need help with all please

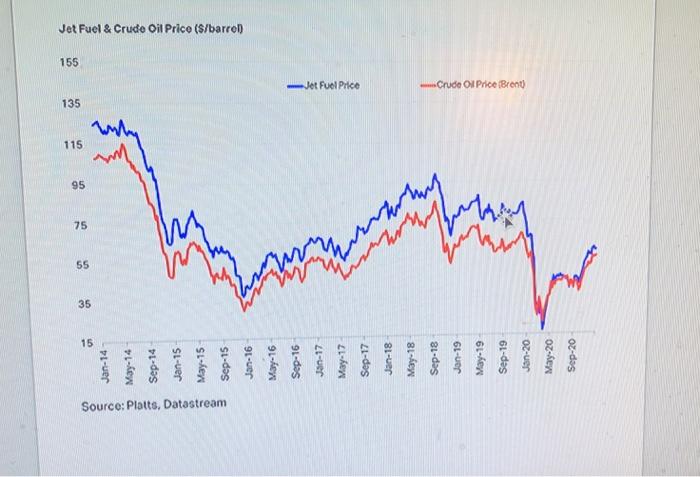

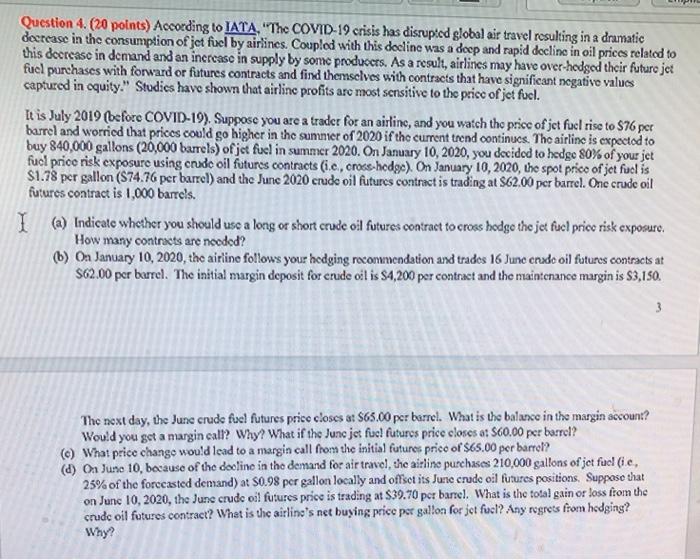

Question 4. (20 points) According to IATA. "The COVID-19 crisis has disrupted global air travel resulting in a dramatic decrease in the consumption of jet fuel by airlines. Coupled with this decline was a deep and rapid decline in oil prices related to this decrease in demand and an increase in supply by some producers. As a result, airlines may have over hedged their future jet fuel purchases with forward or futures contracts and find themselves with contracts that have significant negative values captured in cquity." Studies have shown that airline profits are most sensitive to the price of jet fuel. It is July 2019 (before COVID-19). Suppose you are a trader for an airline, and you watch the price of jet fuel rise to $76 per barrel and worried that prices could go higher in the summer of 2020 if the current trend continues. The airline is expected to buy 840,000 gallons (20,000 barrels) of jet fuel in summer 2020. On January 10, 2020, you decided to hedge 80% of your jet fuel price risk exposure using crude oil futures contracts (i.c,crocs-hedge). On January 10, 2020, the spot price of jet fuel is $1.78 per gallon (874.76 per barrel) and the June 2020 crude oil futurcs contract is trading at 862.00 per barrel. One crude oil futures contract is 1,000 barrels. I (a) Indicate whether you should use a long or short crude oil futures contract to cross bodge the jet fucl price risk exposure. How many contracts are needed? b) On January 10, 2020, the airine follows your hodging recommendation and trades 16 Junc crado oil futuros contracts at S62.00 per barrel. The initial margin deposit for crude oil is $4,200 per contract and the maintenance margin is 3,150 3 The next day, the June crude fuel futures prise closes at $65.00 pcr barrel. What is the balance in the margin account? Would you get a margin call? Why? What if the Junc jet fuel futuros price closes a: 560.00 per barrel? (@) What price chango would lead to a margin call from the initial futuros price of $65.00 per barrel? (d) On June 10, because of the decline in the demand for air travel the airline purchases 210,000 gallons of jet fuelle, 25% of the forceasted demand) at S0.98 per gallon locally and offset its June crude oil futures positions. Suppose that on June 10, 2020, the Junc crude oil futures price is trading at $39.70 per barrel. What is the total gain or loss from the crude oil futures contract? What is the airline's net buying price per gallon for jet fuel? Any regrets from hedging? Why? 135 115 155 95 75 15 Jan-14 um Source: Platts. Datastream Mary-14 Sep-14 Jet Fuel & Crude Oil Price (s/barrel Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17 -Jet Fuel Price May-17 Sep-17 un Jan-18 worthy marhus May-18 Sep-18 Jan-19 May-19 Crude Oil Price (Brent) Sep-19 Jan-20 May-20 Sep-20 Question 4. (20 points) According to IATA. "The COVID-19 crisis has disrupted global air travel resulting in a dramatic decrease in the consumption of jet fuel by airlines. Coupled with this decline was a deep and rapid decline in oil prices related to this decrease in demand and an increase in supply by some producers. As a result, airlines may have over hedged their future jet fuel purchases with forward or futures contracts and find themselves with contracts that have significant negative values captured in cquity." Studies have shown that airline profits are most sensitive to the price of jet fuel. It is July 2019 (before COVID-19). Suppose you are a trader for an airline, and you watch the price of jet fuel rise to $76 per barrel and worried that prices could go higher in the summer of 2020 if the current trend continues. The airline is expected to buy 840,000 gallons (20,000 barrels) of jet fuel in summer 2020. On January 10, 2020, you decided to hedge 80% of your jet fuel price risk exposure using crude oil futures contracts (i.c,crocs-hedge). On January 10, 2020, the spot price of jet fuel is $1.78 per gallon (874.76 per barrel) and the June 2020 crude oil futurcs contract is trading at 862.00 per barrel. One crude oil futures contract is 1,000 barrels. I (a) Indicate whether you should use a long or short crude oil futures contract to cross bodge the jet fucl price risk exposure. How many contracts are needed? b) On January 10, 2020, the airine follows your hodging recommendation and trades 16 Junc crado oil futuros contracts at S62.00 per barrel. The initial margin deposit for crude oil is $4,200 per contract and the maintenance margin is 3,150 3 The next day, the June crude fuel futures prise closes at $65.00 pcr barrel. What is the balance in the margin account? Would you get a margin call? Why? What if the Junc jet fuel futuros price closes a: 560.00 per barrel? (@) What price chango would lead to a margin call from the initial futuros price of $65.00 per barrel? (d) On June 10, because of the decline in the demand for air travel the airline purchases 210,000 gallons of jet fuelle, 25% of the forceasted demand) at S0.98 per gallon locally and offset its June crude oil futures positions. Suppose that on June 10, 2020, the Junc crude oil futures price is trading at $39.70 per barrel. What is the total gain or loss from the crude oil futures contract? What is the airline's net buying price per gallon for jet fuel? Any regrets from hedging? Why? 135 115 155 95 75 15 Jan-14 um Source: Platts. Datastream Mary-14 Sep-14 Jet Fuel & Crude Oil Price (s/barrel Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17 -Jet Fuel Price May-17 Sep-17 un Jan-18 worthy marhus May-18 Sep-18 Jan-19 May-19 Crude Oil Price (Brent) Sep-19 Jan-20 May-20 Sep-20