Answered step by step

Verified Expert Solution

Question

1 Approved Answer

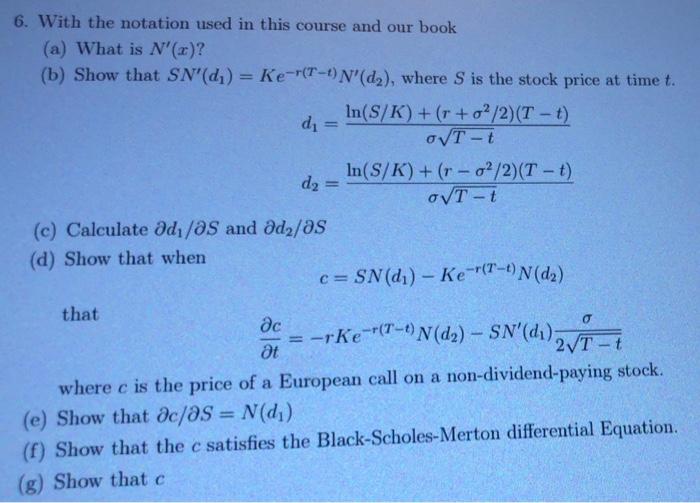

need (e)(f)(g), thanks 6. With the notation used in this course and our book (a) What is N'(x)? (b) Show that SN'(d) = Ke-(T-1)N'(d), where

need (e)(f)(g), thanks

6. With the notation used in this course and our book (a) What is N'(x)? (b) Show that SN'(d) = Ke-"(T-1)N'(d), where is the stock price at time t. In(S/K) + (r + 02/2)(T-t) di OVT-t In(S/K) + (r - 0/2)(T - t) d2 OVT-t (c) Calculate ad/as and ad2/as (d) Show that when c= SN(d) - Ke-r(T-1) (dz) that ac at 2VT where c is the price of a European call on a non-dividend-paying stock. (e) Show that dc/as = N(d) (f) Show that the c satisfies the Black-Scholes-Merton differential Equation. (g) Show that c =-rKe="{7-N(dz) SN'(di)vT - C c Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Before You Buy The Homebuyers Handbook For Todays Market

Authors: Michael Corbett, Jim Gillespie

1st Edition

0452296803, 978-0452296800