Answered step by step

Verified Expert Solution

Question

1 Approved Answer

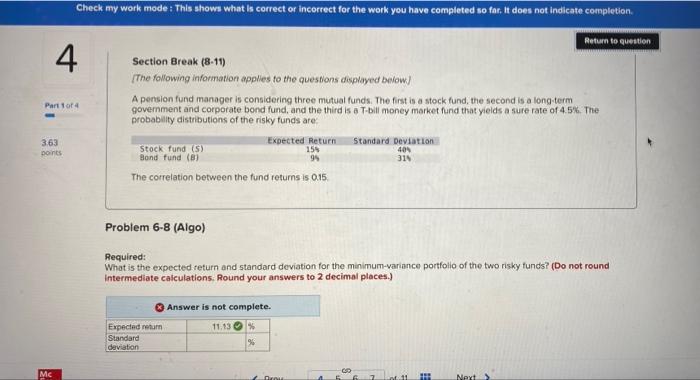

need help finding standard deviation Check my work mode: This shows what is correct or incorrect for the work you have completed so far. It

need help finding standard deviation

need help finding standard deviationStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Mein Ultimativer Weihnachts Planer

Authors: Zizo Nimane

1st Edition

B0CM2J8GTG