Answered step by step

Verified Expert Solution

Question

1 Approved Answer

need answer urgently Q2: An investor purchased a newly issued bond with a maturity of 10 years 200 days ago. The bond carries a coupon

need answer urgently

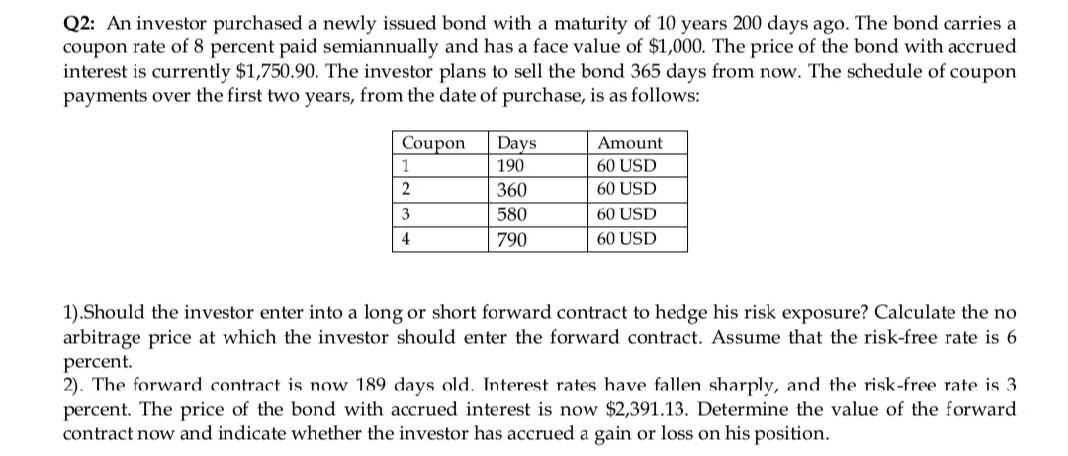

Q2: An investor purchased a newly issued bond with a maturity of 10 years 200 days ago. The bond carries a coupon rate of 8 percent paid semiannually and has a face value of $1,000. The price of the bond with accrued interest is currently $1,750.90. The investor plans to sell the bond 365 days from now. The schedule of coupon payments over the first two years, from the date of purchase, is as follows: Coupon 1 2 Days 190 360 580 790 Amount 60 USD 60 USD 60 USD 60 USD 3 4 1).Should the investor enter into a long or short forward contract to hedge his risk exposure? Calculate the no arbitrage price at which the investor should enter the forward contract. Assume that the risk-free rate is 6 percent. 2). The forward contract is now 189 days old. Interest rates have fallen sharply, and the risk-free rate is 3 percent. The price of the bond with accrued interest is now $2,391.13. Determine the value of the forward contract now and indicate whether the investor has accrued a gain or loss on his position. Q2: An investor purchased a newly issued bond with a maturity of 10 years 200 days ago. The bond carries a coupon rate of 8 percent paid semiannually and has a face value of $1,000. The price of the bond with accrued interest is currently $1,750.90. The investor plans to sell the bond 365 days from now. The schedule of coupon payments over the first two years, from the date of purchase, is as follows: Coupon 1 2 Days 190 360 580 790 Amount 60 USD 60 USD 60 USD 60 USD 3 4 1).Should the investor enter into a long or short forward contract to hedge his risk exposure? Calculate the no arbitrage price at which the investor should enter the forward contract. Assume that the risk-free rate is 6 percent. 2). The forward contract is now 189 days old. Interest rates have fallen sharply, and the risk-free rate is 3 percent. The price of the bond with accrued interest is now $2,391.13. Determine the value of the forward contract now and indicate whether the investor has accrued a gain or loss on his positionStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essential Personal Finance A Practical Guide For Students

Authors: Lien Luu, Jonquil Lowe, Jason Butler, Tony Byrne

1st Edition

1138692956, 978-1138692954