Answered step by step

Verified Expert Solution

Question

1 Approved Answer

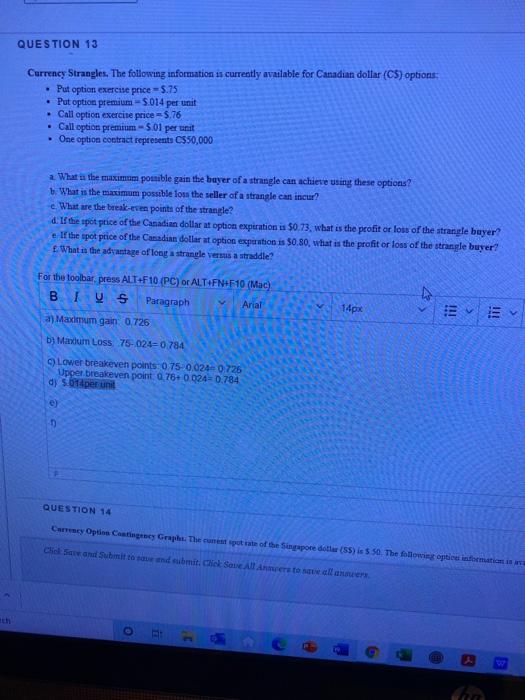

Need help on D, E, F please and thank you! QUESTION 13 Currency Strangles. The following information is currently available for Canadian dollar (CS) options

Need help on D, E, F please and thank you!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cryptocurrency And Bitcoin 101 Beginner S Guide To Becoming A Professional Trader And Investor In Digital Currency Without The Fear Of Liquidation Or Crash

Authors: Robert J Lewis

1st Edition

979-8826353905