Answered step by step

Verified Expert Solution

Question

1 Approved Answer

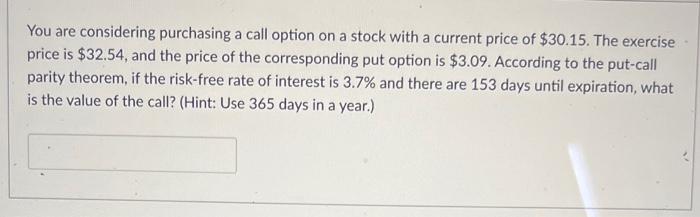

Need help on Hw, ill leave a like! (round to 4 dec. if possible) You are considering purchasing a call option on a stock with

Need help on Hw, ill leave a like! (round to 4 dec. if possible)

You are considering purchasing a call option on a stock with a current price of $30.15. The exercise price is $32.54, and the price of the corresponding put option is $3.09. According to the put-call parity theorem, if the risk-free rate of interest is 3.7% and there are 153 days until expiration, what is the value of the call? (Hint: Use 365 days in a year.) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Financial Management

Authors: James C. Van Horne

10th Edition

0138596875, 978-0138596873