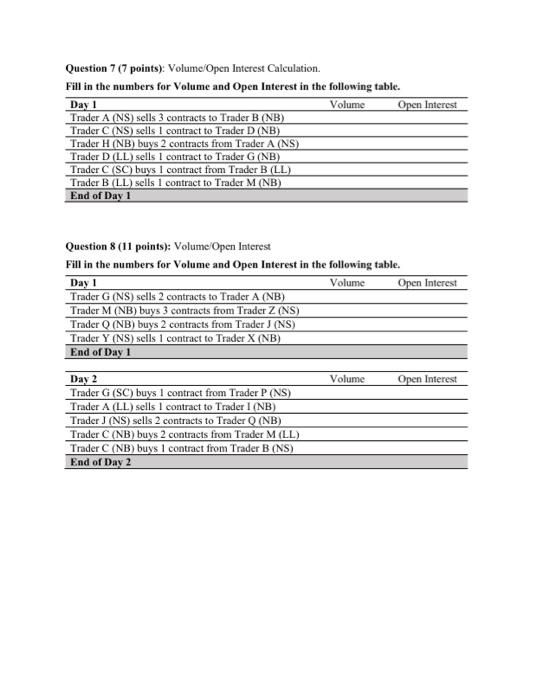

Need help with question 7. i attached the other pages to the assignment but i dont tbink they connect

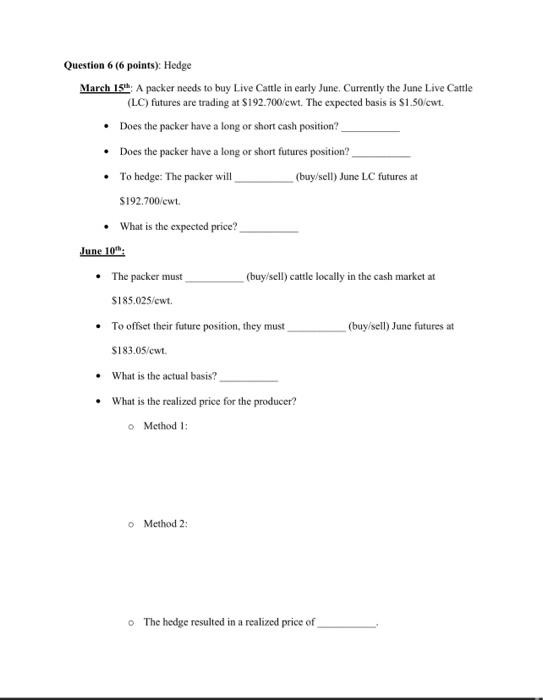

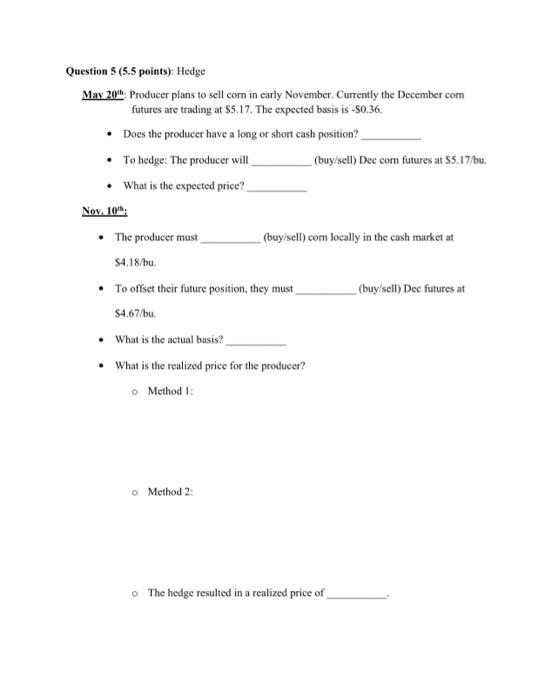

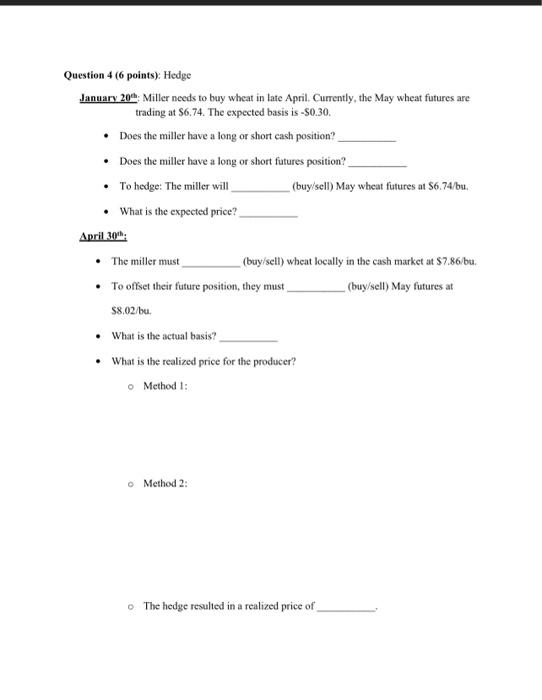

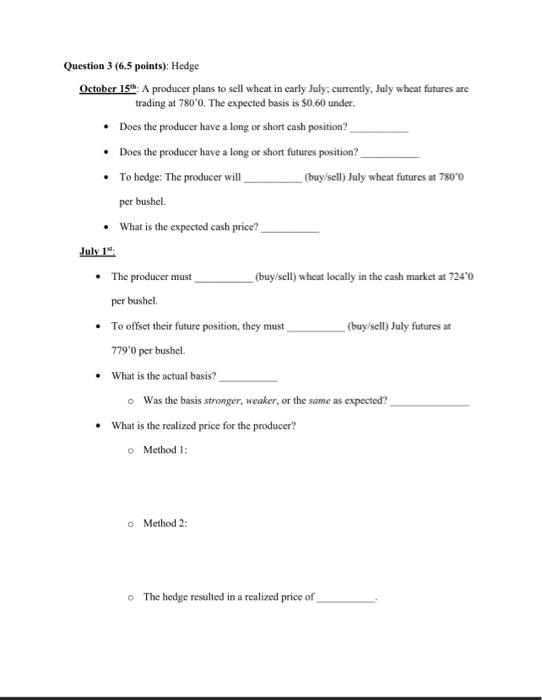

Question 7 (7 points): Volume/Open Interest Calculation. Fill in the numbers for Volume and Open Interest in the following table. Question 8 (11 points): Volume/Open Interest Fill in the numbers for Volume and Open Interest in the following table. Question 6 (6 points): Hedge March 15 th: A packer needs to buy Live Cattle in early June. Currently the June Live Cattle (LC) futures are trading at $192.700/cwt. The expected basis is $1.50/cwt. - Does the packer have a long of short cash position? - Does the packer have a long or short futures position? - To hedge: The packer will (buy/sell) June LC futures at $192.700/cwL - What is the expected price? June 10th: - The packer must (buy/sell) cattle locally in the cash market at $185.025/cwt. - To offset their future position, they must (buy/sell) June futures at $183.05/cwt. - What is the actual basis? - What is the realized price for the producer? o Method 1: - Method 2: - The hedge resulted in a realized price of Question 5 (5.5 points): Hedge May 20 th:. Producer plans to sell com in early November. Currently the December com futures are trading at $5,17. The expected basis is $0.36. - Does the producer have a long or short cash position? - To hedge: The producer will (buy/sell) Dec corn futures at \$5.17/bu. - What is the expected price? Nov, 10th: - The producer must (buy/scli) corn locally in the cash market at 54.18/bu. - To offset their future position, they must (buy/sell) Dec futures at $4.67/bu. - What is the actual basis? - What is the realized price for the producer? - Method 1: - Method 2: - The hedge resulted in a realized price of Question 4 (6 points): Hedge January 20 : Miller needs to buy wheat in late April. Currently, the May wheat futures are trading at $6.74. The expected basis is $0.30. - Does the miller have a long or short cash position? - Does the miller have a long or short futures position? - To hedge: The miller will (buy/sell) May wheat futures at $6.74/ bu. - What is the expected price? April 30"t: - The miller must (buy/sell) wheat locally in the cash market at $7,86/ bu. - To offset their fufure position, they must (buy/sell) May futures at $8,02/bu. - What is the actual basis? - What is the realized price for the producer? - Method 1: - Method 2: - The hedge resulted in a realized price of Question 3 (6.5 points): Hedge October 15th: A producer plans to sell wheat in early July; currently, July wheat futures are trading at 7800. The expected basis is $0.60 under. - Does the producer have a long or short cash position? - Does the producer have a long or short futures position? - To hedge: The producer will (buy/sell) July wheat futures at 7800 per bushel. - What is the expected cash price? July 1s: - The producer must (buy/sell) wheat locally in the cash market at 7240 per bushel. - To offset their future position, they must (buy/sell) July futures at 7790 per bushel. - What is the actual basis? - Was the basis stronger, weaker, or the same as expected