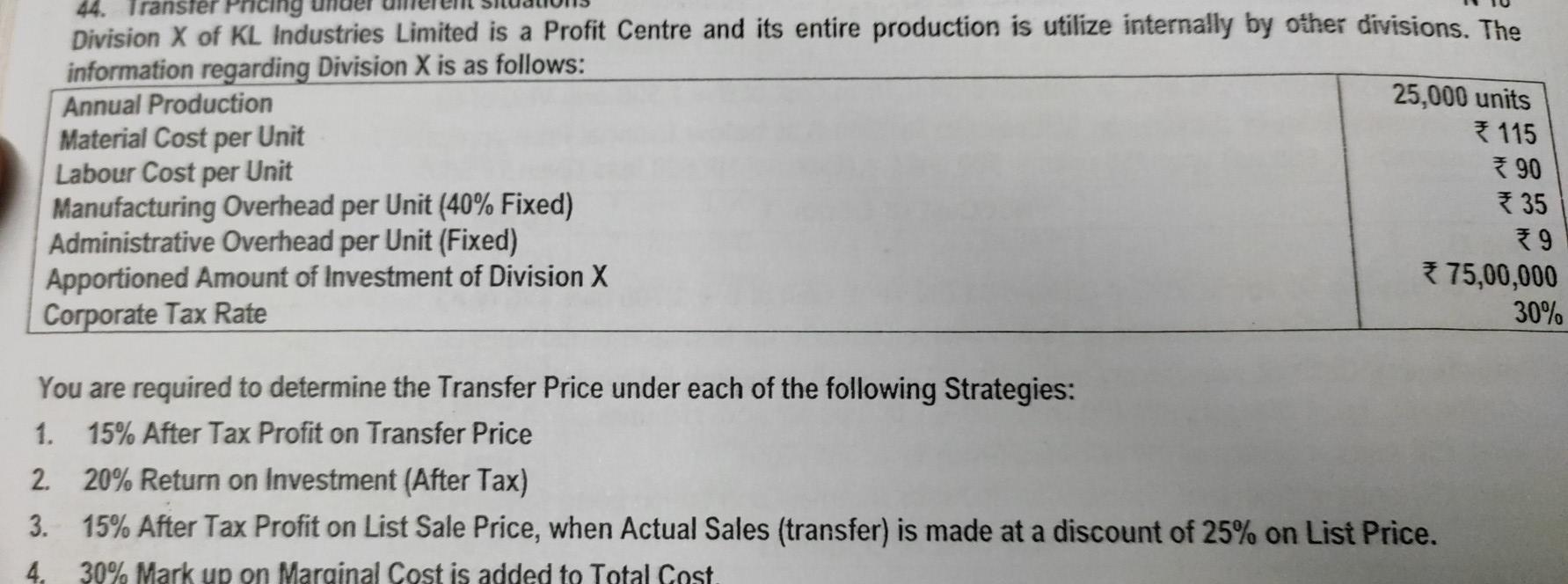

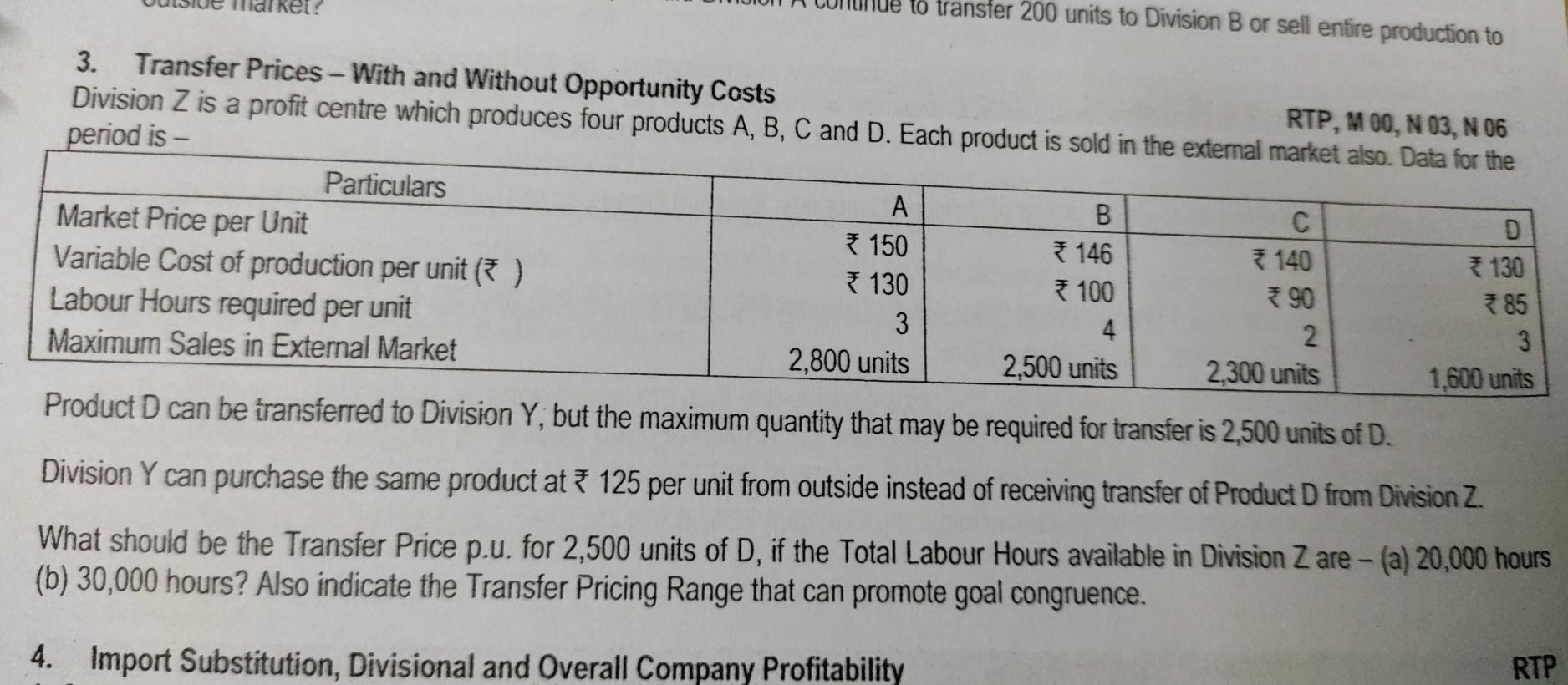

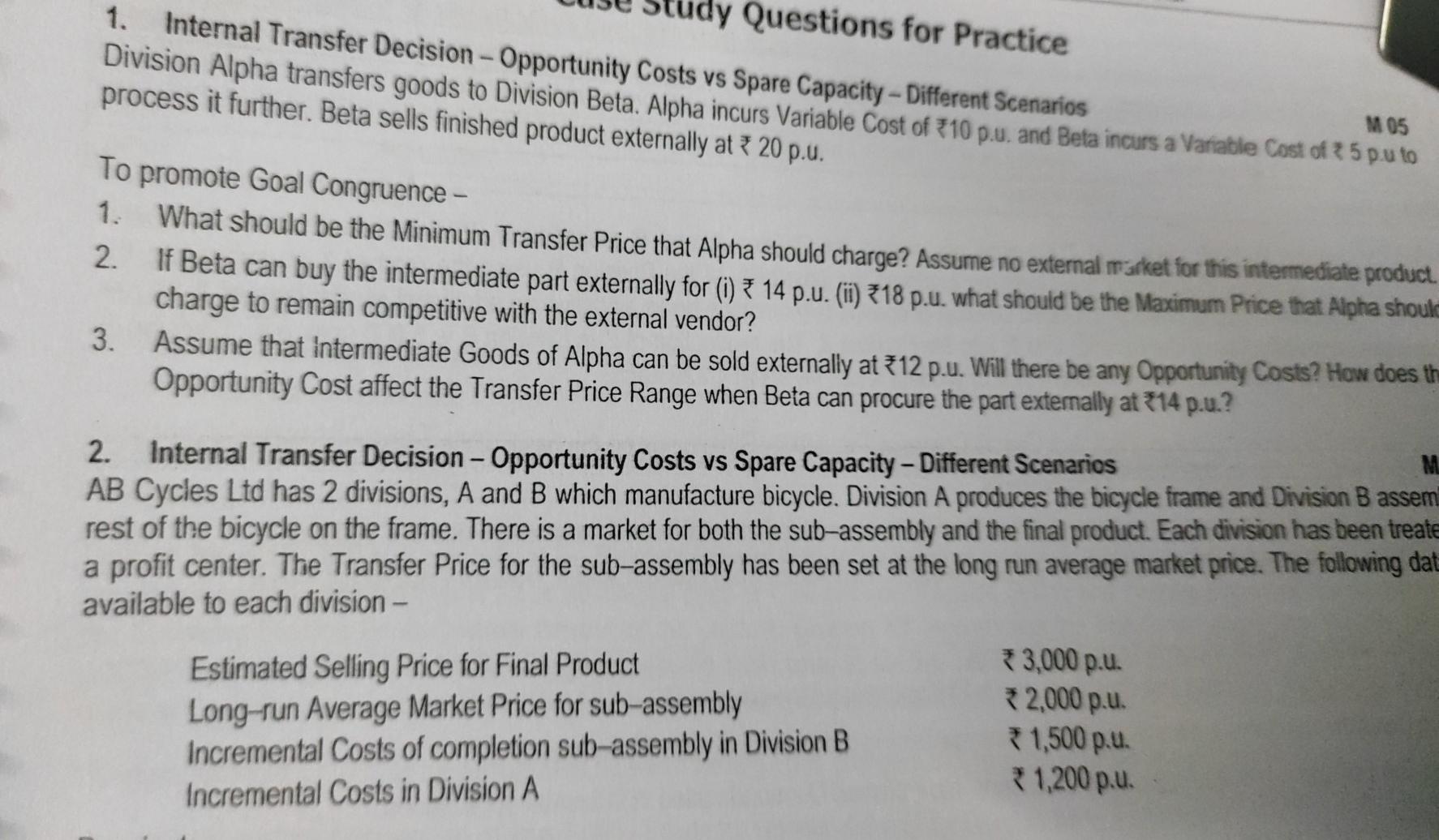

ategic Cost Management & Performance Evaluation - CA Final RTP 42. Divisional and Overall Company Profitability - Best Strategy and Optimal Decisions A Company has dvo divisions whose activities and related cost are given below- Division A: Products Capacity of Production Machine Hours per unit Selling Price per unit Variable Cost per unit Z 8,000 units 5,000 units 3,000 units 3 4 2. 480 3460 400 * 330 240 280 Division B has a capacity to produce 3,000 units of FY taking input Product Y from Division A. It has also option to buy the similar product as Y from the market. The Cost and Selling Price per unit are as given below: Particulars Material Cost Direct Variable Variable Selling Wages POH SOH Price If processed with Product Y from Division A At Transfer Price * 200 * 150 *100 1,200 If processed with similar product from the market * 400 * 180 * 150 110 1,100 There are capacity constraints of Division A in terms of Machine hour of 38,000 hours. Fixed Cost of Division A is * 10.00 Lakhs and that of Division B is * 5.00 Lakhs. You are required to: 1. Calculate profitability of the Company, if the Transfer Price of Y from Division A to Division B is fixed at * 400 on the basis of Market Price of similar product. 2. Give your comments on fixing the Transfer Price based on Market Price. 3. Calculate the impact on profitability, if capacity of Division B is enhanced to 5,000 units by making capital expenditure of 6.00 Lakhs at 15% Cost of Capital and Transfer Price is the True Market Price i.e. *460. 11 12 43. Final Product Required by Transferring Division itself AB Lid makes Component C and Billing Machines. Division A makes Component that is ved in the Find Assembly di the Machine in Deinion B. (One unit of Component C is used per Machine). Component Chas an outside matriek diso. A and Beste as profit centres and each Division can take its own decisions. The following data is given in the easting scenario for Drsions A and B, under which Division A has enough special and external demand to use its capacity and hence is offering Brates of 800 lunit for quantity up to 750 units and 2 900 lunit for more than 750 units, so that its outside contribution is not affected by transfers to B. A and B can sell any quantity up to the maximum indicated under 'units sold, without affecting their future demands. Division A Division B External Market (Special External Market Particulars (Normal Sales) Sales) (Normal Sales) Selling Price (lu) 1,000 800 4,000 Variable Manufacturing Cost elu) 600 600 1,500" ("excluding Component C) Variable Selling Cost (elu) 100" 200" ("Not incurred on inter division tfrs) Total Variable Cost (lunit) 700 600 1,700" ("excluding Component C) Contribution (lunit) 300 200 Units sold 1,250 750 900 Production Capacity 2,000 units 900 units Padhuka's - Students' Handbook on Strategic Cost Management & Performance Evaluation - CA Final . For the next period, A requires for its own use in its selling outlets, 50 units of Billing Machines produced by B. B's Manager proposes as follows: Option I-B will supply 50 Machines to A on its Variable Manufacturing Cost basis provided A supplies to B, 500 units of Component C at A's Variable Manufacturing Cost basis. Option II - Both A and B resort to Total Variable Cost per unit basis applicable to normal external sale, though neither A nor B incurs any Selling Cost on inter division transfers. A will be given 50 Machines for its use. A will have to supply Ball the 900 units that B requires. Option III - Both A and B use the External Market Selling Price (i.e. 1,000 and 4,000 Klunit for 900 units of Component 'C' and 50 Machines respectively). e Required: 1.From a financial perspective, advise Division A's Manager what he should choose. Support your advice with relevant figures. 2.What is the change in the rate of discount per unit given by B to A (based on Unit Transfer Price to Market Price Ratio) from Option I to Option ll? 1 Cact Renefit Analysis of various Options from A's Viewpoint 44. Transfer Pri Division X of KL Industries Limited is a Profit Centre and its entire production is utilize internally by other divisions. The information regarding Division X is as follows: 25,000 units Annual Production * 115 Material Cost per Unit 90 Labour Cost per Unit Manufacturing Overhead per Unit (40% Fixed) * 35 Administrative Overhead per Unit (Fixed) 9 75,00,000 Apportioned Amount of Investment of Division X 30% Corporate Tax Rate You are required to determine the Transfer Price under each of the following Strategies: 1. 15% After Tax Profit on Transfer Price 2. 20% Return on Investment (After Tax) 3. 15% After Tax Profit on List Sale Price, when Actual Sales (transfer) is made at a discount of 25% on List Price. 4. 30% Mark up on Marginal Cost is added to Total Cost to transfer 200 units to Division B or sell entire production to 3. Transfer Prices - With and Without Opportunity Costs Division Z is a profit centre which produces four products A, B, C and D. Each product is sold in the external market also. Data for the RTP, M 00, N 03, N 06 period is - Particulars A B C Market Price per Unit * 150 * 146 140 130 Variable Cost of production per unit ( ) 130 100 90 85 Labour Hours required per unit 3 4 2 3 Maximum Sales in External Market 2,800 units 2,500 units 2,300 units 1.600 units Product D can be transferred to Division Y, but the maximum quantity that may be required for transfer is 2,500 units of D. Division Y can purchase the same product at * 125 per unit from outside instead of receiving transfer of Product D from Division Z. What should be the Transfer Price p.u. for 2,500 units of D, if the Total Labour Hours available in Division Z are - (a) 20,000 hours (b) 30,000 hours? Also indicate the Transfer Pricing Range that can promote goal congruence. 4. Import Substitution, Divisional and Overall Company Profitability RTP idy Questions for Practice 1. Internal Transfer Decision - Opportunity Costs vs Spare Capacity - Different Scenarios M05 Division Alpha transfers goods to Division Beta. Alpha incurs Variable Cost of 310 p., and Beta incurs a Variable Cost of 25 pu to process it further. Beta sells finished product externally at 20 p.u. To promote Goal Congruence - 1. What should be the Minimum Transfer Price that Alpha should charge? Assume no external madket for this intermediate product 2. If Beta can buy the intermediate part externally for (i) 7 14 p.u. (ii) 318 p.u. what should be the Maximum Price that Alpha should charge to remain competitive with the external vendor? 3. Assume that intermediate Goods of Alpha can be sold externally at 312 p.u. Will there be any Opportunity Costs? How does the Opportunity Cost affect the Transfer Price Range when Beta can procure the part externally at 314 p.u.? 2. Internal Transfer Decision - Opportunity Costs vs Spare Capacity - Different Scenarios M AB Cycles Ltd has 2 divisions, A and B which manufacture bicycle. Division A produces the bicycle frame and Division B assem rest of the bicycle on the frame. There is a market for both the sub-assembly and the final product . Each division has been treate a profit center. The Transfer Price for the sub-assembly has been set at the long run average market price. The following dat available to each division - 3,000 p.u. Estimated Selling Price for Final Product R2,000 p.u. Long-run Average Market Price for sub-assembly 1,500 p.u. Incremental Costs of completion sub-assembly in Division B 1,200 p.u. Incremental Costs in Division AStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting Chapters 14-23

Authors: Charles T. Horngren, Walter T. Harrison Jr, M. Suzanne Oliver

8th Edition

0136073018, 978-0136073017