Answered step by step

Verified Expert Solution

Question

1 Approved Answer

need help from finance expert Current quotes on the US dollar (USD) to Euro (EU) are spot =$1.0400 and 3-month futures = $1.0300. The risk-free

need help from finance expert

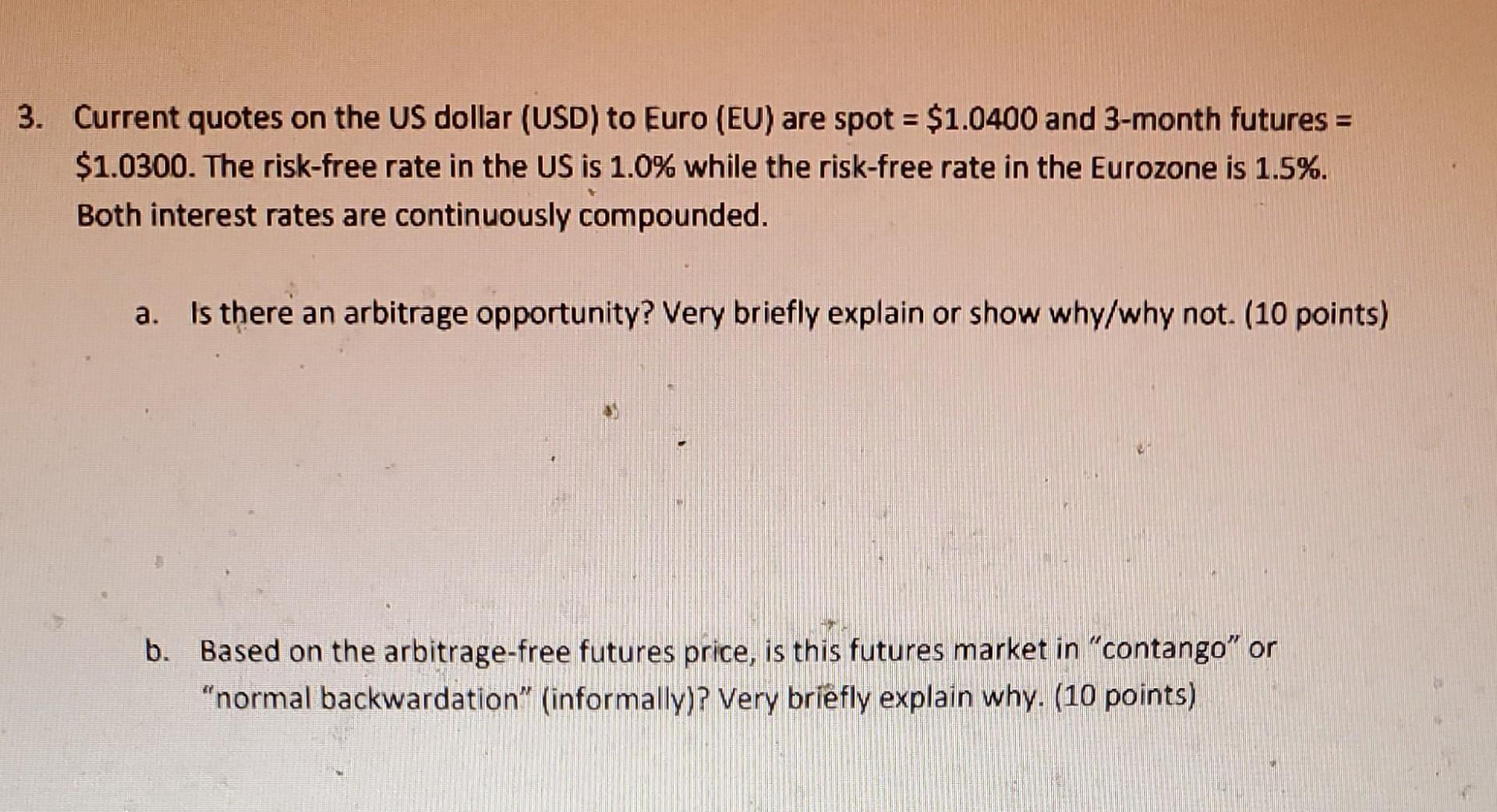

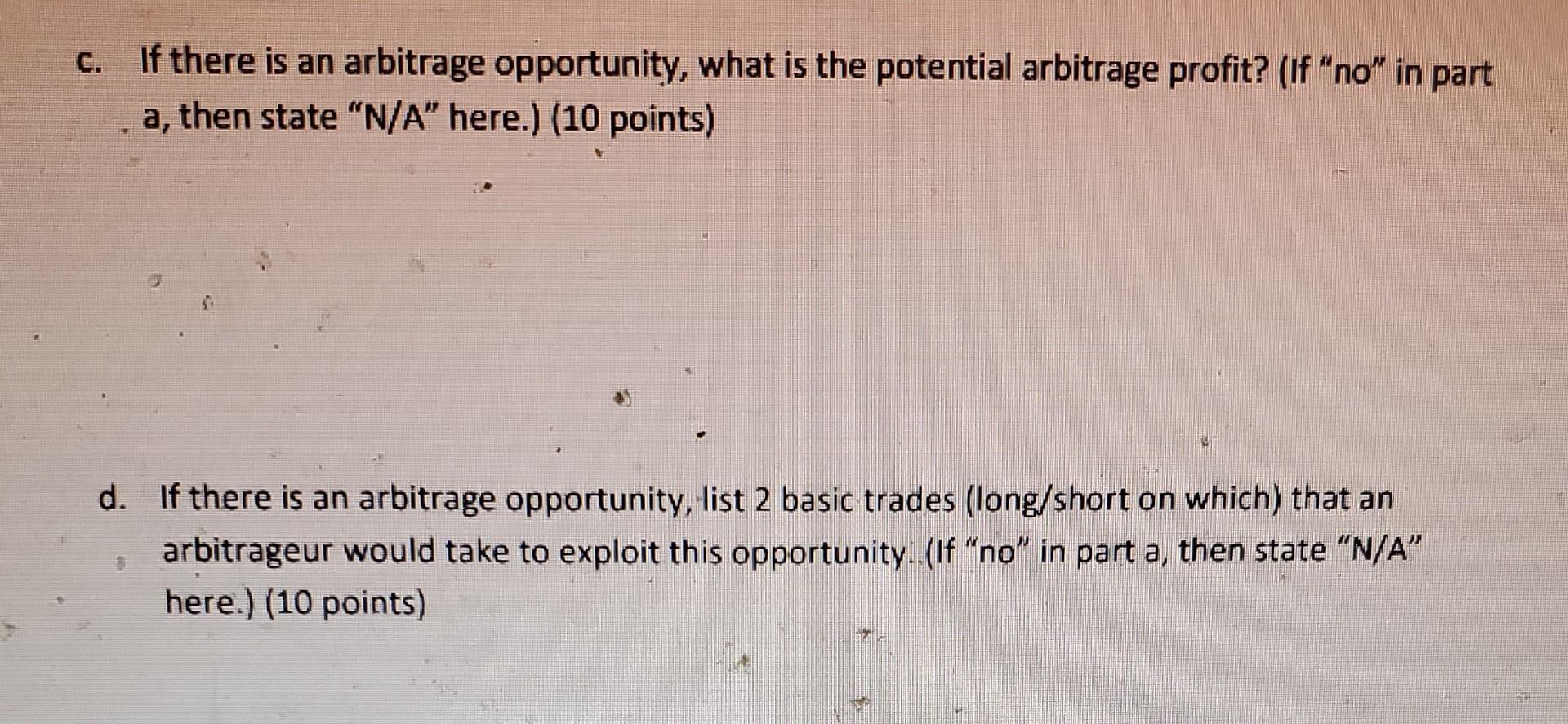

Current quotes on the US dollar (USD) to Euro (EU) are spot =$1.0400 and 3-month futures = $1.0300. The risk-free rate in the US is 1.0% while the risk-free rate in the Eurozone is 1.5%. Both interest rates are continuously compounded. a. Is there an arbitrage opportunity? Very briefly explain or show why/why not. (10 points) b. Based on the arbitrage-free futures price, is this futures market in "contango" or "normal backwardation" (informally)? Very briefly explain why. (10 points) c. If there is an arbitrage opportunity, what is the potential arbitrage profit? (If "no" in part a, then state "N/A" here.) (10 points) d. If there is an arbitrage opportunity, list 2 basic trades (long/short on which) that an arbitrageur would take to exploit this opportunity. (If "no" in part a, then state " N/A" " here.) (10 points) Current quotes on the US dollar (USD) to Euro (EU) are spot =$1.0400 and 3-month futures = $1.0300. The risk-free rate in the US is 1.0% while the risk-free rate in the Eurozone is 1.5%. Both interest rates are continuously compounded. a. Is there an arbitrage opportunity? Very briefly explain or show why/why not. (10 points) b. Based on the arbitrage-free futures price, is this futures market in "contango" or "normal backwardation" (informally)? Very briefly explain why. (10 points) c. If there is an arbitrage opportunity, what is the potential arbitrage profit? (If "no" in part a, then state "N/A" here.) (10 points) d. If there is an arbitrage opportunity, list 2 basic trades (long/short on which) that an arbitrageur would take to exploit this opportunity. (If "no" in part a, then state " N/A" " here.) (10 points)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Green And Sustainable Finance

Authors: Simon Thompson

2nd Edition

1398609242, 978-1398609242